Worst Economy in 42 Years Needs an Honest Look

(Bloomberg Opinion) -- India’s economy hasn’t been this bad in 42 years. Pulling it back from the abyss will require more honesty than imagination.

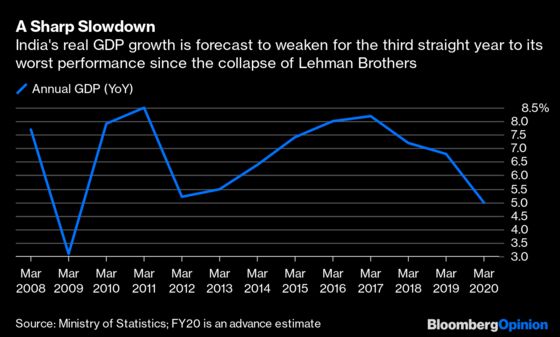

Tuesday’s advance estimates for the financial year ending on March 31 peg the economy’s inflation-adjusted growth rate at 5%, a third year of slowdown. And even this figure could be optimistic. Consumer demand is in the doldrums and government spending — the only thing supporting growth — is bound to be pruned in the closing months of the fiscal year to avoid a budget blowout.

So much for the real economy. The main function of these advance statistics is to aid the upcoming government budget, which requires a handle on nominal GDP. By that measure, not only is the current fiscal year’s 7.5% growth the worst since 1978, it’s substantially lower than the 12% expansion the government had penciled in when projecting taxes. Needless to say, those revenue calculations have gone out of the window.

A dose of realism is called for. When Prime Minister Narendra Modi’s government returned to power in 2019, it made rosy projections for public finances by completely glossing over the previous year’s shortfall in tax revenue equal to 1% of GDP. Any repeat of such machinations in the Feb. 1 budget won’t go down well with investors.

More well-grounded tax assumptions will reveal a big resource gap — closer perhaps to 5% of GDP, including borrowings not captured in the budget but whose burden falls on the taxpayer nonetheless. Indian state governments have a deficit equal to 3% of GDP, higher than the budgeted 2.6%. Add that, and the financial savings of India’s households are almost fully spoken for. No wonder Indian corporate borrowers are making a beeline for overseas debt markets.

Even borrowing abroad, which hit a new record of $22 billion last year, will become costlier should India’s sovereign rating fall one run into junk territory. S&P Global Ratings warned last month that it might cut India’s ratings if economic growth doesn’t recover. A shallow recovery will probably only show up in the second half of the fiscal year that starts in April. Meanwhile, should the recent escalation of U.S.-Iran tensions sustain oil prices at a high level in a weakening global economy, the loss of discretionary consumer spending at home and abroad could hurt India further.

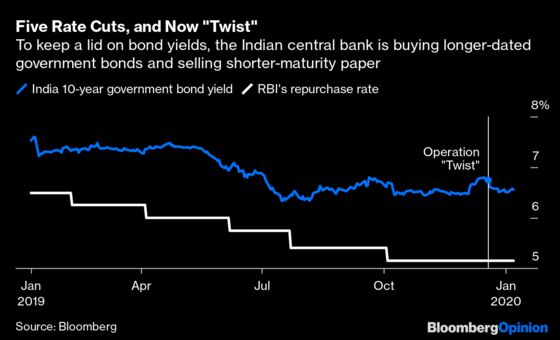

The Indian central bank is “twisting” its balance sheet — selling short-term government bonds to banks and buying long-term securities from them — to keep a lid on the benchmark 10-year bond yield. But this support may not be enough for the government’s five-year, $1.5 trillion infrastructure plan, which will rely heavily on public funding.

So what’s to be done? I’ve suggested that the Indian central bank should purchase assets from the non-bank financial sector, which will help shadow financiers deal with their large overhang of bad loans and open up the clogged funding arteries of the economy. Tuesday’s terrible nominal GDP growth figure should buttress the argument for this kind of quantitative easing.

But while the monetary authority should dare to be unconventional, the most creative tool in the government’s possession — the Excel spreadsheet — won’t help much. In fact, a badly needed overhaul of the broken goods-and-services tax can’t even be attempted in the federal budget. It will require tough political bargaining with state governments, which share the proceeds.

Since its introduction in 2017, the GST has subsumed many of India’s indirect taxes, but it has several design flaws and compliance is both poor and expensive for small firms. According to IDFC Mutual Fund, GST collections this fiscal year may grow only 4%. That’s even slower than nominal GDP. A budget that papers over the very real fiscal constraints to paint a picture of business as usual will do a disservice to the task. A sober acknowledgement of the challenges is the first step toward a fix.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2020 Bloomberg L.P.