(Bloomberg Opinion) -- Usually, escaping a nasty bout of the flu is a good thing.

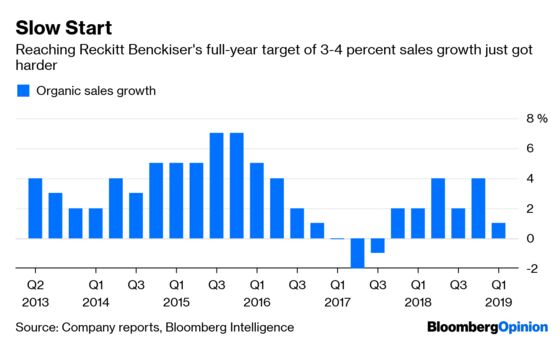

Not for Reckitt Benckiser Group Plc, which reported weaker-than-expected first-quarter sales on Thursday. It turns out fewer Americans came down with the illness, so didn’t need to buy its remedies. In addition, more people are switching to cheaper private-label brands. Like-for-like sales of the company’s over-the-counter medicines fell 9 percent.

To make matters worse, people were less worried about getting sick so didn’t buy as many vitamin supplements. And Scholl, which has been a problem for a while, continued to disappoint.

All this means Reckitt will find it a bit harder to achieve its full-year target of 3-4 percent like-for-like sales growth. Management’s decision to maintain the guidance looks ambitious.

True, it is only the first quarter, and the company has the rest of the year to make up for it. It may get some help from infant nutrition, where sales growth of 5 percent indicates that the division is recovering from a disruption to baby milk supplies last year. It’s a good sign that prices rose 4 percent in the health division, and that the hygiene and home unit is also ticking along nicely.

But Reckitt must still work harder to meet its full-year forecasts.

Over-the-counter medicines tend to have high margins, so weakness here bolsters concerns that Reckitt might not be able to maintain profitability. Outgoing Chief Executive Officer Rakesh Kapoor has avoided sacrificing earnings in order to invest and turbo-charge sales growth, but his successor might not.

Factors other than the quarterly performance are at play.

The first is Kapoor’s replacement. The investment case from here largely rests on who takes over, and his or her new strategy. An announcement could come over the next few months.

Second is the potential for a break-up of Reckitt into its health division and its hygiene and home unit. Analysts at Bernstein said this week that this could be worth as much as 91.20 pounds ($119) per share, depending on how the transaction is structured. That’s well ahead of Reckitt’s current share price of around 61 pounds.

As my colleague Chris Hughes has argued, a split could be hampered by the aftershocks from the Justice Department’s indictment of Indivior Plc, a pharma business Reckitt spun off in 2014 that faces fines related to claims about its opioid addiction treatment. Reckitt on Thursday maintained a provision of $400 million arising from its own related probes and litigation.

If a break-up is further away, that makes Reckitt’s current path even more of a grind. It’s an ailment which has no immediate remedy.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.