(Bloomberg Opinion) -- The use of “Earnings Before Interest Tax, Depreciation and Amortization” — Ebitda for short — to measure a company’s performance was popularized during the dot-com bubble of the late 1990s and adopted more broadly by CEOs hoping to sprinkle some sunshine on their results. The metric has its uses, but it doesn’t provide the hard certainty of cash flow.

With corporate debt markets showing signs of increasing strain, it’s useful be reminded again of Ebitda’s weaknesses as a gauge of a company’s health.

Vallourec SA, a provider of steel tubes to the oil and gas industry whose shares were brutalized on Friday, has certainly done that. The French company has had a rotten time of late. Net losses have totaled about 3 billion euros ($3.4 billion) in the past four years as demand for its products collapsed along with oil prices.

Yet with demand recovering, notably in the U.S., its Ebitda rebounded in the first nine months of this year to a modest 61 million euros. Nevertheless, its free cash flow was still negative to the tune of 571 million euros, according to figures published late on Thursday.

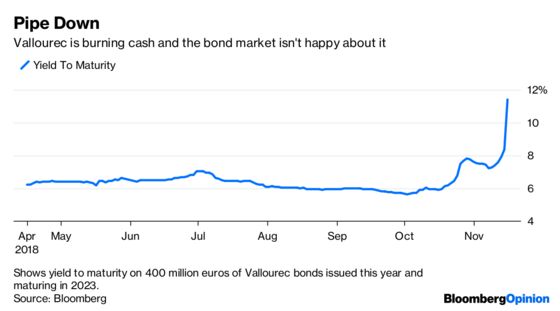

It’s easy to see what figure investors paid attention to. The shares tumbled 22 percent on Friday, bringing the decline since 2011 to 95 percent. Meanwhile, the yield on 400 million euros of five-year Vallourec bonds soared to an eye-watering 11.4 percent. The shares are among the most heavily shorted in Europe, with at least 16 percent of the stock out on loan, according to Bloomberg data.

Even equity analysts are sometimes seduced by companies’ own Ebitda figures, but Vallourec shows clearly why you might not want to do that. When you have lots of debt, as Vallourec and plenty of other companies do, you really don’t want to be burning through too much cash. It only makes things worse. The French company’s net debt has risen again this year to about 2.1 billion euros, much higher than its market value.

Vallourec has done plenty of emergency surgery: The dividend was scrapped in 2016, when it raised about 1 billion euros of fresh capital. It's been busy stripping out costs and cutting thousands of jobs. Unfortunately, interest costs have increased and it is obliged to maintain a certain level of capex spending (explaining part of the cash shortfall.) There are taxes and restructuring costs too, plus the need for working capital. It’s sitting on a lot more inventory because of the U.S. tariffs on steel imports, though the effects should be temporary.

The company would need to report more than 500 million euros of Ebitda to return to positive free cash flow. But the weakness in offshore drilling means analysts don’t think that will happen until 2020, according to the Bloomberg consensus forecast. Cutting that debt will therefore be slow, which will surely keep the hedge funds circling.

Vallourec should be able to keep the lights on for the time being. It has 770 million euros of cash, another 2.2 billion euros of undrawn credit and no debt that needs refinancing until 2022. Management also sounded comfortable about its debt covenants, which are tested at the end of the financial year. Investors don’t appear to be so sure.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2018 Bloomberg L.P.