(Bloomberg Opinion) -- Whenever a Japanese company acquires an overseas asset, the rationale is typically that it’s finding a way to survive the country's aging demographics and shrinking returns.

But Hitachi Ltd.'s 800 billion yen ($7.06 billion) purchase of ABB Ltd.'s power-grid business is bigger than that. The deal, while on the expensive side, is high-margin for the Japanese industrial conglomerate, and could catapult it into the big leagues of power equipment globally.

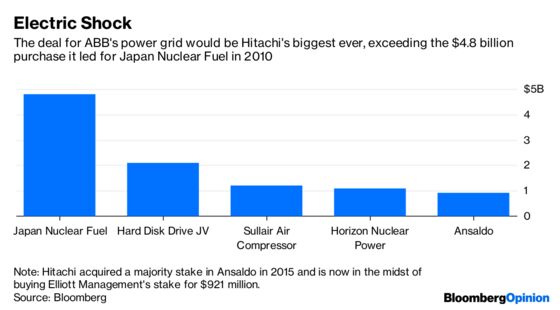

Hitachi is nearing an agreement to buy 80.1 percent of Swiss engineering giant ABB Ltd.’s power-grid unit, in a deal that values the entire business at $11 billion. ABB has an option to sell its 19.9 percent stake three years after the current deal – Hitachi's largest-ever purchase – is completed. In its statement, ABB noted that Hitachi would help provide access to new markets as well as financing.

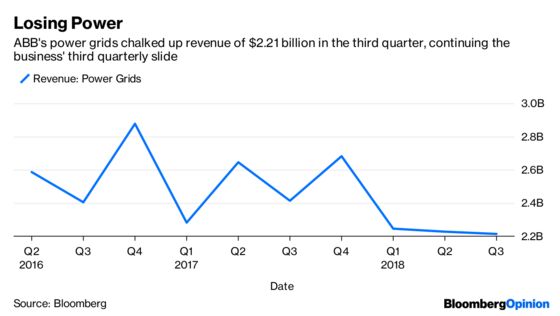

ABB investors have long been underwhelmed by the power-grid business, which is low-margin compared with the Zurich-based firm’s robotics and factory automation operations. On a sum-of-the-parts basis, the unit trades at around 9.8 times forward enterprise value-to-Ebit, weighing on the Swiss conglomerate’s overall multiple of around 12 times. Last year, power grids carried ABB’s lowest return on assets.

Combined with the Japanese conglomerate’s other industrial-equipment business, ABB’s power grids will allow Hitachi to compete neck-and-neck with General Electric Co. and Siemens AG.

With ABB’s power grids under its belt, Hitachi also could avoid the fate of so many other global industrial companies, which have struggled to turn their businesses around. As Japanese conglomerates increasingly talk about reforming to extract more value and shed the Japan discount, Hitachi has been ahead of the pack – selling units that no longer fit its strategy and putting more cash to work.

Hitachi has almost 800 businesses spanning everything from construction machinery to nuclear power plants and healthcare. It’s now cutting its subsidiaries by 40 percent to 500 companies, as the Nikkei reported earlier this year, and aims to focus on four core areas, of which power and energy is one.

Buying ABB brings Hitachi closer to its consolidated operating margin target of more than 10 percent by 2022, compared with 8 percent for the group and 6.5 percent for the power business currently. Other targets loom, too: The Japanese company is looking to almost double the sales in its power segment to more than 800 billion yen by March 2022 from around 450 billion yen.

ABB's power grids will give Hitachi much-needed exposure overseas that past purchases haven't quite succeeded at, especially after the company broke up its thermal-power business last year. Overseas sales made up just 3 percent of its nuclear subsidiary and 9 percent of other power units, according to Nomura Research analysts.

In getting its hands on more of the world's electricity-grid makers, Hitachi is acquiring an edge in the future of power. With its equipment, it could help drive the global shift from coal and nuclear, and answer calls for systems that can carry renewable energy.

Much of Hitachi’s mid-term plan is focused on this shift. ABB also has the kind of exposure to emerging markets Hitachi would love. And crucially, the $1.1 trillion Internet of Things market will need equipment to power it.

To be sure, execution is key. Hitachi’s overseas adventures have a reputation for being pricey, as it suffered rising indirect expenses from its deals. The fate of its nuclear plant in the U.K. and the potential funding difficulties it faces there have weighed on the stock. The company will have to show shareholders that this time is different.

But done right, Hitachi may just have found more than just an out from Japan.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2018 Bloomberg L.P.