Are GE Insiders the Best Choice for Its Power Fix?

(Bloomberg Opinion) -- Larry Culp is General Electric Co.’s first outsider CEO, but he’s betting insiders will be the ones to save the company’s troubled power unit.

Culp laid out a plan last month to split GE’s power division into two as a means of accelerating cost cuts and operational improvements in a business that posted a $631 million third-quarter loss. GE’s gas turbines and services will be housed in one unit, while products that serve healthier parts of the power market, such as grid solutions, will be put in another. On Monday, GE announced that the CEO of GE Power, Russell Stokes, will now lead the latter business, while the head of GE’s power-services arm, Scott Strazik, will become CEO of the gas-turbine operations. Former GE Vice Chairman John Rice will return and become chairman of the gas-turbine unit.

All three men are long-term insiders. Stokes is a 20-year GE veteran, Strazik has been there 18 years, and Rice served a whopping 39 years before retiring last year as part of former CEO John Flannery’s efforts to overhaul the management team. All three will report to Culp.

One big criticism of Flannery’s tenure was that he was too surgical in his efforts to reboot GE’s identity, attempting to strike a balance between deference to the past and a need to address the harsh reality of the present. The appeal of Culp as GE’s next CEO, apart from his strong track record leading Danaher Corp., was that, in theory, he wouldn’t be as encumbered by allegiances to the GE of old. Two months into the job, though, he has yet to appoint a deputy of his own, and his actions indicate he intends to work within the GE system.

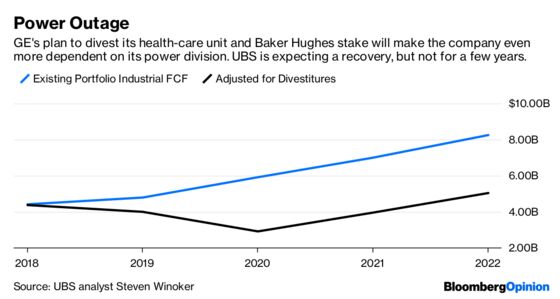

Installing a totally new leadership team likely wasn’t an option; GE doesn’t have time to educate uninitiated executives on the intricacies of the power market. GE was slow to adapt to the downturn in demand for gas turbines and its business remains far too bloated. That’s depressed GE’s cash flow to the point that investors are debating the company’s ability to handle its estimated $100 billion in net liabilities. GE is rushing to raise cash via asset sales, but it also needs to restore its earnings and cash-flow momentum as much as it can, and the power unit is key to that.

Rice previously led GE Energy, which included the gas-turbine businesses, so this job does cater to his expertise. GE highlighted his relationships with customers. That will be useful as GE seeks to assure utilities that the quality of its products and services won’t be impaired by its plan to cull at least $1 billion in costs from the power business alone this year. An oxidation issue with its flagship H-frame gas turbines caused Exelon Corp. to temporarily shut down two power plants. A fix has been rolled out, but the incident underscored how little room GE has for mistakes in its power business right now.

That being said, given the extent to which mismanagement of GE’s power business exacerbated the demand downturn, it’s jarring that Culp didn’t recruit another outsider to share oversight of the turnaround. Rice hasn’t run GE’s power business for years, but he served as a vice chairman of the company from 2005 until his retirement last year. Much like Flannery, his professional identity is intertwined with the legacies of the Jeff Immelt era at GE, legacies that most investors are ready to put behind them. And fixing GE’s power business is about more than soothing worried customers. For this turnaround to stick, the company needs to deal with the deep-rooted cultural issues that allowed the kind of bad news that’s at the heart of GE’s current crisis to fester for years.

Stokes, meanwhile, has been criticized for failing to move more aggressively to fix the power unit, and many investors believed he would be fired, if for no other reason than to send a message. His new job will take him away from GE’s most pressing problems in the power unit and will likely be more about carving up GE’s OK-ish power assets for divestitures.

To me, Culp’s decision to tap a trio of insiders to run the power business speaks to how he himself is perhaps too much of an outsider. He has little experience with gas turbines, nor the kind of debt squeeze that GE is battling. That lets him get away with the kind of management decisions investors would never stand for if they were coming from Flannery. It appears that if Culp wants to tear up the GE playbook, he may need help from the people that wrote it in the first place.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2018 Bloomberg L.P.