(Bloomberg Opinion) -- Fourth-quarter earnings tend to be an afterthought for investors in the U.S. industrial giants. By this point in time, they usually have a good sense of the year that was and have already heard from companies on the near-term outlook.

Not this year.

Investors don’t have the same assurances headed into this earnings season and will be parsing the numbers for even the slightest sign of slowing growth or weakening margins when America’s biggest manufacturers start reporting year-end results later this month. They likely won’t have to look hard: China’s official factory gauge has slipped into a contraction, Europe’s economic growth has slowed, and now that weakness is threatening to spread to the U.S. as side effects from President Donald Trump’s trade war risk strangling the industrial cycle in its adolescence.

Already, the broader U.S. data is coming in on the softer side: A report this week showed the five Federal Reserve indexes of regional manufacturing declined in December, the first time there’s been an across-the-board slump since May 2016. The Institute for Supply Management manufacturing gauge registered above the 50-point level that indicates expansion last month, but relative to November, the reading dropped by the most since the 2008 recession. A measure of new orders plunged 11 points, which Robert W. Baird & Co. analyst Mircea Dobre says is the fourth largest decline in the past 30 years. While payroll and wage-growth data released Friday indicate a still-robust labor market, just 16.6 percent of respondents in the Conference Board’s consumer confidence survey last month expect more jobs in the next six months, down from 22.7 percent the month before in the biggest drop since 1977.

Tariffs are starting to bite, whether via rising raw material costs or simply too much uncertainty for any reasonable business manager to make big supply-chain and purchasing decisions. Industrial demand is still growing and a recession may be a while off in the U.S., but the recent turn in the data is a reminder of how quickly things can change. Recall that FedEx Corp. had to cut its 2019 guidance in December only three months after it had raised it, with CEO Fred Smith blaming a deterioration in the company’s economic outlook that was so rapid “it’s hard to react to it.”

Against that backdrop, it’s hard to imagine industrial CEOs striking the same rosy tone they stuck to in the third quarter as analysts peppered them with questions about the impact of the trade war. The importance of fourth-quarter earnings calls is particularly acute this year because we’ve heard so little from industrial CEOs over the past month. The multi-week parade of year-end presentations known as the “fifth earnings season” among analysts was practically non-existent in 2018. RBC analyst Deane Dray says 14 companies from his multi-industrial coverage area held outlook calls at the peak a few years ago; this year, only five did so, or plan to: 3M Co., Danaher Corp., Illinois Tool Works Inc., Flowserve Corp. and Honeywell International Inc. The latter is fudging a bit by moving its call to January from a usual December slot and Flowserve won’t give specific 2019 numbers until its February fourth-quarter earnings release.

One reason for the lack of a rush to give 2019 guidance may be that CEOs were hoping the extra month or two would bring more clarity on the trade war. And on that front, I expect they are sorely disappointed. Trump and China President Xi Jinping agreed last month to a temporary truce that pushed out until March the U.S. threat to increase tariffs on $200 billion of Chinese goods to 25 percent from 10 percent. Companies are apt to have used the hiatus to lock in orders ahead of more dire levies, which likely aided industrial manufacturers's fourth-quarter numbers. That will be an empty victory, though, if 2019 winds up being a bust.

It remains unclear what kind of deal with China the Trump administration would be willing to accept. On Thursday, Trump tweeted that tariffs on Chinese goods are being paid to the U.S. Treasury; they aren’t. The same day, Kevin Hassett, the chairman of the White House Council of Economic Advisers, predicted “a heck of a lot of U.S. companies that have sales in China” will face lower earnings.

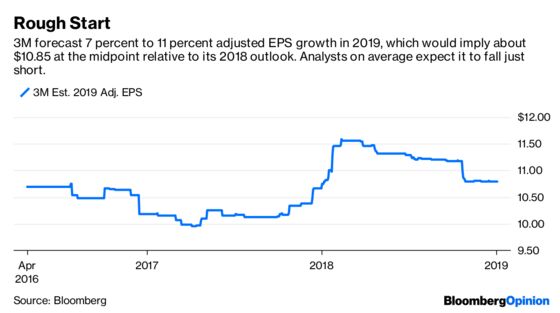

Those companies that did give 2019 guidance at the end of last year may already be regretting it. 3M forecast fiscal 2019 adjusted EPS growth of 7 percent to 11 percent and organic sales growth of 2 percent to 4 percent, both of which look ambitious at the high end in the event of waning economic growth. Apple Inc.’s slashing of its quarterly revenue forecast this week bodes poorly for 3M, which sells display, touch and battery materials for consumer electronics. CEO Michael Roman has been in the job since July and has already had to cut 2018 guidance twice amid weaker-than-expected growth, a pinch from foreign currency swings and rising raw-material costs.

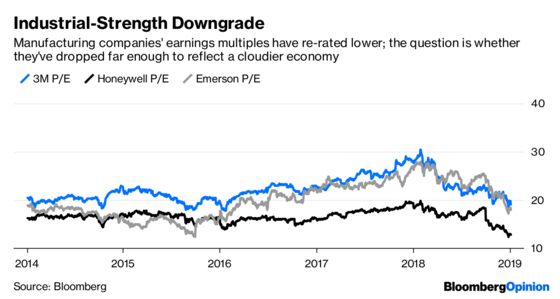

So expect a healthy dose of caution from CEOs. The bigger question is whether markets are sufficiently prepared. The S&P 500 Industrial Index has slumped nearly 20 percent since the end of the third quarter and earnings estimates have been coming down, but RBC’s Dray notes that on a price-earnings basis, the sector is still trading at a higher-than-typical premium relative to the broader benchmark. Particularly if you think a recession is nigh, some of these stocks are arguably still a tad expensive, and that could lead to unfortunate surprises come earnings season.

General Electric Co. CEO Larry Culp is expected to lay out his turnaround strategy in early 2019 and that could take place at an event separate from its fourth-quarter earnings; either way, things like tariffs and rising raw material costs are the least of his concerns right now and unlikely to be the focus.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.