(Bloomberg Opinion) -- About the closest Intel Corp. got to recognizing concerns around the state of the chip sector was to note how it’ll be difficult to keep the momentum going in 2019:

“This has been a fantastic year for us, I think for the industry, and you know that just makes comps a little bit tougher as we go into next year.”

That’s CFO Bob Swan answering a question about possible headwinds for the company given the trade war between the U.S. and China. It’s almost as though Swan, who’s also interim CEO, wasn’t even aware of the cacophony outside Intel’s Santa Clara headquarters.

And, frankly, why would he be?

Not only did Intel’s sales and earnings per share beat estimates, Swan raised the company’s full-year guidance. Intel is also planning to spend around $1.5 billion more on capex this year than it originally expected. Its budget for equipment to make logic chips – the stuff that’s not memory – will rise even further next year, he said.

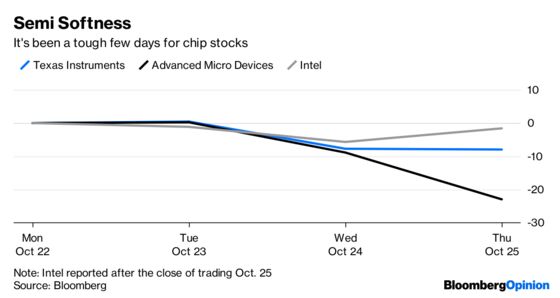

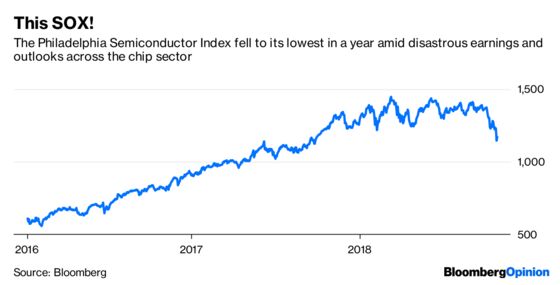

Meanwhile, shareholders of Advanced Micro Devices Inc. and Texas Instruments Inc. are 23 percent and 8 percent poorer respectively in the last two days after both companies delivered bad news. Taiwan Semiconductor Manufacturing Co. kicked off a gloomy earnings season last week when it blamed continued cryptocurrency weakness and excess inventories for a disappointing outlook and a third cut in its full-year guidance.

Then in waltzes Intel fiddling an upbeat tune.

Either it’s somehow immune to the macro meltdown affecting not just chips but multiple areas of the global economy, or the dark clouds just haven’t appeared on its horizon yet.

I’m leaning toward the latter.

Intel deserves the accolades its management, and its share price, will get from turning in a great set of numbers. But a lot of this is accidental or not easily replicated.

The company itself conceded that third-quarter numbers were juiced by surprising demand for PCs, a slice of the tech industry that’s been a laggard for the past decade. Despite pivoting strongly toward the development of chips used in server farms and communications equipment, its client computing group still accounts for more than half of sales. A 15 percent jump in shipments of desktop PC chips from the prior quarter, and a 12 percent increase for notebooks, drove the division to record sales.

That strength will continue this quarter, though Intel said this will constrain its ability to meet demand as the chipmaker prioritizes higher-value products used in data centers.

Which is where I think Intel’s landmines may lie next year.

The world’s obsession with streaming TV shows, playing online games, and uploading selfies has been a boon to swathes of the tech industry. That enthusiasm for content won’t die anytime soon. But as the hardware side of the equation matures it’s going to get more competitive.

Caught off guard by a slowdown in demand for graphic chips and the crypto industry, AMD is on the cusp of beating Intel to the latest production technologies. That’s because it made the decision earlier this year to switch manufacturing to TSMC, which is leading the world in production of chips at 10 nanometer and the more advanced 7-nanometer nodes. (Apple’s latest iPhone has chips made at 7nm – Intel doesn’t expect to ship 10nm until next year.)

Beyond AMD, Intel faces the risk that its clients are considering building their own chips. It never really made sense for PC brands like HP Inc., Dell Inc. or Lenovo Group Ltd. to go it alone on semiconductors because the unit cost of end devices is low and those products are quite varied. When you buy servers by the truckload for thousands of bucks each, then designing your own components seems like a wise move.

It's worth noting that the cloud giants aren't invincible either, which makes any sales to them far from a sure bet. Both Amazon.com Inc. and Alphabet Inc. turned in disappointing numbers this week.

Then there are the macro headwinds that Swan avoided discussing, and to which even mighty Intel isn’t immune. The world’s biggest chip company may well be better positioned than its rivals to handle any global slowdown, but when the hurricane comes everyone has to batten down the hatches.

Until then, Intel and its shareholders should bathe in the glorious sunshine. While it lasts.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2018 Bloomberg L.P.