Is Warren Buffett Sending a Signal About the Bond Market?

Berkshire Hathaway is refinancing floating-rate notes with 30-year fixed-rate debt. Traders take notice.

(Bloomberg Opinion) -- Warren Buffett is wading into the bond market with a new deal, leaving traders wondering whether the Oracle of Omaha is making a prediction about the direction of interest rates.

Berkshire Hathaway Finance Corp. is issuing 30-year fixed-rate bonds to refinance $950 million of floating-rate senior notes that mature at the end of next week. The decision to switch from floating to fixed could be viewed as a bet on where interest rates are headed. Or, at the very least, it could indicate that the company sees the steep decline in long-term yields over the past two months as a market-timing opportunity that’s too good to pass up.

Berkshire, with the third-highest credit rating from both Moody’s Investors Service and S&P Global Ratings, is expected to price the debt on Thursday with a spread of 150 to 155 basis points above benchmark Treasuries. The 30-year U.S. yield fell to 2.91 percent on Thursday, the lowest since January 2018. The recent bond rally equates to millions of dollars of savings a year for Berkshire, if its plan all along was to convert from floating to fixed rate.

The other interpretation is that the company chose to refinance with long-term fixed-rate debt because it sees the big drop in 30-year yields as unsustainable. After all, if a borrower expects interest rates to rise in the future, it would prefer to lock in a fixed rate now rather than face higher payments down the road.

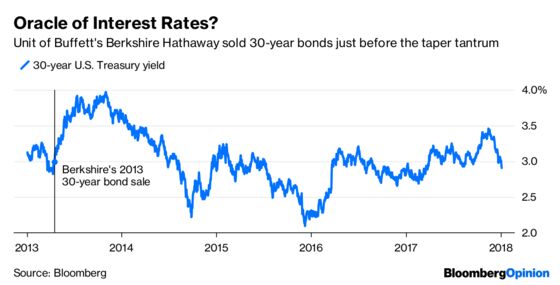

Now, the Berkshire unit also issued 30-year bonds in August to refinance a portion of floating-rate notes. But before that, it hadn’t issued debt with such a long maturity since May 2013, which just so happened to be right before the “taper tantrum” that sent interest rates soaring. Buffett said at his annual meeting ahead of the offering that he felt sorry for savers who depend on fixed interest payments, given the low yield levels at the time.

Regardless of the exact motivation for this week’s deal, Berkshire is borrowing at a time of growing angst among traders about the path of interest rates. In a recent Bloomberg News roundup of forecasts for 2019, BMO Capital Markets and Morgan Stanley said the 30-year yield will fall to 2.85 percent by the end of the year, while JPMorgan Chase & Co. predicts it will rise to 3.55 percent. NatWest Markets is the most bearish on the long bond, calling for the yield to climb to 3.8 percent.

Yet it’s not exactly the worst time to be a floating-rate borrower, either. In a first, bond traders on Thursday were pricing in a full 25-basis-point rate cut by the Federal Reserve at its September 2020 meeting. And Dallas Fed President Robert Kaplan said on Thursday that the central bank should pause rate hikes “in the first couple of quarters of this year.”

Of course, for corporate issuers, yield spreads also matter. Berkshire’s expected premium to the benchmark is right in line with the average spread for the Bloomberg Barclays U.S. Corporate Bond Index, which has soared to the highest since mid-2016 amid the turbulence in equity markets. At 154 basis points, that penalty is still just half of what it was for issuers in July 2009, after the last recession ended. That context matters because one of the most reliable indicators of an impending downturn — the flattening yield curve — reached a new post-crisis low on Wednesday.

When it comes to tapping the bond markets, Berkshire has no shortage of options. Its decision to issue 30-year fixed-rate bonds, rather than going with a shorter maturity or even sticking to floating-rate debt, has to factor into traders’ thinking about where rates and credit spreads are headed in the new year.

Parent company Berkshire Hathaway Inc. is the guarantor.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.