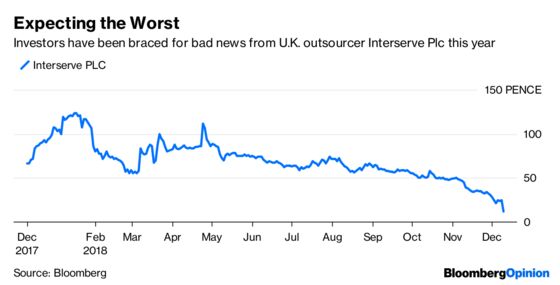

(Bloomberg Opinion) -- Investors had been bracing for bad news from Interserve Plc. Monday's announcement that the U.K. government contractor is considering a debt-for-equity swap was worse than they had feared. The scale of deleveraging required is so great that even assuming the company is repaired, existing shareholders are unlikely to enjoy much of the upside.

Interserve overextended its business and balance sheet venturing into areas beyond its core expertise of construction. Banks and hedge funds had already put a colossal refinancing package in place, but an action plan to cut debt was sure to follow. That moment has come.

On Monday, Interserve confirmed it was looking to bring net debt to down to 1.5 times Ebitda from an estimated five times Ebitda at the end of this year. That means cutting it from roughly 650 million pounds ($821 million) to around 200 million pounds – a tall order.

The shares halved in value in a morning, paring the company's market value to just 18 million pounds. It had been as much as 1.1 billion pounds four years ago.

The new leverage target looks at once both aspirational and only just conservative enough. Following the collapse of construction group Carillion Plc at the beginning of the year, businesses reliant on government contracts have been racing to cut their borrowings.

Capita Plc used a rights offering earlier this year to reduce indebtedness to 1.5 times Ebitda. Builder Kier Group Plc is on the road marketing a share sale to bring average leverage to under 1 times Ebitda.

With Interserve's market capitalization so reduced, it's hard to see shareholders writing a check to solve the problem. An outside investor is theoretically possible, as are asset sales. The reality is that fresh equity and orderly disposals are probably going to have to be the second act in any deleveraging, contingent as they are on a partial repair of the balance sheet. Hence Interserve's lenders and bondholders will have to take some pain by swallowing extended maturities on their debts and converting some into equity.

Quite how the burden will be shared is hard to pin down. Interserve's enterprise value is about the same as its borrowings, implying the equity is mainly option value. A debt-for-equity swap covering the full 400 million pounds or more needed would leave existing shareholders with a mere fraction of the company – and a similarly thin slice of any upside.

And that upside requires a big leap of faith. Based on the multiples of its better-performing peers, a well-capitalized Interserve could have an enterprise value of as much 1 billion pounds – about 350 million pounds more than today.

The government would surely prefer that Interserve achieves its reorganization while remaining a publicly traded company. Unlike Carillion, the management team is at least relatively new – albeit already in the spotlight over excessive pay.

Assuming Interserve emerges from this, it will be the new money and the lenders, not existing shareholders, who enjoy the lion's share of any recovery.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2018 Bloomberg L.P.