(Bloomberg Opinion) -- Europe’s asset managers are trying to avoid the squeeze on fees that has befallen their U.S. peers selling exchange-traded funds. They are hoping to keep revenue streams as high as possible by stressing the attractiveness of more complicated products they can charge more for. It’s an effort that looks doomed to fail.

The size of the global market for ETFs has more than doubled in the past five years to $5 trillion as investors have snapped up the products. JPMorgan Asset Management is predicting a further explosion over the next decade or so.

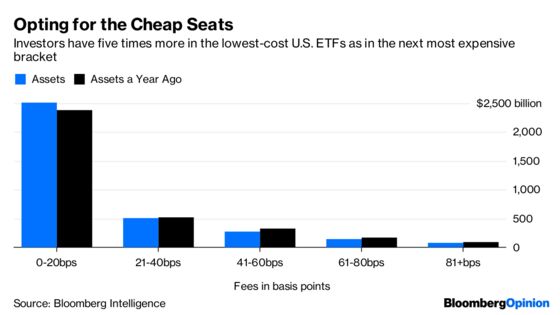

At the forefront is the U.S., which accounts for $3.5 trillion of ETFs in existence. There, the bulk of the money has headed for the products that charge the lowest fees. My colleagues at Bloomberg Intelligence estimate that 97 percent of the money that flowed into ETFs last year went to products charging 0.2 percent or less, up from 83 percent in the previous year.

As a result, the vast majority of U.S. cash is invested in ETFs that charge the lowest fees. So while assets under management have doubled in the past five years, revenue has increased at less than half that rate. ETF issuers earn less than a third of what mutual fund providers can make on the same amount of assets, according to Bloomberg Intelligence.

This race to the bottom has already reached its logical conclusion: in August, Fidelity Investments started offering index funds charging zero fees.

This competition may go even further: Timo Pfeiffer, whose firm, Solactive AG, constructs tailor-made indexes that $200 billion of investment products rely on, reckons ETF providers may end up paying for the privilege of having their products included in customers’ portfolios.

He told a London conference arranged by consultancy firm ETF Strategy this week that index providers may be willing to pay investment firms for the privilege of providing the benchmark underlying a high-profile ETF program. The money managers could, in turn, pass that income on to the buyers for their products – raising the prospect that investors could get paid for buying the ETF. The product would then be a loss-leader, but would allow the firm to sell more lucrative services to the same clients in future, and to generate some income for themselves by lending the stocks the ETFs are invested in.

That less-than-zero fate is one that the ETF providers who spoke at the conference are keen to avoid. Speaker after speaker stressed the need to excite clients about factor-based strategies that try to deliver customized solutions, research-enhanced products that try to beat corporate bond indexes, and other actively managed and higher charging flavors of ETFs – in fact, anything but the passive, low-cost, market-capitalization based index-tracking funds that the industry’s success is built on.

European investment firms are, rightly, under increased regulatory scrutiny for how much they charge for their savings products. The days of high fees and opaque pricing are coming to a close, if they haven’t already ended. While Europe’s ETF creators may want to maintain higher margins than their U.S. peers, they may be too late – a welcome development for anyone trying to build a retirement nest egg, but not so good news for the beleaguered asset management industry.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.