(Bloomberg Opinion) -- When London’s Gatwick airport was shut down just last week, stranding thousands of passengers hoping to fly somewhere for Christmas, police suspected someone was deliberately flying a drone nearby. But they failed to identify a culprit. Perhaps the projectiles several eyewitnesses claimed to have spotted weren’t drones at all, but popping champagne corks?

On Thursday, the consortium that owns Britain’s second busiest airport announced the sale of a 50 percent stake to Vinci SA, the French construction and infrastructure group. Including net debt, the transaction values Gatwick at about 8.5 billion pounds ($10.7 billion), or about 20 times Ebitda. Though a princely sum, it’s actually a bit less than the 28 times multiple Gatwick’s principal owner Global Infrastructure Partners secured for the much smaller London City airport in 2016 – a price Willie Walsh, chief executive of British Airways parent IAG, described as “foolish.”

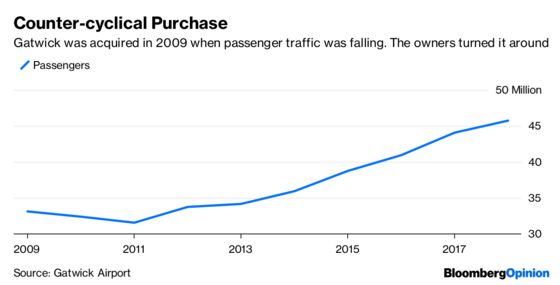

Even so, Gatwick has turned out to be a huge money spinner for its owners. They wisely snapped up the airport for just 1.5 billion pounds in 2009, when Britain was mired in recession and regulators forced BAA to break up its monopoly in southeast England. Locking in profits now and taking some risk off the table feels sensible with Brexit fast approaching and one of Gatwick’s top customers, Norwegian Air Shuttle ASA, suffering financial strain.

I’ve written before about how a shortage of landing slots and favorable regulation has turned the U.K.’s privatized airports into a cash cow for their owners. Gatwick isn’t as profitable as Heathrow because it can’t charge equally high landing fees. (It has more short-haul and budget airline traffic.) Milking its retail concessions and car parking fees helps make up for that, though.

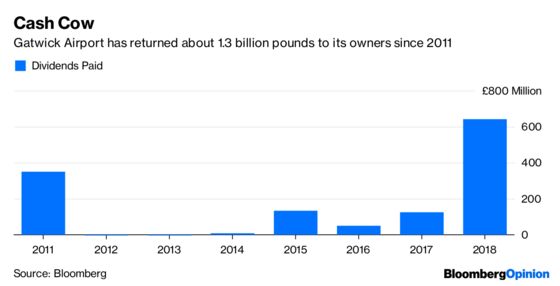

Operating margins exceed 30 percent and Gatwick has paid little corporation tax in recent years. Hence its owners felt able to pay themselves a whopping 643 million pound dividend earlier this year, bringing the total payouts since 2011 to about 1.3 billion pounds, according to Bloomberg data.

In fairness, the consortium of owners, which also includes funds from Abu Dhabi, South Korea, Australia and California, has done a decent job of refurbishing and expanding the airport facilities and driving passenger growth. Gatwick’s single 3.3 kilometer runway is the most efficient in the world in terms of flights per day. And at least Gatwick isn’t drowning in quite so much debt as its larger rival Heathrow. Although net debt that’s 6.5 times Ebitda can hardly be described as cautious.

Gatwick’s future growth is limited because it lost out to Heathrow in a competition to build another runway in southeast England. Even so, its fortunes are probably set fair.

It’ll be almost a decade before Heathrow’s third runway opens, and that’s probably an optimistic assessment given the typical delays that accompany large infrastructure projects. Plus there are other things Vinci can do to expand passenger growth, including making more use of Gatwick’s standby runway and encouraging customers to use larger planes.

While Brexit-related regulatory or economic troubles could yet make the French group’s largess look silly or ill-timed, the threat of near-term disruption doubtless helped it avoid an even higher price. And, in the long term, Britons aren’t about to stop going on vacation, nor does the cheap pound reduce London’s attraction as a tourist destination. In other words, there’s something for both sides to toast here. Just watch out for those celebratory corks.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2018 Bloomberg L.P.