The One Italian Bank That’s Ready for the Next Storm

(Bloomberg Opinion) -- The outlook is darkening for Italian banks. Intesa Sanpaolo SpA has built a decent fallout shelter — but it may be the exception.

Though the Italian bank said Tuesday it delivered on its profit and dividend objectives for 2018, loan growth slowed, and the country’s growing economic malaise will complicate plans to expand revenue. Net interest income in the fourth quarter fell 5.4 percent from the year-earlier period and commissions at Italy’s second-largest bank also dropped, missing analyst estimates.

Chief Executive Officer Carlo Messina is confident the bank can deliver “much higher” income from lending in 2019 and said net inflows will exceed 2018 in a “significant way.” He may sound overly bold but his record of meeting objectives is pretty good — he deserves the benefit of the doubt.

Investors in his rivals should take note. Not many of them will have the levers Messina can pull at Intesa to ease the rough patches that lie ahead.

The Italian economy slipped into recession at the end of last year and the slump may worsen. Weakening domestic demand and a decline in export orders drove a January slump in business activity among Italian service providers.

These are hardly the conditions that will help banks clear up a mountain of bad debt left behind by the previous contraction. Banks are also getting squeezed from a surge in funding costs.

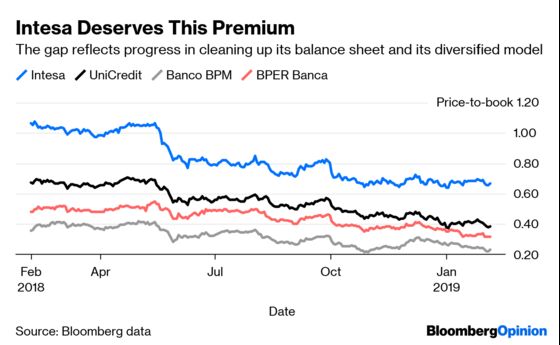

But Intesa may be able to manage better than most. It is further along its cleanup than competitors. Non-performing loans are 9 percent of the total, a figure Messina said he’ll be able to bring down to 6 percent ahead of schedule. Except for its larger peer, UniCredit SpA, smaller competitors still have ratios that exceed 10 percent and regulators are now pushing them to improve their coverage of soured credit. Expect pressure on profit and capital to persist.

What’s more, not many of Intesa’s domestically focused competitors would be in a position to dismiss so lightly the 3 percent drop in deposits it reported for the fourth quarter. Messina said he doesn’t care about the decline — it was largely driven by corporates and institutions, and he explained that these aren’t strategic funds, as opposed to the bank’s retail deposits, which tend to be stickier and can be turned into fees.

In fact, Intesa is so rich in funding, Messina said the bank can ride out the spike in costs by avoiding selling medium-term wholesale bonds in the first half.

As for growth, he’s counting on the lender’s asset management machine to convert more of the company’s consumer deposits into commission income. And he’s pledging to grow a very small international loan book — it currently represents about 8 percent of total loans — to offset the sluggish demand at home.

For now, Intesa’s valuation premium to its Italian peers seems justified. But its response to the deteriorating environment offers no template for the rest of the nation’s lenders in 2019.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Elisa Martinuzzi is a Bloomberg Opinion columnist covering finance. She is a former managing editor for European finance at Bloomberg News.

©2019 Bloomberg L.P.