(Bloomberg Opinion) -- The Financial Conduct Authority has been investigating the U.K. investment management industry. At each step, the behavior it has uncovered might politely be termed sharp practice. The latest broadside from regulators, over how the trustees of the nation’s 1.6 trillion pounds ($2 trillion) of pension assets are served by their advisers, is similarly damning.

The FCA asked the Competition and Markets Authority to investigate whether the market for the consultants used by pension funds is working properly. The watchdog’s report, published on Wednesday, found “substantial customer detriment” in the way advisers and fiduciary managers ply their trades. And, as is all too often the case in money management, opacity in the fees charged is the root issue.

Once the trustees of a pension fund have decided what returns they need to seek and how much risk they are willing to take, they can delegate their other responsibilities to a fiduciary manager. Selecting external asset managers, withdrawing funds from underperformers, and switching money between asset classes are among the day-to-day duties that can thus be delegated.

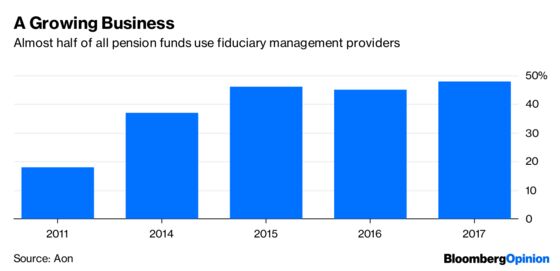

Fiduciary management has become an increasingly lucrative business as pension fund trustees realized that rather than investing the funds themselves they needed more professional help in safeguarding the nest eggs of their members. The CMA calculates that pension providers have increased their spending on these services fivefold since 2011, with the total cost rising to 250 million pounds in 2017.

Almost half of pension fund managers surveyed by Aon Plc used such providers last year, up from 18 percent in 2011. For more than two-thirds of firms, their biggest concern was the difficultly of comparing different firms’ services.

The scope for conflicts of interest when a single firm acts as both investment consultant and fiduciary manager is obvious. The provider will effectively be haggling with itself when negotiating what fees are charged for running a portfolio. If performance disappoints, the fiduciary manager would have to fire its own investment management business.

And yet the CMA found that half of pension plans use fiduciary services provided by their existing investment consultant.

“It is difficult for many trustees to access and assess the information they need on the fees of their existing fiduciary manager and to identify if they would be better off using an alternative provider,” the CMA found.

Financial advisory firm Ernst & Young LLP reckons the fiduciary element of the fees paid by pension firms can range from 11 percent to 70 percent of the total levies when combined with investment management charges. And the fees vary widely: when the firm solicited bids for servicing a 50 million-pound pension plan, the divergence in cost was as much as 90 percent.

The system clearly isn’t working. So the CMA recommends that pension managers opting to delegate 20 percent or more of their assets to fiduciary managers should be obliged to hold a competitive tender for the work; and those already paying for the service have five years from when they first appointed a provider to hold a similar beauty contest. That’s a sensible first step.

But the CMA should have done more. It notes that the investment consultancy market isn’t particularly concentrated and that no single firm has a market share of more than 20 percent. So it could have suggested that the FCA make it mandatory for trustees to hire two different firms to separate the day-to-day management of the pension plan’s assets from the actual investment of the funds.

Moreover, the asset management market generally is already shifting toward performance-based fee structures for investment professionals. A similar approach to paying service providers would be welcome.

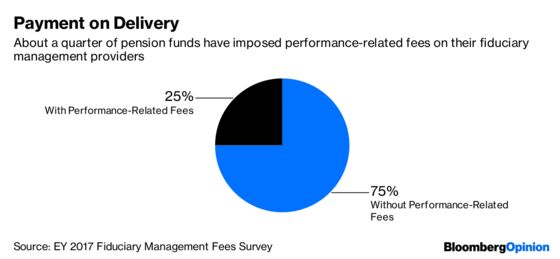

If the choices made by fiduciary managers erode the returns available to pay pensioners, their income should suffer a similar reduction. As the chart above shows, a quarter of pension funds have already achieved this, suggesting the industry is open to the idea.

Granted, designing such fee structures is tricky. But by making such performance-linked provisions mandatory, U.K. regulators would show they are serious about preventing consultants from fleecing their clients and forcing them to align their interests with those of the customers they profess to serve.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2018 Bloomberg L.P.