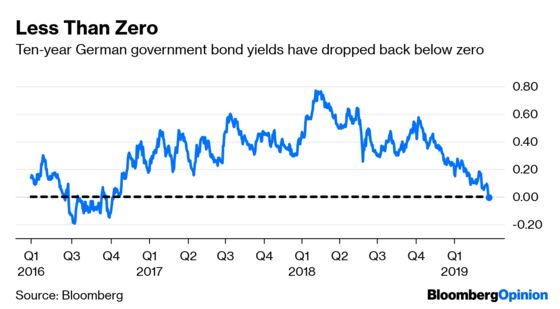

(Bloomberg Opinion) -- Betting that government bond yields will rise is the trade that keeps on giving — giving pain, that is. With the U.S. Treasury market signaling that the world’s biggest economy may be heading into a recession, investors are once again paying for the privilege of owning the benchmark German bond.

Remember in April 2015 when fixed-income guru Bill Gross said he’d spied “the short of a lifetime” by betting against German debt? Since then, the trend has been far from a hedge fund manager’s friend. While the 10-year bund spiked to 1 percent in about mid-2015, a year later it was back down to minus 0.2 percent. After spending most of the second half of 2016 below zero, the yield began an erratic climb to 0.8 percent — a rise that peaked about a year ago.

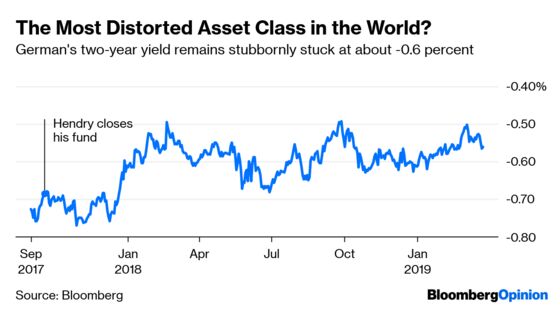

Speculating against “the most distorted asset class in the world” caused Hugh Hendry to close his Eclectica hedge fund in September 2017, after the German two-year note confounded his expectations. In the interim, that short-dated yield has averaged minus 0.6 percent — about where it was when Hendry decided to shut up shop, and within a whisker of where it rests today.

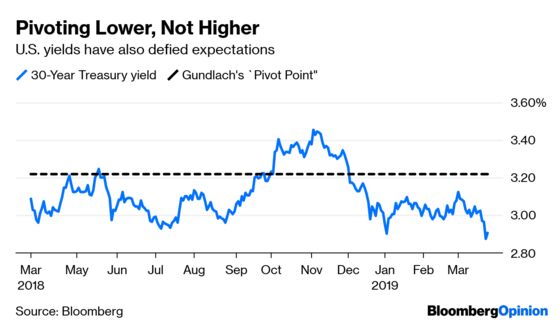

In the U.S. Treasury market, DoubleLine Capital Chief Investment Officer Jeffrey Gundlach warned a year ago that 3.22 percent on 30-year debt would prove to be the “one last pivot point” before yields started to march higher. Well, that level came, and went, and came again, and went again — and hasn’t been seen this year.

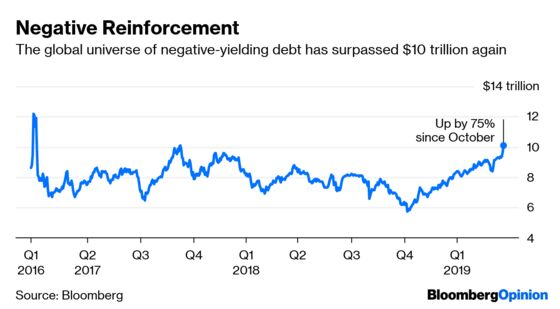

There’s another side effect of the renewed lurch lower in bond yields. The amount of debt around the world that yields less than zero has soared by 75 percent since October, reaching the $10 trillion level once again.

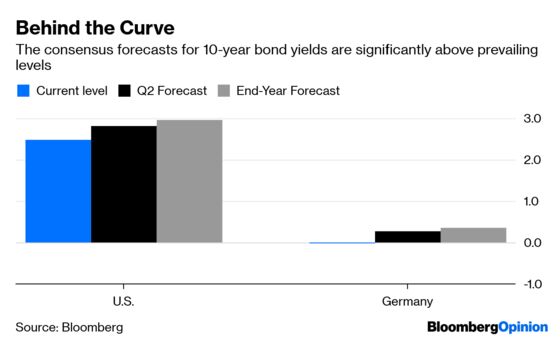

This wasn’t supposed to happen. With the Federal Reserve seemingly well on its way to normalizing interest rates and the European Central Bank halting additions to its stockpile of government debt at the end of last year, bond yields should have headed north. Indeed, the consensus forecast of analysts surveyed by Bloomberg News shows how far current levels are from mid- and end-year predictions.

Not every hedge fund will have been caught out betting on higher yields. But it will have been a tempting trade for global macro portfolio managers who’ve been struggling particularly hard to deliver decent returns in recent years. As the first quarter draws to a close, we’ll learn soon enough how many more victims the widowmaking trade of recent years has claimed.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.