(Bloomberg Opinion) -- The truth hurts.

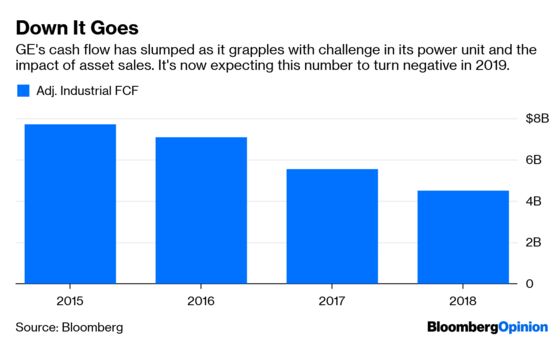

Free cash flow for General Electric Co.’s industrial businesses will be negative this year, down from a positive $4.5 billion in 2018, CEO Larry Culp said in a presentation on Tuesday at JPMorgan Chase & Co.’s Aviation, Transportation and Industrials Conference in New York. This was a danger I flagged a month ago, given the ongoing downturn in GE’s power unit and the associated restructuring obligations, loss of cash flow from divestitures and litany of one-time hits laid out by Culp on the company’s fourth-quarter earnings call. It was a reality that investors apparently needed to be hit over the head with before they acknowledged it, but they are starting to: GE shares fell more than 5 percent after Culp spoke.

It’s the first concrete disclosure we’ve gotten so far on 2019 guidance, and it’s a reminder of how the numbers will likely get yet worse for GE before they get better. GE had flagged the prospect of 2019 organic growth and operating margin expansion on the earnings call, but this remains a cash flow story and that's the number everyone cares about. The prospect of negative industrial cash flow in 2019 should raise alarm bells about Culp’s pledge for substantial growth in 2020 and 2021. Shifting from a negative number to a positive number might count as “substantial” in some people’s books, but the actual numbers do matter, and they point to 2020 industrial cash flow that’s at best in-line with the $4.5 billion pace set last year, assuming a recovery in the beleaguered power business. Culp said Tuesday that the cash burn at the power unit in 2019 will exceed the $2.7 billion outflow from last year.

It’s important to keep in mind that Culp’s call for negative free cash flow includes contributions from the health-care unit, which GE has tabled plans to divest after striking a deal to sell its biopharmaceutical business to Danaher Corp. for $21.4 billion. It doesn’t include the GE Capital operations, which are likely to be yet another drag on the company. Culp said Tuesday that the $4 billion the industrial parent is committing to GE Capital this year – already increased from $3 billion – likely won’t be the end of its funding obligations. Culp’s presentation comes about a week after the release of GE’s 10-K filing, which exposed potential land mines in its long-term care insurance business and possible pain points as the company unravels the intricate relationship between the industrial businesses and the GE Capital finance arm.

As a final note, GE’s approach to 2019 guidance and communication in general continues to befuddle me. Culp had room to set the bar low on the fourth-quarter earnings call and he chose not to take that opportunity, instead providing piecemeal disclosures on the lead-up to an outlook call scheduled for next week. Given that Culp spelled out most of the 2019 cash-flow headwinds on the earnings call, I find it hard to believe that he didn’t know then that it would be negative. He seemed nervous during Tuesday’s presentation, particularly when giving the free-cash-flow details, and JPMorgan analyst Steve Tusa had to ask for clarification about whether they included GE Capital. GE made great strides as far as transparency in the 10-K, but it’s still relying on heavily adjusted earnings metrics that muddy the picture.

I understand the reluctance to give bad news, but in holding back, GE has allowed investors’ expectations to get ahead of reality.

One of these was the adverse impact to cash flow from transitioning a supply-chain finance program that allowed GE to lock up early-pay discounts with suppliers to MUFG Union Bank, N.A. Culp mentioned again on Tuesday as being among the factors for the negative outlook in 2019.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.