Is the Trade War Really Holding China Back?

Domestic policies such as reining in credit and investment-driven growth are having a much bigger impact on the economy.

(Bloomberg Opinion) -- With China posting its weakest growth in a decade, officials have blamed a “challenging external environment” – polite language for the trade war. It makes for a good sound bite with an obvious villain. But in reality, responsibility for the slowdown rests squarely with Beijing’s policies and cracks in the economy.

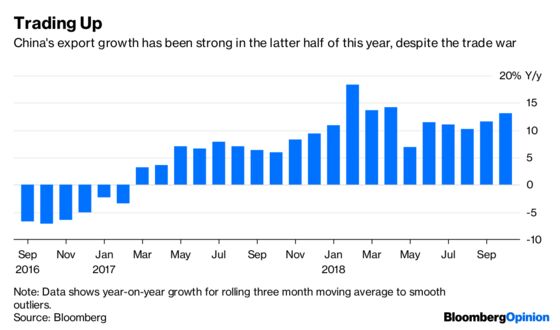

For all the headlines and hand-wringing, the macro-level impact of U.S. tariffs on China is tiny. Growth in the country’s exports to its largest trading partner, currently at 13 percent, is on track to record its best rate in 10 years, largely thanks to U.S. strength.

Even without trade barriers, it’s unlikely Chinese exports would grow much faster. If export growth to the U.S. were to hit 20 percent, for instance, that would add just $22 billion to a current GDP of about $13 trillion. Put another way, such an increase would nudge the 9.7 percent third-quarter nominal GDP growth figure to a less-than-overwhelming 9.85 percent.

The bigger drags on the economy are Beijing’s policy decisions, such as restricting credit growth and investment. When President Xi Jinping was reelected chairman of the Chinese Communist Party in October 2017, new total social financing was growing at 31 percent year-to-date. One year after his coronation, this broad measure of credit is down 13 percent.

Xi’s maneuver to sharply curb credit growth so soon after taking control for a second term was a prudent one – and its economic impact far outweighs that of the trade war. Assume Beijing chose to restrict new total social financing growth to 10 percent rather than shrinking it 13 percent. This would have added 4.1 trillion yuan ($590 billion) to economic activity, nearly thirty times more than the effects of the spat with Washington.

China’s move to limit investment, another necessary step to improve the economy, is also slowing growth. In 2015, fixed-asset investment amounted to 80 percent of GDP, and it has been falling since. As of September, the figure was growing at a relatively restrained 5.4 percent, or just 55 percent of 12-month GDP.

Measures of confidence – for investors, consumers and businesses – have fallen through 2018. Whether we can blame this on the trade war is debatable, and even more questions emerge about the ultimate impact on behavior. Foreign direct investment in China is up, in line with historical norms, and the fall in the yuan from a stronger dollar has muted the impact of tariffs.

Beijing has made a sound policy decision to rein in runaway credit and investment-driven expansion, for which policymakers should be commended. Slowing consumption – as people struggle to pay their mortgages and real-estate transactions drop – is a legacy of the debt-fueled growth Beijing championed after the 2008 financial crisis.

China now faces significant economic challenges. Beijing has announced a steady stream of stock-market bailout funds, financing for private and small enterprises, and measures to get the economy back on track. It is a profound disservice, however, to conflate those problems with a short-term trade war, which will have minimal impact on the country’s policy and economic challenges in the long run.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Christopher Balding is a former associate professor of business and economics at the HSBC Business School in Shenzhen and author of "Sovereign Wealth Funds: The New Intersection of Money and Power."

©2018 Bloomberg L.P.