India Should Have Learned From Walter Bagehot

Almost 150 years later, Walter Bagehot’s advice on how to deal with a liquidity crisis still rings true.

(Bloomberg Opinion) -- Almost 150 years later, Walter Bagehot’s advice on how to deal with a liquidity crisis still rings true. The problem, as India found out last month, is in implementing it.

Bagehot wrote in his 1873 treatise “Lombard Street” that central banks should curb panic by lending “quickly, freely and readily” to any bank that can offer “good securities” as collateral.

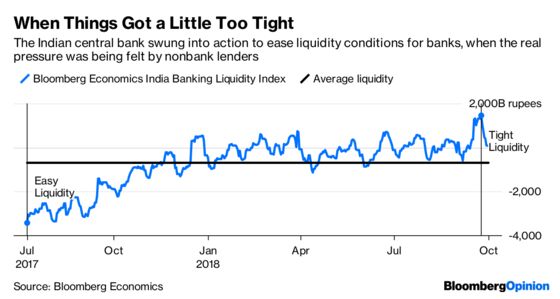

When the sudden insolvency of IL&FS Group, an infrastructure lender, spread panic through India’s money and equity markets, the Reserve Bank of India had no qualms about acting on the first part of Bagehot’s prescription. The trouble came with Part 2: The good securities against which the central bank could lend didn’t exist.

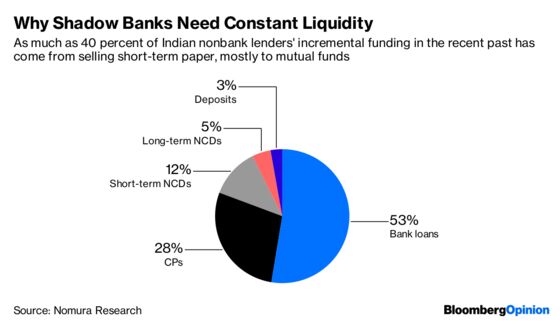

Shadow banks in India have amassed large balance sheets, pumping out 30 percent of all the new credit in the economy over the past three years, according to Nomura Research. But their assets can’t be easily pledged even in normal times.

To see why, look under the hood of their rapid growth. Housing-finance and other nonbank lenders stepped in as state-run banks retreated under the weight of surging nonperforming assets. But unlike banks, shadow lenders didn’t have access to household deposits. So they became increasingly reliant on wholesale funding. Four years ago, only 12 percent of these specialist financiers’ loan books were funded by commercial paper and non-convertible debentures maturing in less than a year. CP and short-maturity NCDs now account for 21 percent of funding, according to Nomura’s Adarsh Parasrampuria and Amit Nanavati.

Almost all of this money came from mutual funds, which have picked up 97 percent of the shadow lenders’ CP and 78 percent of their NCDs since March 2017. Those funds, in turn, raised the bulk of their money by getting businesses and high-net-worth individuals to park surplus cash with them.

Notice how disconnected all this is from the ultimate loans, which may have facilitated a subprime mortgage, met the working-capital needs of a small business or, in the case of IL&FS, gone into the construction of a road, tunnel, or power plant. The funding chain, however, depends entirely on the creditworthiness of the shadow banks. So if the RBI were to step in and lend to mutual funds against their holdings of CP and NCDs, it would essentially be accepting credit ratings as collateral.

But ratings, which can be AA one day and jump to default the next, hardly meet Bagehot’s test of a good security — something that’s “commonly pledged and easily convertible” in normal times.

Ultimately, India dealt with the IL&FS debacle by firing its management and guaranteeing its $12.5 billion debt. That should soothe investors’ nerves for now. However, there has to be a less expensive, more durable solution to deal with future liquidity episodes.

As I’ve written before, India’s shadow banks need to securitize more of their loans. Not only would this give weak state-run banks an avenue to profitably deploy their surplus deposits, the asset-backed securities would also be good collateral, as financial consultant Harsh Vardhan argued in a BloombergQuint article.

The market in securitized claims can also freeze, like the $350 billion contraction in the U.S. asset-backed commercial-paper market in the final five months of 2007. But in that case, the Indian central bank would need simply to emulate the Federal Reserve and start accepting paper that’s underpinned by something more valuable than an opinion.

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2018 Bloomberg L.P.