Hong Kong’s Latest Move Will Stir, Not Shake Singapore

(Bloomberg Opinion) -- Charles Li, chief executive of Hong Kong Exchanges & Clearing Ltd., has his plan at the ready. An agreement with MSCI Inc. is in the bag. Once regulators bless the idea, he will give futures contracts on China’s A-share index in the city a go.

One place where Li’s announcement was received with some trepidation was the rival financial center of Singapore, where investors drove shares down as much as 4 percent on Monday.

But is it game over for Singapore Exchange Ltd.’s FTSE China A50 Index Futures, which the city landed back in 2006 as the first internationally available, dollar-denominated futures contract on mainland stocks? Recall this was when Beijing’s then three-year-old Qualified Foreign Institutional Investor program gave foreigners only tightly restricted access to yuan-denominated local A shares. Back then, global investors considered H shares, freely traded in Hong Kong, their entry point to China’s equity market.

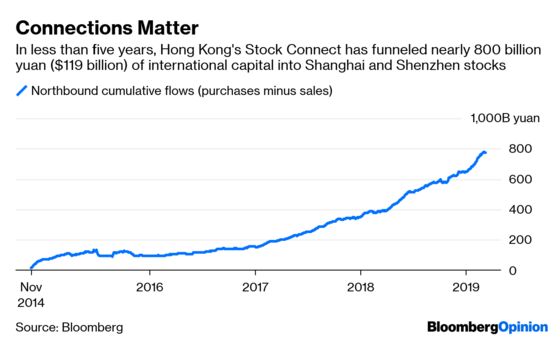

It was only in late 2014 that international investors got Hong Kong’s Stock Connect to invest directly in Shanghai’s A shares; a similar pipe to the Shenzhen market was established two years later.

And then came the payday for Singapore’s patient bet that, albeit in fits and starts, China would open up its markets.

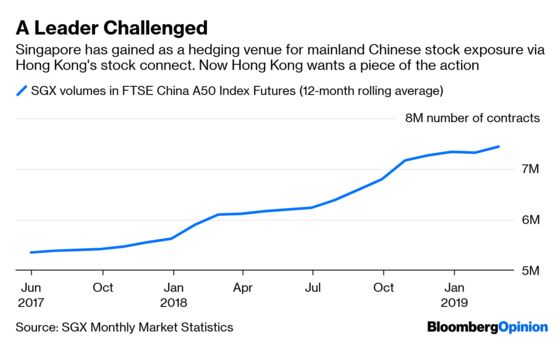

Over the past year, an average 7.4 million contracts have changed hands on SGX-listed FTSE China A50 Index Futures every month, a 22 percent jump from a year earlier. Open interest at the end of February was up 67 percent at 959,080 contracts, worth $12 billion at current prices. Add the less popular SGX MSCI China Free Net Total Return Index Futures, and open interest rises to $15 billion. SGX investors are now jittery that Hong Kong is making a play for this bounty. After Citigroup Inc. downgraded SGX stock to sell from neutral, it fell more on Tuesday morning.

At HKEX, Li is targeting the hedgers. Goldman Sachs Group Inc. estimates MSCI’s recent decision to boost the weighting of A shares in its China and emerging-markets indexes will pull a fresh $60 billion into mainland stocks. For investors using Stock Connect, it makes sense to buy protection in Hong Kong.

Yet Singapore still has its advantages. An investor in mainland stocks who also wants to profit from the yuan wobbling — or iron ore prices fluctuating — while seeking a cushion against whiplash in the equity market may be tempted to keep using Singapore. Not only is the city-state a bigger venue than Hong Kong for trading the offshore Chinese yuan, via CNH futures, SGX also allows margins on future trades to be offset across asset classes, leading to savings. SGX is already popular with Chinese firms for hedging the price risk on their iron-ore imports from Australia and Brazil.

Think of SGX as the Best Buy Co. of riskier derivatives whereas the HKEX Stock Connect is the Costco Wholesale Corp. of vanilla Chinese cash equity. Yes, some shoppers will come for the $4.99 Costco rotisserie chicken and go home with a flat-screen TV. But that doesn’t invalidate Best Buy’s business model. By the same yardstick, SGX can’t aspire to challenge HKEX in IPOs. That ship has sailed.

No doubt SGX could lose some derivatives market share. Overall, though, more internationalized Chinese stocks will pique the interest of more global investors. Liquidity begets liquidity, and that might be more true if SGX can add mainland fixed-income derivatives. HKEX is also in the race. It wants to reintroduce Chinese treasury bond futures, though the product flopped in 2017.

Singapore could end up a major loser if mainland regulators “do an India” on SGX. Gripped by panic over losing domestic business to overseas venues, early last year Indian exchanges banned use of local securities data by SGX and others. The knee-jerk move led to a most spectacular spat. Wisely, that nationalistic project has been put in cold storage.

Will Beijing borrow a page from that playbook? Perhaps not. Obtaining more prominence for A shares in the universe of emerging-market stocks is China’s bigger goal, and reducing choices for global investors just as they’re readying to invest more would be self-defeating.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2019 Bloomberg L.P.