Can QE Work in India With 7% Inflation?

Unconventional policies would help fight stagnation even as rising prices narrow scope for more rate cuts.

(Bloomberg Opinion) -- The anguish is palpable. First, it was the news that India’s nominal gross domestic product is growing at its slowest pace in more than four decades. Now comes the inflation data for December, showing the steepest rise in consumer prices since July 2014. If this is the onset of stagflation, then it will be very hard to beat back the blues. But is that what we’re seeing?

The risk of economic stagnation combined with high inflation has indeed risen, though the former remains the dominant force. For the central bank to get nervous and switch prematurely to a hawkish stance would be a grave error. Even if it can’t reduce interest rates any further this year, the Reserve Bank of India should keep quantitative easing among its options for supporting the economy.

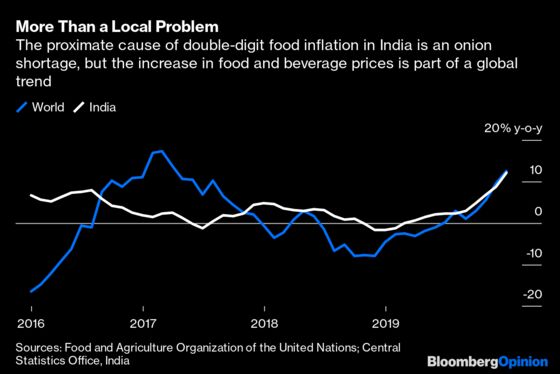

Last month’s jump in inflation to 7.35%, way above the central bank’s 2% to 6% target range, was driven by food. A vegetable shortage has been emerging for some time, and that’s now making substitutes such as eggs, milk and fish more expensive, too. With food prices increasing globally, it’s hard to predict just when the Indian situation will ease.

However, core inflation, which strips out volatile food and fuel, is more under control. It inched up to 3.75% after mobile-services firms bumped up fees and rail fares rose. Still, corporate insolvencies are pushing joblessness higher. New investment — and hiring — are muted. This will constrain wages and producers’ pricing power. While headline inflation will eventually weaken and head toward the core rate, economists expect it to stay above 6% for 2020. That would crimp the RBI’s ability to add to last year’s five rate cuts.

The monetary authority’s support can still make a difference, but only if it alters the strategy of buying government bonds from banks. With deposit-taking institutions sitting on excess liquidity of 3.2 trillion rupees ($45 billion), pumping more cash into an overflowing pond is increasingly pointless. Lubrication is needed elsewhere, and the way to provide it will be for the RBI to start buying assets from insurers, mutual funds, housing finance companies and other lenders that don’t take deposits.

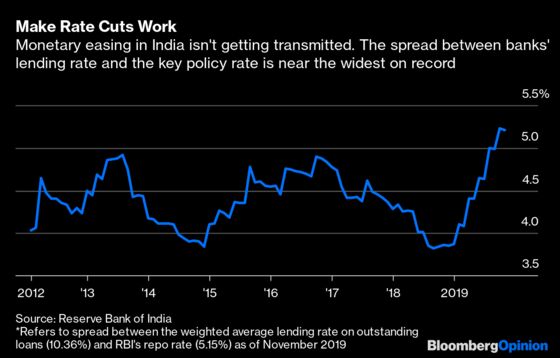

This will hit two goals. As the balance sheets of funding-constrained shadow banks become more liquid, their borrowing costs, elevated since the collapse of infrastructure financier IL&FS Group in September 2018, may start to drop meaningfully. Once the asset-sale proceeds get deposited in the banking system, the lenders will seek to deploy these liabilities to protect profitability. The 10.4% weighted average lending rate of India’s banks in November — double the central bank’s policy rate — should ease.

Recommending Federal Reserve-style quantitative easing when inflation is above 7% sounds like a plan fraught with risk. It needn’t be. For one thing, as the State Bank of India’s chief economist, Soumya Kanti Ghosh, has been arguing, the 46% weight of food in India’s inflation basket is hopelessly outdated. If actual spending on food and beverage is closer to the 30% level reported in national accounts, inflation is being overstated by as much as 2 percentage points.

Right or wrong, the price statistics are likely to have a bearing on what Prime Minister Narendra Modi’s government does in its Feb. 1 annual budget. Any fiscal adventurism, such as deep cuts to income taxes, will need a rethink. Now that the bond market must rule out further rate cuts this year, it may not be in a mood to supply funds for a bulked-up borrowing program. Why should investors accept 6.5% yields on 10-year notes with expected inflation at 6% or higher? On Tuesday, the sovereign yield jumped as much as 10 basis points, the most since Dec. 5. Given its funding constraints, the government still needs the monetary authority to do the heavy-lifting.

For the central bank to throw in the towel now would only worsen the stagnation.

To contact the editor responsible for this story: Patrick McDowell at pmcdowell10@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2020 Bloomberg L.P.