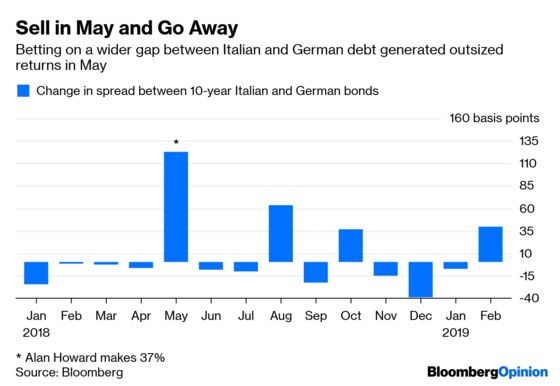

(Bloomberg Opinion) -- Hedge funds had their worst performance since 2011 last year. But amid the gloom, one trade did work and seems poised to generate profits in the coming months: betting against Italian government bonds.

Italy needs to borrow about 250 billion euros ($283 billion) this year. Put another way, it has to sell almost a billion euros of fresh debt every business day of 2019. So it can ill afford to see its funding costs climb – leaving it vulnerable to a renewed attack by hedge funds who doubt the government can maintain any kind of fiscal discipline.

The trigger for the latest jump in Italian borrowing costs is a renewed bout of economic weakness. Figures released on Friday showed industrial production fell for a fourth consecutive month in December. The drop of 0.8 percent confounded economists’ expectations for a 0.4 percent gain. That suggests the recession heralded by the economy’s contraction in the third and fourth quarters of last year may worsen.

On Thursday, the European Commission slashed its 2019 growth forecast by a full percentage point, dropping it to 0.2 percent. And while Europe as a whole is suffering an economic slowdown, the shoe pinches particularly hard for Italy because of tensions over its budget deficit.

A negotiated agreement in December saw the government reluctantly agreeing to a 2.04 percent target; David Powell of Bloomberg Economics reckons the recession could see the budget gap instead rise to the 2.4 percent level that the Commission rejected.

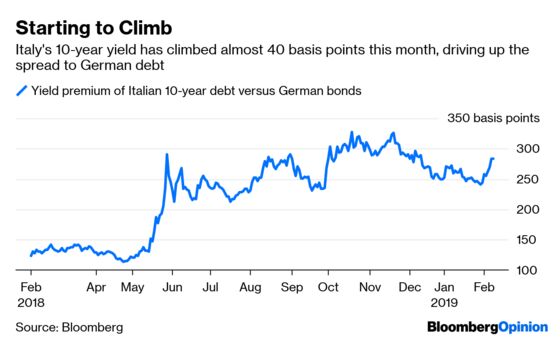

The rise in Italian yields this month reflects investor concern that slippage on the deficit could spark another clash between the government and the Commission. The 40 basis-point widening in the spread between benchmark Italian and German government bonds in just the first eight days of February is reminiscent of the surge that proved very profitable for some hedge funds last year.

For example, Alan Howard, who made 30 percent last year on the pool of funds he manages himself, reaped a 37 percent gain in May, helped by a short position on Italian government debt, according to Bloomberg News.

On the other side of the spread trade, German 10-year yields have plummeted to their lowest since October 2016, and are hovering at just above 0.1 percent. As Italian yields are rising, those on German benchmark bunds look set to rejoin the newly expanded below-zero club. In total, the value of debt with negative yields has climbed by an astonishing 55 percent since the start of October to reach almost $9 trillion, the highest level since the end of 2017.

It may be too soon to bet on the Italian-German yield difference reaching the highs of more than 326 basis points seen in October. As I argued then, Brussels will be wary of taking the government to task ahead of the European elections in May for fear of giving ammunition to the various populist parties taking aim at the European Union’s economic strictures.

But once that vote is out of the way, the tussle over Italy’s deficit will come to the fore once again. At that point, the hedge-fund traders dubbed “the gentlemen of the spread” by Deputy Premier Matteo Salvini last year are likely to smell blood in the Italian bond water once again.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.