GE Should Engage With Everyone on Asset Sales

The new GE CEO has a task to mitigate the bloated debt load and put the company on the path to a healthier future.

(Bloomberg Opinion) -- New General Electric Co. CEO Larry Culp could help himself out by accelerating asset sales.

Shares of the troubled industrial conglomerate climbed in late trading on Friday after Bloomberg News reported Apollo Global Management was considering a bid for the company’s GE Capital Aviation Services jet-leasing business. A deal, if one were to happen, would underscore Culp’s willingness to do whatever is necessary to mitigate GE’s bloated debt load and put the company on the path to a healthier future. Former CEO John Flannery had acknowledged the “optionality” offered by the GECAS business, considered the crown jewel of its remaining finance assets, but he didn’t include it in the breakup plan he unveiled in June and arguably dilly-dallied around an asset sale that could make a real difference for the company.

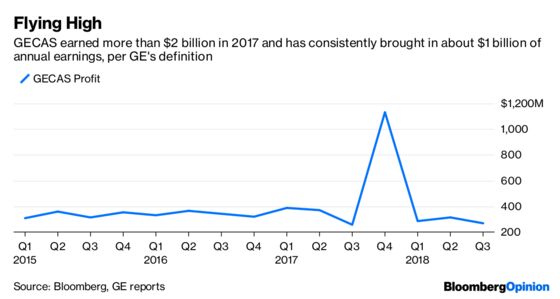

GECAS is being valued at $40 billion on an enterprise value-basis, according to the Bloomberg News report. Analysts including Barclays Plc's Julian Mitchell have estimated a $10 billion equity value for the unit in a sale. Interest at that price point would help alleviate doubts about GECAS’s valuation that arose after rival helicopter lessor Waypoint Leasing Holdings Ltd. filed for bankruptcy. GE has said its helicopter-leasing business, Milestone Aviation, is profitable and fleet utilization is about 90 percent, compared with about 78 percent at Waypoint.

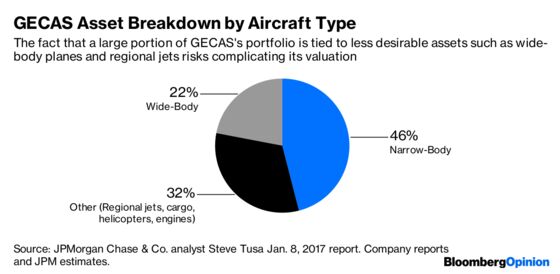

There are undeniable benefits to having an in-house lessor. As an engine manufacturer, GE has to have access to spares so it can replace engines under warranty. It’s able to house those at GECAS so when they’re not needed, they can be leased out to other users and earn money, rather than gather dust on the company’s balance sheet. Having a lessor also gives GE added insight into aviation market trends. But the ties that bind the two businesses aren’t so strong that they can’t succeed separately. And in the interest of raising funds and simplifying GE’s portfolio, this is a business that the company could afford to let go of. It’s certainly less of a hit to cash flow than its planned health-care spinoff.

Apollo’s interest follows reported talks in August between GE and Singapore’s sovereign-wealth fund GIC Pte. about a possible deal for GECAS. Other buyers are also circling. Also of note, KKR & Co. announced this week that it’s investing $1 billion to acquire a 50 percent stake in aircraft lessor Altavair AirFinance and six cargo aircraft in a bet that demand for commercial and freighter planes will remain strong.

If Culp were to capitalize on interest in the sector, it would echo his accelerated divestiture of GE’s stake in the merger of its energy assets with Baker Hughes. That’s another asset that Flannery had chosen to sit on, wary of creating the optics of a fire sale and selling out at a sub-optimal price. When GE announced the start of the Baker Hughes stake sale, I said it smacked of desperation and noted the poor timing with Baker Hughes trading at its lowest point since the combination with GE. Well, fast forward and Baker Hughes has slumped a further 7 percent as the price of oil has slid. Perfection can be the enemy of success, and there may never have been an ideal time to sell Baker Hughes.

Rapid-fire divestitures do smack of desperation. But you know what? GE is desperate, and a GECAS sale would show Larry Culp is trying to do something about it.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.