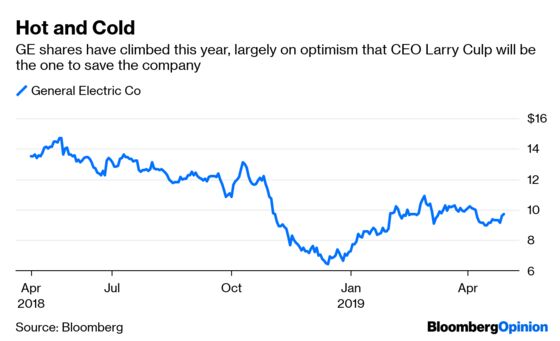

(Bloomberg Opinion) -- At first blush, General Electric Co.’s first-quarter results would seem to suggest that its turnaround is gaining traction and that the industrial giant is finally getting a handle on cash flow. Look deeper, though, and you’ll know not to get too carried away.

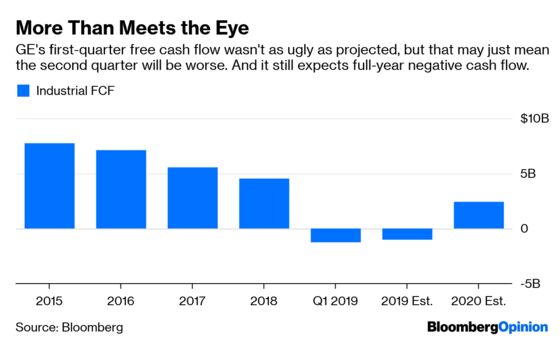

GE said it burned $1.2 billion in cash in the first three months of the year, far less than the roughly $4 billion that analysts from Wolfe Research and RBC were projecting. Cash is the only number that really matters for the struggling industrial company, given ongoing concerns about its high debt burden and a comical degree of adjustments that make its earnings per share relatively useless. So in that respect this is a win for GE. But while the first quarter is seasonally the worst for the company, it never made much sense to me why the cash flow drags that CEO Larry Culp has flagged for this year — including restructuring costs and the untangling of its GE Capital financing operations — would hit early on.

Just two weeks before the first quarter ended, Culp told investors that first-quarter that the cash flow burn would be worse than the negative $1.7 billion it reported in the same period a year earlier. The surprise improvement is largely a function of the timing of orders, the collection of customer payments, planned restructuring and other non-operational items, GE said Tuesday. Gordon Haskett analyst John Inch also flagged beneficial adjustments for the Baker Hughes oil and gas business that GE has already started to sell. All of this will balance out over the course of the year — which helps explain why GE maintained its guidance for as much as a $2 billion cash burn in 2019. Power seemed to get most of that timing benefit, with the unit posting a small operating profit after two quarters of steep losses. But it’s a bit hard to judge what’s actually going on here because a breakdown of free cash flow by segment was notably absent from GE’s earnings materials.

The company had disclosed 2018 cash flow for each of its segments when it delivered its guidance for this year and it’s disappointing to see it taking a step backward on the transparency front. That was one of the few positive takeaways from an outlook that retained GE’s heavily adjusted earnings construct as a benchmark.

The expectation was that GE would continue to keep investors apprised of those segment-by-segment cash-flow numbers and hold itself accountable to them. The company already has a fair amount of discretion on how it allocates corporate overhead, investments, tax benefits and inter-company transactions between its divisions, and the lack of disclosure isn’t going to convince skeptical investors of GE’s math. GE did say on the outlook call that it believes its cash-flow figures are more meaningful on an annual basis because there’s significant variability between quarters. That’s all the more reason not to take too much heart from the first-quarter results.

One generous way to view the positive cash-flow surprise is to believe Culp set the bar so low for 2019 that all the company has to do is roll over it. It would be a welcome development for GE to be guiding conservatively for once. But I’m not so sure that’s the case here. Time and again, we’ve seen situations where numbers from GE are taken at face value when they should be more closely scrutinized, or are considered a victory just because they surpassed a so-called whisper number from analysts that never made much sense in the first place.

The bigger issue, of course, isn’t what cash flow GE generates in the first quarter or even the full year of 2019; it’s what the trajectory is from there. GE reiterated its expectation for cash flow to turn positive in 2020 and accelerate from there in 2021. And while that will likely happen in some capacity, those sweeping terms cover a lot of ground. I remain skeptical that GE’s annual cash flow will surpass the depressed $4.5 billion level of 2018 over that time frame.

As Culp himself said in Tuesday’s release, “This is one quarter in what will be a multi-year transformation.” Investors would be wise to remember that.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.