Global Equities Confront Uncomfortable Truth

(Bloomberg Opinion) -- A strong performance in July allowed the MSCI All-Country World Index of stocks to end a month in the black for the year for the first time since January, gaining 1.7 percent. Strip out U.S. equities, though, and the benchmark is still showing a loss of 3.39 percent for 2018. Therein lies a big problem.

Outside of strong earnings in the U.S. and a few other places, there’s not a whole lot to get excited about in the global equities market. Of the 95 global equity indexes tracked by Bloomberg, only 33 are positive year-to-date. This time last year, 81 were showing gains. “That kind of narrow leadership usually doesn’t last,” the strategist at Richardson GMP wrote in a research note Wednesday. “So either other markets have to step it up or there could be trouble.” Judging by the latest economic data, it’s more likely that trouble erupts than markets outside the U.S. step it up. Reports on Wednesday showed factory activity in the U.S., Europe and Asia-Pacific region slowed last month, and companies are issuing warnings about the impact of tit-for-tat battles over import tariffs on their profits, according to Bloomberg News’s Carolynn Look and Shobhana Chandra. The data suggest that protectionist threats are starting to weigh on global growth, they report.

“Weaker expectations for global trade are clearly feeding through to production,” Stefan Schneider, chief international economist at Deutsche Bank, told Bloomberg News. “Particularly in many open economies, such as Germany, but also Japan and Korea, weaker expectations for exports weigh on investment activity.” Even in the U.S., where growth has been hot, there are some worrisome signs. Although ADP Research Institute said Wednesday that private payrolls rose by 219,000 last month, up from 181,000 in May, big international companies actually slowed their hiring. Businesses with more than 1,000 employees added just 24,000 jobs, down from 46,000 the prior month and the fewest since May 2017.

METALS MARKET GETS IT

Worries about the global economy can be seen clearly in the markets for so-called base metals such as copper, aluminum, nickel and zinc. These raw materials are the building blocks of an economy, and a drop in prices can signal a drop in demand from end users. The Bloomberg Industrial Metals Subindex fell as much as 2.62 percent on Wednesday, its biggest drop since April, as a result of what some strategists said were inflammatory comments on trade between the U.S. and China. Bloomberg News reported that the Trump administration is considering more than doubling its planned tariffs on $200 billion in Chinese imports, ratcheting up pressure on Beijing to return to the negotiating table. China responded by warning the U.S. against “blackmailing and pressuring” it over trade. “As long as tariffs are allowed to metastasize, they do have the potential to do real damage to the global growth story,” Edward Meir, an analyst at INTL FCStone, wrote in a research note Wednesday. The Economic Cycle Research Institute has an index that tracks nontraded industrial commodities. That gauge has fallen to its lowest since April 2016 in an ominous sign for the global economy.

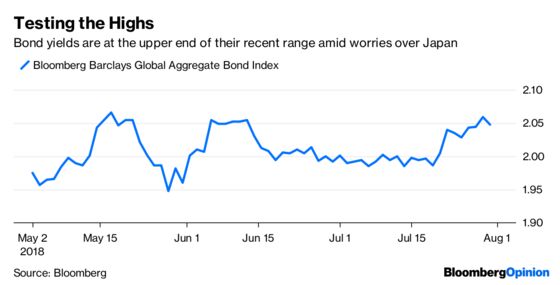

IGNORE JAPAN AT YOUR OWN RISK

Japan’s bond market is going haywire, and it could have global implications. Moves in 10-year government debt futures were so extreme on Wednesday — a drop of as much as 0.5 percent, the most in almost two years — that they triggered an emergency margin call from the clearinghouse, according to Bloomberg News’s Chikako Mogi. This is all because the Bank of Japan said this week that it would allow 10-year yields to rise to 0.2 percent after capping them at 0.1 percent. Investors are concerned that this is the BOJ’s first step to extract itself from markets. No central bank is as intertwined in its markets as the BOJ. It owns so many government bonds that on some days none are available to be traded. The concern is that domestic yields will rise to a level that will entice Japanese investors to bring back the trillions of dollars they have sent overseas. That would cause longer-term bond yields in places such as the U.S and Europe to surge as the Japanese sold. It’s understood that low long-term rates have helped fuel the second-longest bull market in U.S. stocks as well as a general rally in riskier assets globally. So if long-term rates start to rise, riskier assets could most likely take a pretty big stumble.

