(Bloomberg Opinion) -- By the looks of it, investors’ misgivings about Chinese surveillance have taken a backseat.

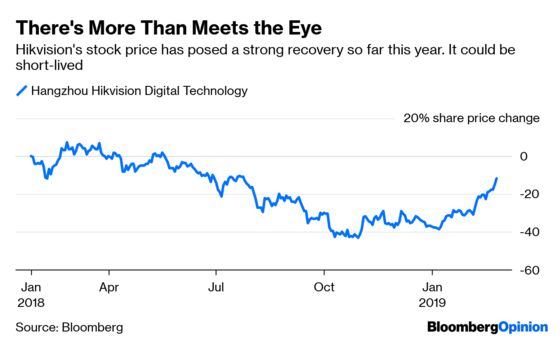

Shares of Hangzhou Hikvision Digital Technology Co. are up more than 50 percent since plumbing lows in October, and have climbed almost 40 percent since the beginning of the year. Yet troubles are piling up for China’s largest spy-tech maker – at home and abroad.

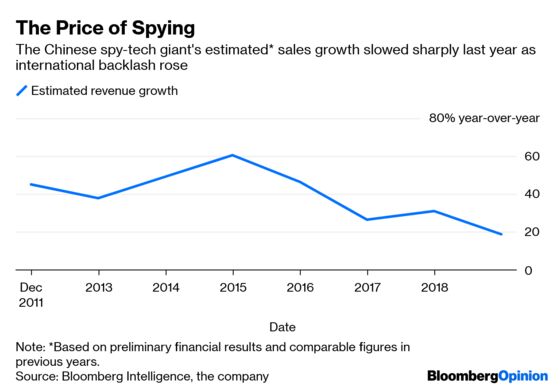

Its financial results show as much. In preliminary numbers released earlier this month, Hikvision’s net profit rose just 20 percent last year, the slowest pace of growth since the company went public in 2010. Sales grew 19 percent, down from 31 percent a year earlier.

Back in September, news that the U.S. was considering sanctions against the spy-gear maker drove its stock lower. Those fears eventually eased as investors and analysts noted the company’s domestic market remains huge: Beijing has no shortage of surveillance needs. Supported by subsidies and other freebies, the company’s success has been tied to its government contracts. Now, around 90 percent of sell-side analysts that cover the stock give the company a “buy” rating.

But state support can have a downside, too. Government-procurement contracts don’t necessarily ensure steady cash flows, especially since Hikvision’s pacts aren’t all long-term. In December, such deals rose 13.2 percent from a year earlier, after dropping each month between August and November. While that figure rose 8 percent in the fourth quarter from a year earlier, it fell 2 percent from the previous period. Beijing’s help is beginning to look like the only driver for Hikvision’s earnings.

Other macroeconomic factors may start to bite, too, as the government reins in spending and balances its priorities. A Goldman Sachs Group Inc. analysis found that Hikvision’s revenue growth lags China’s fixed-asset investment by around nine months: Surveillance equipment tends to get added to infrastructure projects toward the end of construction. The company’s expansion is also correlated with the country’s total credit growth. Both indicators have slowed meaningfully in recent months.

Meanwhile, Hikvision’s other growth plans – to develop Internet of Things products, artificial intelligence-based surveillance cameras and the like – are costly, as is the underlying hardware. Most of the company’s supply chain is spread globally, as we’ve noted, with many parts coming from the U.S. As overseas skepticism grows, it will become harder to source components for the company’s higher-tech cameras.

Hikvision’s operating costs and expenses also have started inching up, making it tougher to maintain those fat margins. At some point, the company’s slowing profit growth may not be able to fuel its lofty ambitions, with its cash flow from operations dropping in the 12 months through Sept. 30, and negative free cash flow in the quarter ended the same date.

Investors shouldn’t take this recent rally for granted. That firm hand seemingly at Hikvision's back may be getting weaker.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2019 Bloomberg L.P.