(Bloomberg Opinion) --

Has the U.S. stock market, at last, reached the turn of the cycle? The economy, of course, has been running hot, but in the short run the correlation between the economy and the stock market is minimal. And if the recent renaissance of consumer staples and other defensive stocks is anything to go by, the stock market cycle may well have turned towards pessimism.

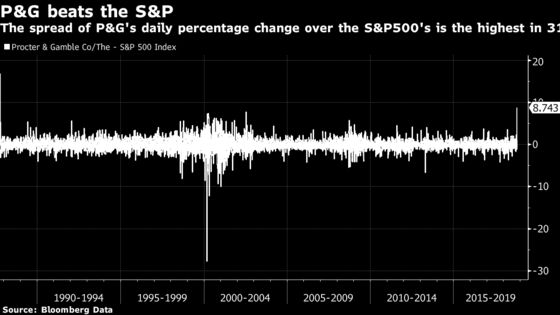

Procter & Gamble Co. released its results for the third quarter on Friday, and shareholders rewarded the company with its biggest daily outperformance relative to the S&P 500 Index since the day after the Black Monday crash in 1987. P&G’s share price gained 8.80 percent after publishing very good sales, while the rest of the market was flat. As this chart shows, that type of divergence is very rare:

(For those interested, that stunning underperformance one day in early 2000 came when P&G issued disappointing earnings and a profit warning only a week after reaffirming guidance, just as the rest of the market was in the final euphoric days of the dot-com bubble.)

Naturally, this is good news for P&G, but it is arguably bad news for the rest of the market. When investors start to get excited about the sales of shampoo and toothpaste, that tends to mean that they are not terribly optimistic about life in general — or at least the economy. P&G, like Walmart Inc., is considered a classic defensive stock that investors only get excited about and buy with any enthusiasm when they are worried about everything else.

P&G’s performance Friday was startlingly strong, but it continued a period when defensive sectors — which for this exercise I will take to be Consumer Staples and Utilities — have started to outperform cyclicals — which we will take to be Industrials and Consumer Discretionary. As the next chart shows, cyclicals have meaningfully outperformed ever since the November 2016 elections, and even outperformed during the sharp rise in equity market volatility in February. This current bout of turbulence is different. Judging by the shift from cyclical to defensive, this sell-off seems to reflect genuine nerves about the economy.

The chart above was my replication of one by strategist Jim Paulsen of Leuthold Group, which went into more detail by adding Materials to the list of cyclicals, and measured the indexes on a total return basis. That approach made the snap back from cyclicals to defensives look even sharper.

Another worrying point to bear in mind is that shares of Consumer Staples such as P&G and Walmart tend to be bought primarily for their perceived role as offering protection against broader weakness in equities, rather than for any reassuring characteristics such as high and regular dividend yields. Andrew Lapthorne, a quantitative analyst at Societe Generale SA, showed in a research note in 2013 that demand for Staples was driven by the perception that they offered drawdown protection. Here is how he explained the approach, and its spectacular results:

[W]e devise a strategy that invests mainly in Consumer Staples but we switch into the equity market rather than the staying in the sector during periods of major market declines. By doing this we effectively remove the drawdown protection from the sector by being totally invested in equities instead of lower-beta Consumer Staples during market pullbacks. So, with perfect foresight, we identify the months when the MSCI World index lost more than 3%. Then, rather than stay invested in Consumer Staples (as you should), we invested (mistakenly) in the equity market instead. The purpose here is to understand just how important capital preservation is in driving overall returns from the Consumer Staples sector versus the market by replacing the best months of relative performance with the market return. By investing in the market, and not the sector, during those periods when the market was down 3% or more effectively kills the outperformance of the sector, to the extent that the sector goes from outperforming by nearly 50% to underperforming by 20%. This in part starts to demonstrate just how important the downside protection is in driving the performance of this sector.

If investors are starting to get excited about consumer staples again, and reacting with such delight to P&G’s earnings, it does suggest that sentiment is shifting away from optimism. The sales of Tide may be high, but in the rest of the market the tide appears to be turning.

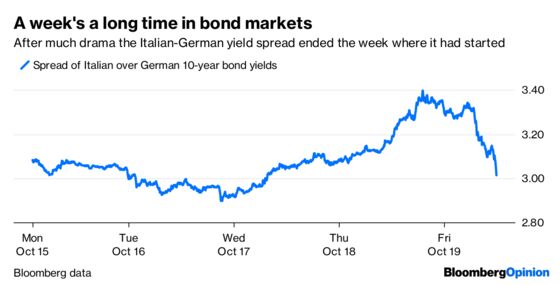

I spent the end of last week anxiously checking yield spreads for Italian bonds as shares of euro zone banks kept tumbling, while anxiously waiting for news from interminable European Union summits. At one point, the spread over similar maturity German bunds had lurched upward by as much as 50 basis points, but by the end of the week it was virtually unchanged from where it started. And all of this came before the much anticipated announcement by Moody’s Investors Service late on Friday that it was downgrading Italy’s debt rating to the lowest level of investment grade, putting it on the cusp of “junk.” The chart shows how the spread of Italian over German bond yields moved last week, and there is every reason to fear that this week could be just as erratic:

I spent several years at the beginning of this decade watching European government debt spreads on an almost constant basis. It was no fun then, and it’s no fun now. But there never was supposed to be a this time.

I am not alone in feeling this way. Ulrich Leuchtmann, a foreign-exchange strategist at Commerzbank AG, evidently feels the same way. This is how he started his note Friday morning:

Not another euro zone crisis, please. I am beginning to feel too old for sleepless nights during which I wait for the end of Euro Group emergency meetings — while staring at an empty EbS screen, too old to work through thick emergency plans in cooperation with our Macro and IR team in a panic (“10 page each!”) etc. But there is no way around it. The combination of the tax-cutting right-wing populists and happy-to-spend left-wing populists in Rome has provided Italian bonds with a momentum that very much reminds of 2011 (figure 1). The problem is: If yields (10-year BTPs back at approx. 3.7% after all) are back at a level that makes the sustainability of the debt levels look significantly worse, then there is no stopping things. Rising yields are then no longer mainly a compensation for the increased risks of Italian fiscal policy, but become the driver of a vicious circle of falling credit quality and rising yields — just as was the case in 2011. It is difficult to say with any degree of certainty when exactly this point of no return will be reached in Italy, most definitely for your FX analyst. However, there is that smell in the air.

It is hard to disagree. And the politics seem to have the same vicious logic as the markets. The Italian government seems intent on defying the EU’s budgetary demands, and it is not Greece or Cyprus. It is too big to be pushed around, and the exposure of banks in the rest of the euro zone to Italy is so great that Italian politicians really could try to call the EU’s bluff and get away with it. But unfortunately, Italy is not able to call the bluff of bond traders. So it is best to be prepared. Some final advice from Ulrich Leuchtmann:

I am going to fill my stockpile of crisps, coke and sweets in the office in preparation for the long nights I might to have to spend here.

You could always try looking for some healthier snacks, but other than that this is good advice.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

John Authers is a senior editor for markets. Before Bloomberg, he spent 29 years with the Financial Times, where he was head of the Lex Column and chief markets commentator. He is the author of “The Fearful Rise of Markets” and other books.

©2018 Bloomberg L.P.