(Bloomberg Opinion) -- After a harrowing end to 2018, U.S. stocks have staged a fierce comeback. The S&P 500 Index notched a record high on Friday and extended its advance on Monday. It is up 25 percent from its Christmas Eve nadir, placing the 85-day advance among the top 2 percent strongest rallies since 1928. Predictably, bulls and bears are already arguing about the market’s next move.

The debate may be entertaining, but it’s also beside the point. For many investors, whose time in the market numbers in years rather than months, the more useful question is how stocks will fare over the longer term, and the most likely answer is not well.

The reason is that U.S. stocks are expensive, thanks to a historic rally in which the market has more than quadrupled in value since the financial crisis eased in March 2009. And as investors are constantly told but never quite seem to believe, frothy stock prices tend to be followed by subpar returns.

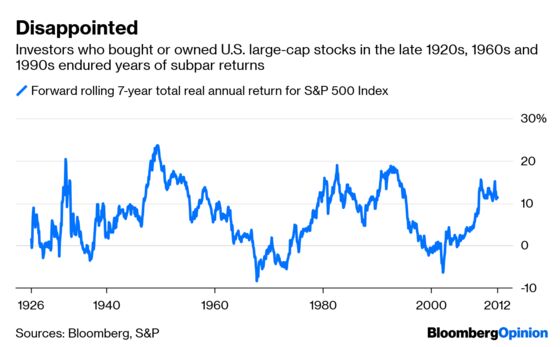

Previous episodes are instructive. The market nearly quintupled in value during the Roaring ’20s, and stock prices were famously rich by the end of the decade. Investors who managed to hang on during the subsequent plunge that accompanied the start of the Great Depression didn’t lose much, but they weren’t rewarded for their bravery, either. From the late 1920s to the mid-1930s, the real, or inflation-adjusted, total annual return for the S&P 500 was essentially flat.

It happened again four decades later when the market jumped more than six times in value during the 1950s and 1960s, driving up valuations to heights not seen since the 1920s. Investors who bought or owned the S&P 500 during the late 1960s through mid-1970s endured modestly negative real annual returns for many years afterward.

Three decades later, the market quadrupled during the 1980s through the mid-1990s. Then came the dot-com mania, and the S&P 500 tripled in value from 1995 to 1999. By the time the two-decade-long bull market ended in early 2000, the market had surged more than 12 times in value, reaching the highest valuations on record. And yet again, the S&P 500’s real annual return was flat for much of the decade that followed.

That repeating pattern is not a coincidence. To see why, it’s helpful to look at three variables that drive returns: real earnings growth, dividend yield and change in valuation. All three smiled on investors in recent years, as they did in previous bull markets.

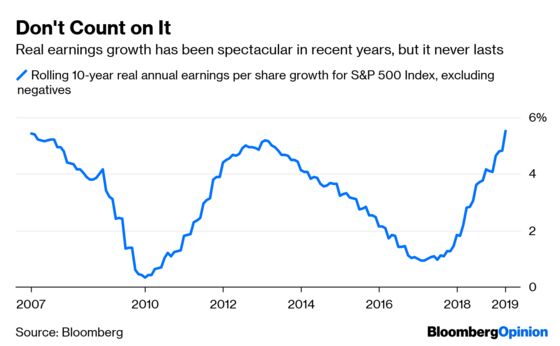

Consider that the S&P 500 returned 13.9 percent a year over the last decade through March, net of inflation and including dividends. Over the same time, real earnings grew by 5.5 percent, the dividend yield averaged 2.1 percent, and the 12-month trailing price-to-earnings ratio, excluding negative earnings, expanded to 18.5 from 10.5, reflecting investors’ growing affection for stocks and adding another 5.8 percent. The sum of those three variables is 13.4 percent, which accounts for most of the real annual return from stocks during the period.

The problem is that, while dividends are generally reliable, earnings are not. They’re highly volatile, growing in fits and starts. And as I’ve previously pointed out, earnings have grown at an unusually robust pace in recent years. Real earnings grew by just 1.9 percent a year over the last 150 years, according to data compiled by Yale professor Robert Shiller, well below recent growth rates, which strongly suggests that the current pace isn’t sustainable.

Making matters worse, when growth slows, investors run for the exits. Just as expanding valuations provide a boost, contracting valuations are a drag. And when real earnings growth dips to 2 percent or lower, it doesn’t take much P/E contraction for returns to hang around zero.

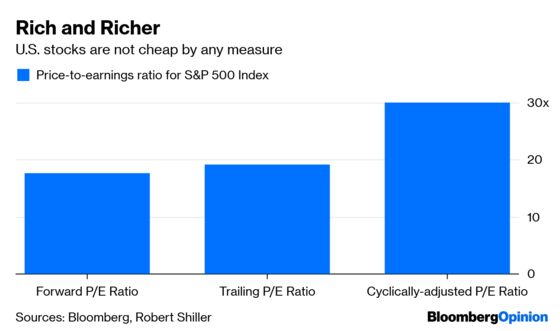

That reality is obscured by arguments about whether and to what extent stocks are too expensive. But even by the most flattering measures, such as price-to-earnings ratios using analysts’ rosy earnings projections, U.S. stocks are not cheap. And according to more conservative P/E ratios that use current earnings or a trailing average of recent years’ earnings, stocks are as pricey as they were in the late 1920s and roughly 40 percent more expensive than in the late 1960s.

That’s why there’s near universal agreement that returns will be lower going forward. Even Wall Street, which rarely lacks enthusiasm for stocks, concedes as much. BNY Mellon and BlackRock estimate that the total return from U.S. stocks will be roughly 6 percent a year over the next 10 years, before inflation, or close to half the S&P 500’s return of 10 percent a year since 1926. JPMorgan estimates that the long-term return from U.S. large-cap stocks will be closer to 5 percent. I suspect the number will prove to be even lower.

That doesn’t mean investors should dump all their U.S. stocks, but it’s useful to have realistic expectations about what’s likely ahead. It may temper investors’ urge to take more risk than they can afford or skimp on saving in the hope that the market will bail them out, or simply prevent surprises that could lead to bad investment decisions down the road.

So while bulls and bears bicker about the market’s path, it’s worth remembering that there’s little disagreement about where it’s likely to end up, which, after all, is the only thing worth talking about.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

©2019 Bloomberg L.P.