Glaxo Creates a Consumer Behemoth and a Pharma Question Mark

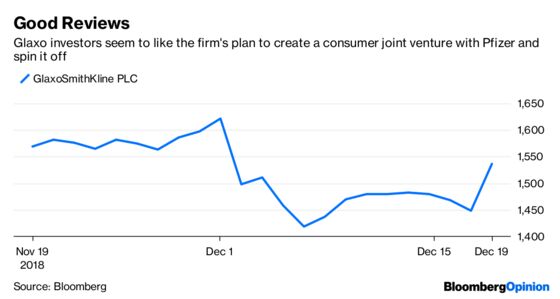

(Bloomberg Opinion) -- After years of trying to persuade investors that its pharma and consumer units were better together, GlaxoSmithKline PLC finally threw in the towel and committed to a split Wednesday.

The U.K. drug giant announced that it is creating a consumer joint venture with Pfizer Inc., and will separate the business from its pharma and vaccine unit within three years.

It’s a smart deal. Glaxo is taking advantage of Pfizer’s inability to find a conventional buyer for its consumer unit to gain synergy benefits and create an over-the-counter behemoth on the cheap. It also makes a clamored-for split easier. But big questions remain surrounding the pharma unit that will be left behind.

The deal will theoretically aid the pharma business, which Glaxo has been trying to reboot under the leadership of new R&D head Hal Barron after a fallow period. With the company facing looming generic competition for asthma drug Advair, one of its biggest products, the need for the next blockbuster is greater than ever.

Glaxo should reap extra cash flow out of this deal, which could help fund drug research, and the pharma unit should benefit from greater focus. The fact that it doesn’t require additional debt is also important, as it is already constrained by its dividend commitment and other recent deals.

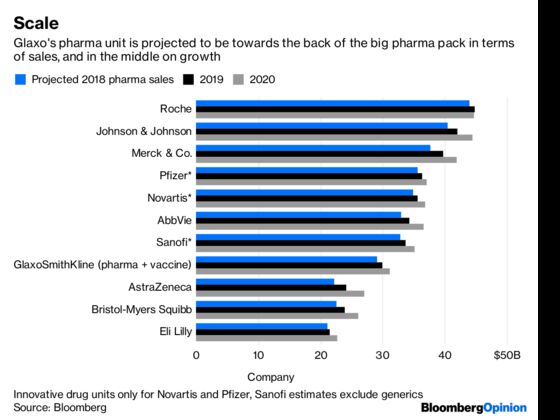

All this might not be worth as much, though, if the unit is in in bad shape when it goes solo. Three years sounds like a long time. But it’s not all that long when it comes to drug development and wholesale R&D revamps. The new consumer unit is set to be a global market leader. Glaxo’s pharma remainder will be at the small end for a big pharma, and has to overcome some pretty substantial challenges.

An Advair generic is due next year, which will add to pricing pressure in Glaxo’s respiratory business. It also heavily relies on its HIV drugs for growth, and though it has good treatments area, Gilead Sciences Inc. Merck & Co. are potentially serious competitive threats. Its shingles vaccine Shingrix is one of its few stars.

Glaxo’s drug pipeline leaves a lot to be desired. Its planned purchase, announced earlier this month, of cancer-drug developer Tesaro Inc. is a questionable start to a rebuild in that area. Tesaro’s lead medicine has been a commercial disappointment in a heavily crowded class, and its most advanced research project is even less original. Glaxo’s star internal cancer asset, a blood-cancer medicine, is one of as many as a dozen drugs aimed at the same target. It won’t hit the market until at least 2020.

Many of the rest of Glaxo’s research efforts are in very early stages, which makes them difficult to judge. And even with this split, Glaxo’s dividend and debt commitments will make substantially increased investment tough in the near term.

The impending separation will put extra pressure on the pharma unit’s results and R&D efforts. If things go poorly, the assumed valuation, balance sheet, and focus benefits of the deal may all take a hit.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2018 Bloomberg L.P.