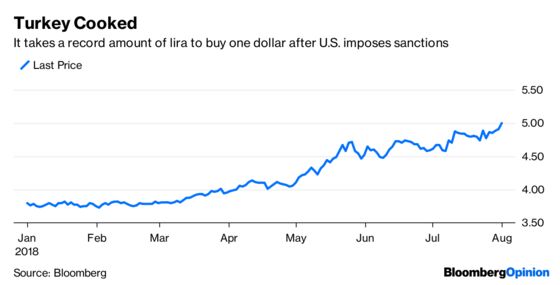

TURKEY GOES FROM BAD TO WORSE

The Turkish lira has been hit hard this year, dropping 23 percent against the dollar through Tuesday as President Recep Tayyip Erdogan tightened his grip on power, installed his son-in-law as the economy czar and the central bank failed to raise interest rates. The currency’s losses grew another percentage point on Wednesday as the lira fell to a record low after the U.S. sanctioned two senior Turkish government officials over the continued detention of an American pastor. At about $851 billion, Turkey’s economy and external debts are big enough to be worrisome. The extent of the damage on the nation’s financial system caused by the lira’s decline may be revealed in coming days as Turkish banks report second-quarter results. Profits are expected to drop 5 percent on average from the previous three months, according to data compiled by Bloomberg based on the median estimates of the six-biggest publicly traded lenders. Of specific interest will be what banks say about the ability of borrowers to repay foreign debt, which has only become more expensive with the lira’s decline, according to Bloomberg News’s Asli Kandemir and Constantine Courcoulas. “Given Turkey’s external financing requirement, policy credibility may be crucial to avoiding disorderly asset price moves if the external environment deteriorates,” the currency strategist at Goldman Sachs Group Inc. wrote in a research note last week.

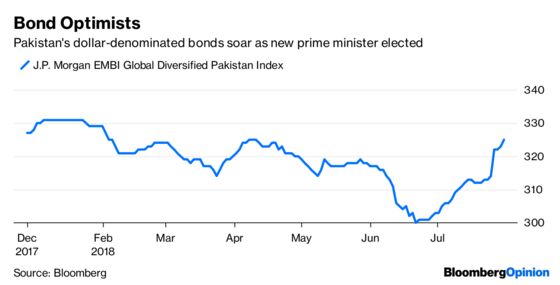

PAKISTAN BEARS WATCHING

At least one influential strategist thinks Pakistan could become an important battleground in the global trade wars. The incoming government of Imran Khan will most likely have to seek another bailout from the International Monetary Fund to stave off an economic crisis. The sum isn’t likely to be that large in the grand scheme of things, perhaps $10 billion to $15 billion, but the U.S. is already balking at delivering any new funds. That’s because the money would go toward repaying loans to the IMF, World Bank and — here's the kicker — China. Marc Chandler, the head of currency strategy at Brown Brothers Harriman & Co., wrote in a research note Wednesday that “U.S. policy makers recognize that China is using its loans to influence other countries” and that “these projects often put the U.S. businesses at a commercial disadvantage.” So if the U.S. can get Pakistan to stiff China on these loans, there could be a ripple effect through other Asian economies, with China feeling the pain. Chandler cited a recent study by RWR Advisory Group that found that almost a third of the value of the loans related to China’s Belt-Road initiative since 2013, or almost $420 billion, are in trouble because of persistent project delays, public opposition and national security issues.

TEA LEAVES

The Bank of England is widely expected to raise its key interest rate on Thursday for the second time since November. Already, some prominent firms are calling the likely increase a misstep. The median estimate of about 50 economists surveyed by Bloomberg is for the rate to be lifted to 0.75 percent from 0.5 percent. But according to the economists at Bank of America Merrill Lynch, doing so would raise the risk that the inflation rate continues to fall short of the BOE’s 2 percent goal while “cutting policy ammunition.” “A likely justification for a hike would be that policy is below ‘neutral,’” the economists wrote in a research note. “But we struggle to see how new BOE estimates of neutral could be of much practical use given their sensitivity to the unknowns of Brexit. With growth at a six-year low and core inflation below 2% and falling, we struggle to conclude that rates are inappropriately low at present.”

DON'T MISS

The Flat Yield Curve Is Flagging a Strong U.S. Economy: Tim Duy

Wall Street Turns Up the Pain on Earnings Misses: Stephen Gandel

Municipal Junk Soars as the Economy Roars: Matthew Winkler

Mark Carney Is In Far Too Much of a Hurry: Ferdinando Giugliano

India Snatches the Punch Bowl, Just in Time: Andy Mukherjee

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.