If the Stock Market Has a Problem, His Job Is to Fix It

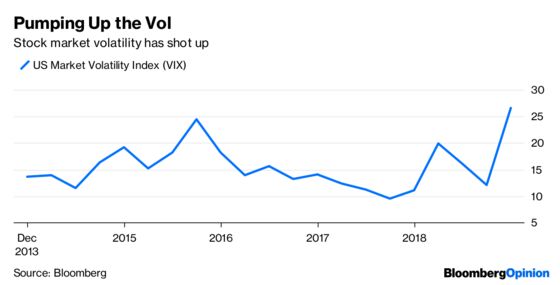

(Bloomberg Opinion) -- It’s harder these days to find reasons for stocks to rise. But the recent 5,000-point market plunge, and seemingly daily swings, when consumers are still spending and the unemployment rate is at historical lows, has more and more people thinking that it’s not the economy that is broken but the market.

Last month, Treasury Secretary Steven Mnuchin blamed high-frequency traders and the Volcker Rule, which restricts trading by large banks, for the market’s volatility. Better Markets, a nonprofit group that advocates for more market regulation and is not normally aligned with officials from the Trump administration, seems to agree. The group has called on the Securities and Exchange Commission to start monitoring for signs the market is being impaired by new trading systems. “Computer-driven, high-frequency algo trading has been driving market drops, swings and volatility for too long. The damage to investors and our economy has been incalculable,” Better Markets CEO Dennis Kelleher said in a statement.

And even before the recent volatility, SEC Chairman Jay Clayton had linked the drought in initial public offerings to a perception that public markets were essentially rigged against “Mr. and Mrs. 401(k).” Making markets appear more fair, Clayton has said, will bring back IPOs and the economic opportunity they create.

If there is a problem with the stock market, the person in charge of fixing it is a former political science graduate student who once led student efforts against nuclear waste and took a year off from college to travel the world with his guitar. Brett Redfearn, who graduated from Evergreen State College in 1987 and then earned a master’s degree in political science from the New School for Social Research, was named head the SEC’s division of markets and trading in October 2017. Since then, he has become, at least on Wall Street, one of the most divisive market regulators under President Donald Trump.

Investor advocates have hailed Redfearn, a former JPMorgan Chase & Co. executive who has long specialized in market structure, as the first regulator in years who puts individual investors first. “It was a room driven by conflicts of interest,” said former Senator Ted Kaufman of Delaware, who served on a panel on market structure during the Obama administration. “That was not the case with Brett.” Officials from the main stock exchanges, though, have a different view of Redfearn. They contend Redfearn has little care for fairness and is just trying to rewrite the rules to boost the profits of his former employer and other large banks.

Redfearn and the SEC declined to comment.

But even if Redfearn’s proposed reforms come with good intentions, some seem positive they will do little to address the market’s growing volatility or the lack of IPOs. “Market structure is about the 13th most important contributor to the lack of IPOs,” said University of Florida finance professor Jay Ritter, an expert on initial public offerings. “It has contributed to perhaps one less IPO a decade.”

Redfearn has long been one of Wall Street’s top experts on market structure. He was laid off from his first job in urban planning at New York’s Port Authority before landing at the American Stock Exchange. “He would take the lead in client meetings even when I was there,” says Sal Sodano, who was CEO of the Amex at the time. Redfearn later went to Bear Stearns and joined JPMorgan when it bought Bear in the run-up to the financial crisis. At JPMorgan, he wrote a widely followed newsletter on market structure.

Now at the SEC, the issues that Redfearn is tackling have been around for a while. In mid-2009, Senator Chuck Schumer of New York called on the SEC to outlaw a technique, called flash orders, that some argued unfairly allowed certain traders to see the buy and sell intentions of others before the rest of the market. It was only one of the techniques that high-frequency traders used, but the name stuck. A few years later, Michael Lewis wrote “Flash Boys” and the controversy over high-frequency went high pitch. Lewis called the market rigged. Mary Jo White, the head of the SEC at the time, pledged to investigate but in the end did little to curtail high-speed traders.

Redfearn, on the other hand, seems intent on taking action. Brad Katsuyama, who founded the upstart exchange IEX Group and is the hero of “Flash Boys,” is a Redfearn fan. “I know the exchanges are pushing the narrative that Brett is conflicted, but it is counterfactual,” Katsuyama said. “The exchanges should be held to a higher standard. Brett has a lot of support and a long-term track record of protecting the interests of investors.”

Redfearn’s most controversial proposal, which would affect the trading of hundreds of stocks for as long as two years, is a pilot program that would limit the incentives — in the form of rebates — that exchanges pay to attract trades. Critics contend the system of access fees and rebates, for which the exchanges typically charge a stock buyer 30 cents for every 100 shares, and rebate as much as 27 cents of that fee to the seller, or vice versa — lead brokers, particularly those who cater to individual investors, to send their trades to exchanges that offer the highest rebates but not necessarily the best price. The difference in price is likely cents or less, but that adds up on millions of trades, which is why many individual investors don’t notice.

A number of large pension funds and mutual fund companies support the pilot program, which has been approved but has no official start date. Others say it’s unnecessary. Virtu Financial Inc., one of the largest high-frequency firms, argues it will be disruptive and that the rebates improve the prices that individuals receive, not the opposite. Brokers say the rebates don’t alter where they send trades. The exchanges say they, like any other company, should have the right to price their products as they like. But at the very least, the access fees that are largely rebated seem like the equivalent of duct tape — a messy and incomplete solution to the real problem, which is that equity markets left largely alone have evolved into a complicated and fragmented mess.

Redfearn has also caught ire from the exchanges for questioning the fees they charge for data, which many contend are too high and a result of the duopoly hold Nasdaq and the New York Stock Exchange have on stock markets. Redfearn has been a vocal critic of those data fees for years, something that has won him friends even among the high-frequency trading crowd. “He’s invited everyone to the table, and there has been some heated discussions,” said Kirsten Wegner, the CEO of Modern Markets Initiative, a group that advocates for the interests of high-frequency trading firms. “He’s done a great job, but he’s going to have a busy next year.”

The biggest question is whether any of these changes will make markets fairer. With Uber and other prominent private companies considering going public, the IPO market seems to be on the upswing. What’s more, investors pay far less than they did to trade even a decade ago, so it’s hard to argue they’re getting a raw deal. And achieving a truly level playing field between average investors and professionals, who spend millions on data and computing power, is most likely an unrealistic goal. But for markets to appear fair, investors need to have a regulator who is putting in some effort seek it. And whether Redfearn finds the right balance, it’s clear that he is looking. In the end, that could be the most important thing he does.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.