Happy Birthday, GE. Investors Want Something to Celebrate.

(Bloomberg Opinion) -- Old age hasn’t been kind to General Electric Co. The company turns 127 years old this week, with April 15 marking the day that Charles Coffin agreed to merge his Thomson-Houston Electric Co. with Thomas Edison’s Edison General Electric Co. in a deal that created the foundation of the modern-day industrial giant.

There was much fanfare over GE’s age a few years ago as then-CEO Jeff Immelt promoted his efforts to reinvent the company as a software maker; both the New York Times and Bloomberg Businessweek labeled GE a “124-Year-Old Startup.” Oh, how times have changed. The digital business technically still exists: GE announced in December that it would form a separate (but still GE-owned) company to house its software assets, which generate about $1.2 billion in annual revenue. However you measure it, that’s a far cry from the $15 billion in sales Immelt said the digital unit could achieve by 2020. No one really asks GE about its software ambitions anymore, though. They’re too preoccupied by the company’s large debt load and cash-flow challenges, as well as the pesky problems at its GE Capital financial arm.

It’s impressive for any company to make it to 127 years old. Plenty of others have merged their way into oblivion, broken into too many pieces for anyone to remember what it was before, or simply flamed out. The question is whether we will someday soon be saying any of those things about GE, or if new CEO Larry Culp can get the company on stable enough ground that we can have a conversation about the next 127 years.

When GE’s difficulties were first mounting, a breakup was thought to be one possible balm, and that’s more or less what former CEO John Flannery proposed last year before he was unceremoniously ousted after just 14 months on the job. Under Flannery and Culp, GE has sold its transportation unit, unwound part of its stake in the merger of its energy assets with Baker Hughes and found a buyer for its biopharmaceutical business.

Both Culp and Chief Financial Officer Jamie Miller have suggested the remaining health-care assets aren’t core to the company and will eventually be divested somehow. But it’s become increasingly clear that some investors’ dream of a move to carve out a pure-play GE aerospace company – one that’s detached from a power unit that’s likely suffering from a structural downturn in demand and profitability and an undercapitalized financial arm that sucks cash away from the parent – will be impossible to realize in the near term. There’s the aforementioned debt load and the fact that the power unit’s cash flow problem will get worse before it can get better. GE’s recent results have also shed light on the working-capital advantages the industrial businesses got from GE Capital.

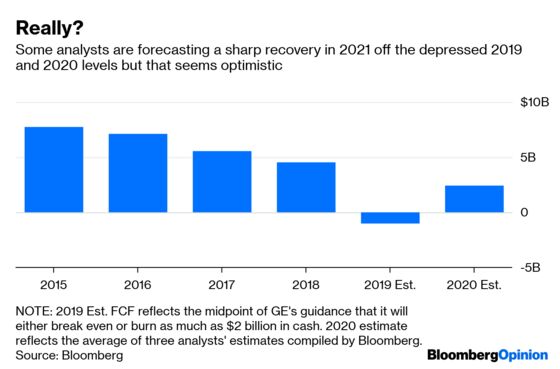

At this point, a GE recovery is more about making the slow and painful operational improvements that may eventually help the company reclaim, if not its former glory, at least an identity that's less of a punchline. There is no quick fix: just a poor cash flow outlook whose degree of ugliness depends on your tendency toward optimism. Even after JPMorgan Chase & Co. analyst Steve Tusa published a 123-page opus reminding investors of that last week, the stock is still holding on to most of its 2019 gains. Call it the Culp premium. But while some investors are willing to give Culp credit now for his promises of a substantial free cash flow in 2020 and 2021, it remains unclear how that rebound is going to happen.

Despite GE’s assertion that its businesses would be resilient in a recession, the company’s still-too-big debt load make it look vulnerable. Any associated drop in interest rates would balloon its pension liabilities, while weaker markets could expose the company’s assumptions for its legacy insurance operations as aggressive and set it up for a large GAAP charge.

Culp may yet save GE, but the turnaround may experience some false starts. As much as birthdays are a time for celebration, they are also an opportunity for self-reflection. So let’s celebrate this one with a resolution to learn from the mistakes of the past by setting realistic goals and holding the company accountable for them.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.