Hong Kong Money Is Fleeing? Not Around Here

The IPO market is turning buoyant again after a fraught summer, with a third candidate seeking more than $1 billion.

(Bloomberg Opinion) -- Hong Kong may have been seeing money flow out as the city’s turmoil undermines its reputation as a stable financial center, but one important source of capital keeps on coming: cash for initial public offerings.

The city has hosted two IPOs of more than $1 billion since early June and ESR Cayman Ltd. is testing investor appetite for a revived share sale of as much as $1.45 billion. The Hong Kong-based warehouse operator, which is backed by Warburg Pincus and Goldman Sachs Group Inc., delayed its IPO in June citing unfavorable market conditions. It has now increased its fundraising target from $1.24 billion.

ESR is the second company to resuscitate a flotation since June, when large-scale protests started to affect Hong Kong. Budweiser Brewing Company APAC Ltd. completed a $5 billion offering last month, having shelved its sale in July amid lackluster demand. The Asian unit of Anheuser-Busch InBev NV almost halved the size of the IPO from a planned $9.8 billion. The stock has risen 15% since it started trading at the end of September.

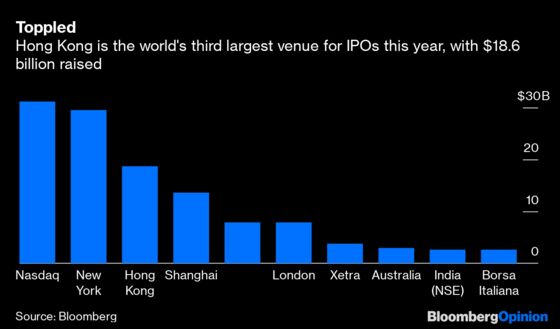

While Hong Kong has slipped from being the world’s largest IPO venue last year, it’s still running in third place in 2019 behind the Nasdaq and New York exchanges, with companies having raised $18.6 billion in the city, according to data compiled by Bloomberg. That testifies to Hong Kong’s enduring strength as a capital-raising hub, an advantage that won’t easily be prized away by any regional rival.

The bottom line for companies such as ESR is that they have few other choices. Hong Kong has Asia’s deepest stock market bar Tokyo, where investors are mostly domestically focused and few foreign companies opt to list. Singapore, meanwhile, has been bedeviled by a lack of liquidity. The city’s market capitalization has shrunk to $478 billion — smaller than Thailand’s and less than a 10th of Hong Kong’s $5.2 trillion, according to Bloomberg-compiled data.

Hong Kong-traded Fortune Real Estate Investment Trust withdrew its dual listing from Singapore’s main board in June, citing costs of compliance and low trading volumes, one of a number of companies to have abandoned the exchange. Singapore is the world's 12th largest venue globally for IPOs this year, behind even Borsa Italiana and SIX Swiss Exchange. Even well-known Singapore names have been looking to sell shares elsewhere: PropertyGuru Ltd., an online real estate classifieds business backed by KKR & Co. and TPG Capital, had been looking to list in Australia, before withdrawing an expected $260 million IPO on Wednesday.

A mild recovery in Hong Kong share prices has given companies confidence to venture back, with the benchmark Hang Seng Index climbing about 5% from its August low. And positive post-IPO performances are helping to bolster investor interest. Besides Budweiser, Chinese sportswear retailer Topsports International Holdings Ltd. has climbed 15% since raising $1 billion this month.

A peculiarity of the Hong Kong market has also aided the return of Budweiser and ESR: the cornerstone investor. Budweiser sold a $1 billion stake to Singapore’s sovereign wealth fund, while Canadian pension fund OMERS has committed $585 million to ESR’s offering. First time around, neither company had cornerstones — big investors that commit to hold the shares for a minimum period, signaling confidence to other buyers.

ESR, which has logistics assets in countries from China to India, is seeking to sell stock at a premium to its bigger, Australian-listed competitor Goodman Group. At the bottom of its targeted price range, ESR is priced at 26.1 times its estimated 2020 enterprise value to Ebitda, according to Aequitas Research analyst Sumeet Singh, who writes on Smartkarma. Goodman is trading on a ratio of 21.8 times, according to Bloomberg-compiled data.

That looks ambitious, though it may reflect the return of more buoyant conditions to the Hong Kong market. A successful sale is likely to encourage more listing candidates to tiptoe back.

--With assistance from Zhen Hao Toh

The market capitalization figures for Singapore and Hong Kong don't include ETFs and ADRS, and include only actively traded, primary securities on the two exchanges to avoid double counting. Including secondary listings, Hong Kong's market cap is $6.1 trillion, versus $672 billion for Singapore.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.