(Bloomberg Opinion) -- Italy is not hanging about. Hot on the heels of its successful 16-year syndicated bond sale in mid-January, it has announced a new 30-year placement. Given the “fill your boots” hunger for all types of debt at the moment — from Turkey to Uzbekistan — it will probably get away okay. It’s certainly priced that way. But with the political and economic turmoil in Italy only getting worse, this may be a temporary sugar high for investors.

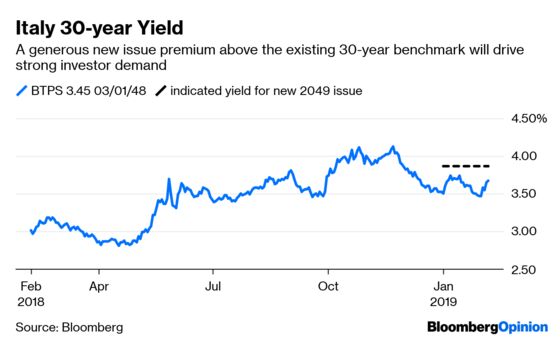

Italy has 250 billion euros ($285 billion) to fund this year, so you can see why Rome might want to seize advantage of the huge demand this year for European sovereign debt. But it risks being too aggressive by opting for such a long duration. After all, the European Central Bank’s bond-buying program is no longer around to provide support. A coupon in the region of 3.875 percent will no doubt tempt enough investor demand into the rarefied environment of 30-year maturity debt, but it’s a bold move when Italy has fallen back into its no-growth rut.

The country is in a technical recession after negative gross domestic product for the second half of 2018 and, with weaker January purchasing managers’ surveys, there’s no obvious rebound in the first quarter. This has led to media speculation that the populist government might even reopen the recently settled budget dispute with the EU by pushing for another supplementary round of spending. Italy remains a much larger credit risk than its European peers.

Even if the initial uptake is strong, a poor subsequent performance of the 30-year note could destabilize Rome’s overall ability to fund its gargantuan debt-load. That would be a serious predicament. Italy will try to raise about 13 billion euros in 30-year debt this year, according to analysts from NatWest Markets. Some 1.5 billion euros’ worth has already been sold via regular monthly auctions, suggesting there was no specific need to raise via alternative means. This will be the first syndicated 30-year offer since June 2017, when 6.5 billion euros was raised on the back of a 24 billion euro order book. But Italy was on much surer political and economic footing then.

And there’s no following wind to smooth the sale. The 34 billion euros of Italian bond redemptions last week will have been reinvested by now. The next batch of maturities and coupons (for 28 billion euros) doesn’t fall until the end of February.

Any eventual problems with the latest sale would endanger the roughly 100 basis point drop in Italian 10-year yields since the EU budget standoff was resolved. Equally, success could help Rome break the back of Italy’s large refunding burden this year — completing nearly half of this year’s ultra-long funding. Italy is ignoring its own troubles and gambling heavily on sustained investor appetite for European government debt.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.