(Bloomberg Opinion) -- Who would want to be a primary dealer in Italian government debt? Thursday is a seminal day for Italy with the new coalition’s headline budget proposals expected after the market close (barring any last-minute delays.)

But before that comes Italy’s monthly five and 10-year bond auctions. That’s quite a test of investor demand right before the most important announcement of the populist administration’s tenure. Buyers will no doubt be skittish ahead of finance minister Giovanni Tria’s press conference, should it go ahead, but the Italian Treasury is falling over itself to help the sales go smoothly.

Just 4 billion euros ($4.7 billion) will be up for grabs, a big drop from the 6 billion euros at the last fixed-rate monthly bond sale in August. This looks prudent amid the volatility around the budget announcement. Plus there are no redemptions of maturing Italian bonds due for three weeks, which means investors have less spare cash to plow back into the new bonds.

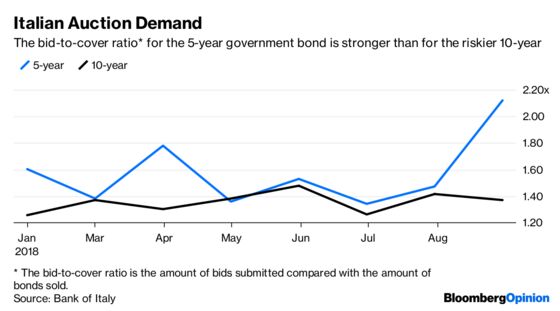

Despite all the background turmoil, the last five-year sale was a success. Bids could have covered the (relatively large) 3.75 billion euro offer more than twice over, the strongest demand for these bonds in 2018. Demand for the five-year notes will probably be strong in Thursday’s auction, not least because the amount on offer has been cut nearly in half. Yields have dropped 65 basis points to 1.8 percent since the last auction, but they’re still about three times higher than before the Italian political situation erupted in May.

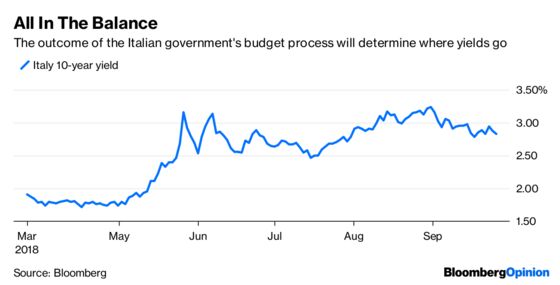

The trouble comes from the longer maturity. Appetite for the 10-year benchmark at all the monthly Italian auctions this year has been lackluster. That’s despite yields rising from 1.8 percent in May to a peak of 3.23 percent at the end of August (they’ve fallen back 40 basis points since). At least the Treasury has slashed the amount for sale to just 2 billion euros this time, the same size as the five-year auction. It doesn’t want a repeat of May’s difficult auction, when it could only find buyers for 3.6 billion euros of 10-year bonds after trying to sell 4 billion euros’ worth. And this after swallowing a discount.

At the 10-year level, higher yields haven’t created stronger demand from investors because of perfectly natural fears about the fiscal rectitude of a populist government. We’ll hopefully get a glimpse of whether they’re right to fret later on Thursday, with Tria’s budget proposals. Still, even if there’s no delay, this won’t be the end of the matter. The budget will need to go through a long process of approval for the rest of this year, with the EU also having a say.

Confidence has been creeping back into Italian government bonds as the populist noises have been quietened by Tria’s fiscal doggedness. Still, concern around the 10-year bonds shows the limits of investor faith. Thursday’s auction remains one for the brave.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2018 Bloomberg L.P.