India’s World-Beating GDP Can’t Mask the Pain of the Pandemic

Even private consumption, which accounts for more than half of India’s economy, is where it was four years ago.

(Bloomberg Opinion) -- Before the ink could dry on India’s quarterly gross domestic product statistics, officials have been quick to parade last quarter’s 20% growth as vindication of their prediction of “imminent V-shaped recovery.” How sensible is that claim?

The April-June period was when the pandemic overwhelmed oxygen supplies and hospital beds, villagers floated bodies in rivers or left them in shallow graves, families sold their assets to save their loved ones, and an estimated 2.5 million to 2.8 million Indians died because of Covid-19, according to independent researchers.

Statistical artifacts may serve to deny the pain. But GDP expanded 20% from a year earlier, and is set to beat expansion in any major economy this year, only because it had shrunk 24% in the same quarter of 2020. Cheery spin can’t hide the mass suffering across the country. Nor should it detract from the long road to recovery ahead.

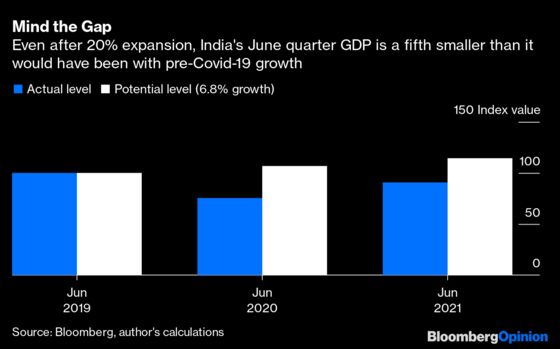

The number policy makers should focus on is minus 20%, for that’s the shortfall in production from India’s pre-coronavirus growth path.

To see this, consider the 36 trillion rupees ($500 billion) of output in the June quarter of 2019. Index it to 100. Had that number continued to increase at the near-7% rate seen during the April-June period of the previous eight years, it would have crossed 114 by now. Instead, India is left with 32 trillion rupees of real production, which corresponds to roughly 91 on the index. That’s a fifth of potential GDP lost in the first quarter of the fiscal year. Assuming that the country gets lucky and avoids a deadly third wave, some of the loss might get made up in the remaining nine months. For that, though, India needs robust pent-up demand. Where will it come from?

The economy was slowing even before the pandemic. What has changed in the past year is the distribution of the income pie. By firing workers, cutting wages and squeezing small suppliers, large firms have improved their share, repaid debt and strengthened their balance sheets. But the gains for India Inc. and the stock-owning rich have come at the expense of households and tiny enterprises, which haven’t received much support from the government.

Even after the pandemic subsided, consumer sentiment in July was only half as strong as before the onset of Covid-19 in February 2020. Worse still, the crucial backbone of the middle class, which comprises over 160 million households earning between 200,000 and 500,000 rupees a year, saw the lowest improvement, “a mere 1 per cent increase over June,” as Mahesh Vyas at the Center for Monitoring Indian Economy puts it.

Private consumption, which accounts for more than half of India’s economy, is where it was four years ago. Among other sources of demand, investment jumped 55% in real, or inflation-adjusted terms, but it was still 17% lower than during April-June 2019. Exports clocked a strong 39% growth over the same period of 2020, but that was because there was no nationwide lockdown this time around.

India’s growth strategy is mostly about boosting the supply side of the economy. The corporate tax rate was cut even before Covid-19. In addition, firms have been promised $28 billion in production-linked fiscal incentives. The underlying demand conditions, however, are artificially propped up by the central bank. More than $125 billion of excess liquidity in the banking system is keeping markets buoyed on the bet that 5%-plus inflation will be transitory, interest rates will remain low for a long time, and that foreign capital won’t up and leave because of any abrupt tightening by the Federal Reserve. Yes, there’s an ambitious $1.5 trillion infrastructure plan to reinvigorate demand. But its success is predicated on the government first monetizing $81 billion of its existing roads, railway, power and other assets to raise resources.

How long can the economy wait for jobs and incomes? Vaccinations have picked up pace, but has some way to go: Only 146 million people in a country of 1.4 billion have been inoculated so far with the required two doses. With the spread of the delta variant in the southern state of Kerala starting to look scary again, India isn’t even in a position to reopen schools. Policy makers aren’t just downplaying the urgency of short-term fiscal palliatives for households, but they’re also ignoring the damaging consequences for India’s long-term competitiveness.

An economy that performs well below potential for too long will suffer a permanent loss. With technology and tastes changing, it’s safe to write off production that fails to materialize in even three or five years. Most of it will never arrive. Something else will have to replace the lost output and the attendant jobs, and that just can’t be food or grocery delivery. There’s work to be done. Chest-thumping about a V-shaped recovery can wait.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2021 Bloomberg L.P.