(Bloomberg Opinion) -- A merger between two of Indonesia’s big three cement companies could be just the ticket to drag the industry out of years in the doldrums and deliver a prize to a state champion. Nevertheless, Jakarta should block it.

Government-controlled PT Semen Indonesia will buy LafargeHolcim Ltd.’s 81 percent share in PT Holcim Indonesia in a deal valuing the entire business at $1.75 billion, the Swiss company said in a statement late Monday European time.

That’s great news for investors in the target business. Semen Indonesia is paying a premium of about 13 percent to Holcim Indonesia’s enterprise value on the eve of the deal. Assuming net debt is held constant, shareholders will get about 21 percent more than the stock was worth as of Monday’s close, and three times what it fetched three months ago. Indonesian property developers, builders, owners and tenants have less to celebrate.

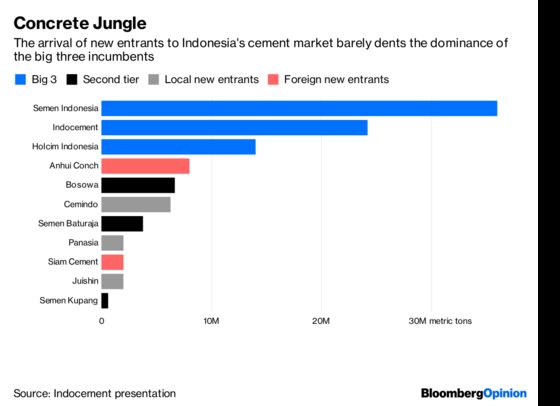

To be sure, as my colleague Anjani Trivedi wrote earlier this year, Indonesia’s cement market is a dismal one – plagued with overcapacity and a slowdown in demand that hit just as new offshore players such as Anhui Conch Cement Co. started breaking into the market. The solution, however, is not to increase the concentration among the top three producers, which are already too dominant.

Adding Holcim Indonesia’s 13 percent share to that of the biggest player will leave almost half the market in the hands of one company. Second-ranked PT Indocement Tunggal Prakarsa – itself majority-owned by HeidelbergCement AG – will have just under a quarter of the total, with eight smaller local and foreign players carving up the remaining 30 percent.

It’s common to blame outsiders for the over-production that’s laid the market low after a wave of foreign money swept into Indonesia’s cement market over the past decade.

That’s not really right, though. If anything, it’s the state that’s causing the problems. Semen Indonesia alone has added about 17 million metric tons of annual output capacity since 2010, well ahead of the 10 million tons total capacity now in the hands of Anhui Conch and Siam Cement Pcl. Even adding in upstart local players PT Cemindo Gemilang, PT Sinar Tambang Anthalestari or Panasia, and PT Jui Shin Indonesia only gets you to 20.3 million metric tons from new entrants.

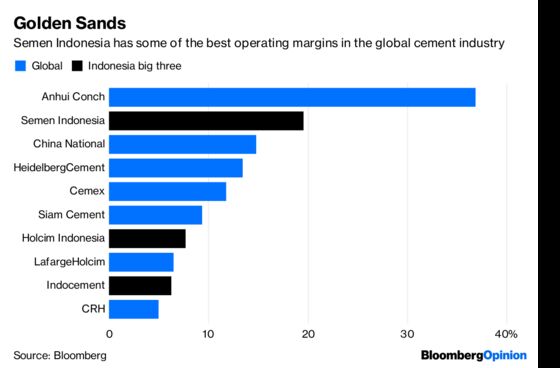

Furthermore, if those new players were the beneficiaries of the downturn in the local market, you’d expect to see the effect in the form of reduced profitability for incumbents. That’s not really happening: While operating margins at Semen Indonesia did decline somewhat last year, they were back up at a very healthy 20 percent in the September quarter, about three times the levels at Indocement and Holcim Indonesia.

With dominant positions in Sumatra, Sulawesi and East and Central Java, the one major region where Semen Indonesia looks weaker is West Java, the largest of the country’s highly localized cement markets and the one that contains the capital Jakarta. Still, even there Holcim Indonesia offers a foothold that the acquirer previously lacked, giving it 53 percent of sales on the island as a whole.

That looks like a bad deal for Indonesia, even if it’s a good deal for its biggest cement companies. A country of 264 million people that’s still drastically underdeveloped needs affordable construction materials if it’s to reach its economic potential. A state-owned enterprise clipping the ticket on its dominant market share isn’t going to deliver that.

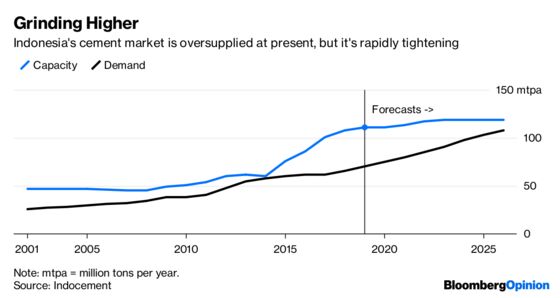

With the country’s construction materials industry already digging itself out of its troubles thanks to recovering demand from property developers and infrastructure, further concentration isn’t even needed to restore profits. If Indonesia’s antitrust regulators want to demonstrate their independence from powerful government businesses, they’ll block this deal and let one of the country’s second-tier players take a shot at being a more capable competitor.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.