Hong Kong IPO Roulette Has Top Money Managers in a Spin

(Bloomberg Opinion) -- Some of the world’s largest asset managers took a spin on Hong Kong’s IPO roulette wheel, and now they’re stuck.

Shares of Meituan Dianping dipped below their offering price on Wednesday, barely one week after trading started. Demand from global investors helped the Chinese restaurant review and delivery company price at the top end of its IPO range, raising $4.2 billion.

Institutional investors who hoped to make a quick buck must be disappointed. Earlier public offerings priced at the upper end of their ranges did much better. China Literature Ltd., a spin-off of Tencent Holdings Ltd., rose as much as 89 percent in its first week. Even Xiaomi Corp., which sold at the lower end, managed a 27 percent gain.

This shouldn’t have come as a surprise. Retail investors certainly aren’t feeling the Meituan buzz. They took up only 1.5 times the total amount of shares available to them, and are even less likely to buy in the open market now.

The more interesting question is: Knowing all that, why are foreign funds still buying?

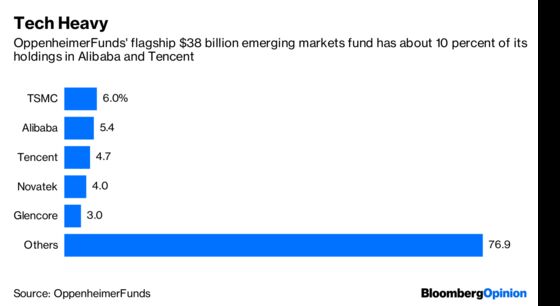

Diversification, perhaps. OppenheimerFunds, with more than $248 billion of assets under management, was a cornerstone investor in Meituan’s IPO. The $38 billion Oppenheimer Developing Markets Fund, for instance, might easily have sold stock in Alibaba Group Holding Ltd. and Tencent — in which it’s overweight relative to the MSCI Emerging Markets Index — to fund its $500 million investment in Meituan.

As for the smaller funds, they may be buying simply to maintain cozy relationships with their brokers. Many managers, I was told, get involved in every tech IPO to keep on a bank’s good side, so when a hot offering or block trade comes along, they get the first call. The Meituan flop might have been a small price to pay for more lucrative deals to come.

Except that there may not be many more such deals.

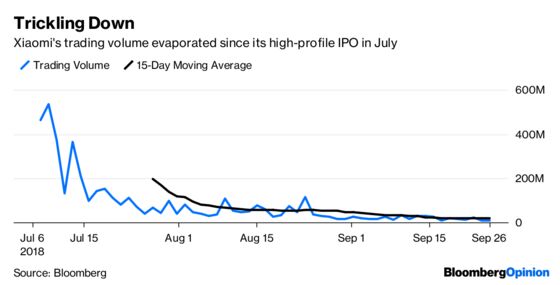

Hong Kong’s IPO window is closing fast, as evidenced by dwindling liquidity and the narrowing investor base. China Literature’s 86 percent pop in its November 2017 debut netted retail investors as much as a $90,000 profit in one day. In the last three months, however, trading has averaged only $14 million a day. Xiaomi’s liquidity has evaporated since its July listing.

It’s well known that Hong Kong’s most recent tech IPOs have languished, with many below their offering prices. But in the current liquidity drought, even managers willing to sell at a loss might struggle to find a buyer.

Take Meituan again. Citic Securities Co. tech analyst Jiang Ya, who has a buy rating on every one of the 47 stocks he covers, assigned Meituan a HK$78 price target, suggesting only 16 percent upside. And on the downside, investors could be staring at cash burns and a valuation landslide. Ahead of Meituan’s IPO, Alibaba’s Jack Ma merged his delivery units and injected more than $3 billion into them, preparing for another price war.

Looking back to early 2012, when blue-chip Tencent was valued at $47 billion (where Meituan is now), it was increasing sales by more than 50 percent a year and generating a 30 percent net income margin. Meituan, on the other hand, is still in the red.

Buying into IPOs is hard work. Investors must absorb hundreds of pages of a prospectus, attend roadshows and write in-house analyst reports. The effort is starting to look like a waste of time. Soon, even the most loyal funds might be abandoning their bankers.

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2018 Bloomberg L.P.