If It Moves, Tax It. That's Desperate, India

(Bloomberg Opinion) -- Desperation is creeping into India’s economic policy-making. Having lost the fiscal plot, bureaucrats are trying to marshal resources by squeezing taxpayers, foreign investors, firms planning buybacks and even the central bank. Such overreach never ends well.

Tax collections last year were a full 1 percentage point of GDP lower than the 7.9% the government had hoped to obtain. Rathin Roy, director of the New Delhi-based National Institute of Public Finance and Policy, describes the situation as an “unstated fiscal crisis.” Instead of confronting the sober reality, revamping a flawed goods and services tax, and taking steps to pull the economy out of a synchronized slowdown in consumption and private investment, bureaucrats are trying to make up the revenue shortfall by taxing everything that moves.

What else can explain an increase to 42.7% from 35.8% in the tax rate on annual earnings over 50 million rupees ($730,000)? Such a steep jump sends a damaging signal to globally mobile professionals. Why should they put up with Mumbai’s poor infrastructure, New Delhi’s unclean air and Chennai’s acute water shortage when they can just as easily ply their skills from low-tax Singapore? The chilling effect won’t stop with individuals. Since many foreign funds investing in India are structured as non-corporate trusts or associations, they, too, will get caught unless they can lobby their way out.

Even if investors get a reprieve, the companies they buy won’t. Cash-rich firms looking to buy back shares will be subject to a 20% tax that until now was applicable only to dividend distributions. The Indian government may be patting itself on the back for closing a loophole, and for nudging firms to invest more in the real economy. But if the viability of new projects is doubtful, then those investments will still prove elusive. Or they will be wasteful. Embedding a valuation discount in some of the country’s most successful firms is hardly a sensible strategy to boost capacity creation.

Then there’s the 1 trillion rupees the government expects to collect in dividends from financial institutions, a staggering 43% increase from last year. Since an undercapitalized state-owned banking system can’t reasonably be expected to contribute much, the bulk of the demand will fall on the central bank. If the monetary authority’s current profits are insufficient to meet the bureaucrats’ target, they will again clamor for a return of its “excess” capital, even if that means weakening the institution’s operational independence.

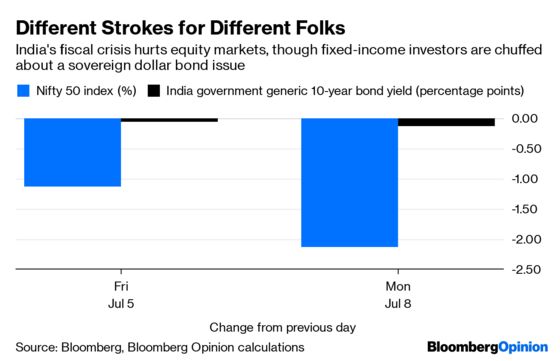

While the equity market is nervous, bond investors are ironically chuffed. Their happiness stems from New Delhi’s decision to issue dollar-denominated sovereign debt, giving up a long-held aversion to subjecting fiscal policy to foreign-currency risk. To the extent such dollar bond sales are strictly capped at a low and stable ratio of India’s overall borrowing, they will help set up useful benchmarks for the private sector to tap overseas investors. However, a more important priority is for India to emulate China and seek inclusion of its local-currency bond market in global indexes. The government should not lose sight of that goal.

As with its tax grab, India’s desperate focus on short-term fiscal fixes risks doing greater damage in the long term.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2019 Bloomberg L.P.