Not All Budget Deficits Are Created Equal

A shortfall that arises from tax cuts is easier to address than one that comes from spending increases.

(Bloomberg Opinion) -- The U.S. budget deficit is now almost $740 billion, the Treasury Department reported last week, prompting a new round of familiar criticism of 2017’s Tax Cut and Jobs Act: The law’s huge tax cuts were irresponsible, as were Republicans’ sloppy and at times deliberately misleading assertions that the law would pay for itself.

That criticism is understandable, but it elides an important distinction. Deficits that arise from tax cuts aren’t as bad as those that come from spending increases.

First, to be clear, it’s nearly impossible for a tax cut to result in increased revenues the year after it’s passed, and Republicans never should have said it would. Over time, increases in economic growth and decreases in tax avoidance can offset some of the revenue losses. But even in the best-case scenarios, these amount to about a third of total revenues lost by the tax cut.

Analysis of the law shows that it would lead to increased revenue — by 2024. But this is because the law includes sunsets and other tax-raising provisions, like a change in the definition of tax brackets. Without the sunsets, the law would result in lower revenues at least until 2027.

So much for the argument that the law would increase revenues. But what about those deficits? The main objection to budget deficits is that they place a burden on future generations. It’s irresponsible, according to this theory, for the current generation to enjoy the benefits of government spending without paying for it.

That’s true as far as it goes, but not all deficits are alike. When a government increases spending, it typically shrinks the private economy. That may well be a choice worth making — but it is one that should be done with a careful eye on the present and future burdens it creates.

When a government cuts taxes, particularly those on capital, it can release resources and leave future generations with a larger economy. In general, the full effects of tax cuts on growth aren’t felt for a decade or more. Future generations will enjoy the most significant benefits, in the form of higher productivity and wages.

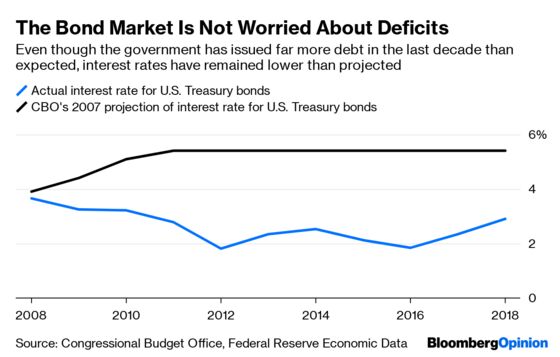

A larger, more productive economy also makes that increased debt easier to bear. The Congressional Budget Office’s scoring process, in which it estimates the effect of proposed bills on the federal budget, invariably shows that lower revenue leads to exploding deficits and debt over time. Crucially, this analysis depends on the assumption that interest rates will rise and that the cost of financing the debt will progressively add to the deficit.

Under these assumptions, however, all paths but a balanced budget lead to eventual ruin. In reality, economic growth almost always exceeds the cost of debt financing. The implication is that modest deficits can be financed indefinitely. Indeed, the U.S. has had deficits pretty much since the 1960s, and its debt burden remains manageable.

The Tax Cut and Jobs Act looks particularly good on this measure. The U.S. currently pays 1.6% of GDP to finance its debt. The Tax Foundation estimates that if all the provisions in the bill were made permanent, the total revenue loss would be $1.4 trillion by 2027. If rolled over indefinitely, that would increase the cost of financing the debt by 0.14% of GDP per year every year.

Over the long run, however — more than 10 years — GDP would be 4.7% higher. The yearly burden on future generations would be less than 1/30th of the increase in annual economic output. These projections, like all budget projections, are the output of economic models.

Now suppose that the models are wrong, that the interest costs are three times higher than expected and growth is one-tenth smaller. In that case, future generations would barely break even. They would be saddled with debt and have barely enough output to pay for it.

In that case, rolling back tax cuts can be done with less political cost or economic dislocation than canceling spending programs. When the Bush tax cuts were partially rolled back in 2012, it was the source of intense debate, but it was nothing like the firestorm that would have come from trying to undo the 2003 Medicare expansion.

Given the U.S.’s slowing long-term growth prospects, politicians should be cautious about increasing the government’s long-term spending commitments. And for that very same reason, they should be bold in seeking growth-enhancing tax reductions.

To contact the editor responsible for this story: Michael Newman at mnewman43@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Karl W. Smith is a former assistant professor of economics at the University of North Carolina's school of government and founder of the blog Modeled Behavior.

©2019 Bloomberg L.P.