GAM’s Rogue Manager Won’t Go Gentle Into the Night

(Bloomberg Opinion) -- It’s eighteen months since Swiss fund manager GAM Holding AG was first alerted to the possibility that Tim Haywood, the manager of its flagship absolute return bond funds, might be in breach of his fiduciary duties. With the scandal still ongoing, it’s little wonder that GAM has yet to appoint a new chief executive officer – or find a buyer for itself.

GAM’s board failed to win the backing of at least 50 percent of shareholders at the AGM to release its directors and executives from liability. It’s rare for Swiss companies to lose what’s typically a routine motion, though not unprecedented; UBS AG suffered a similar rejection last week, while GAM itself saw its executive bonuses plans rejected two years ago.

The vote’s outcome, plus the prospect of Haywood fighting to clear his name, mean the company’s travails are far from over.

The meeting result leaves GAM’s management open to possible legal action for its handling of its former star manager. Given the steep decline in the value of their investment, shareholders are right to express their disapproval through their vote, and would be justified in seeking legal redress for their losses. Moreover, at some point you’d expect the regulators in the various jurisdictions in which the company operates in to chime in with their views on how it has managed its crisis. Their collective verdict might not be exactly favorable.

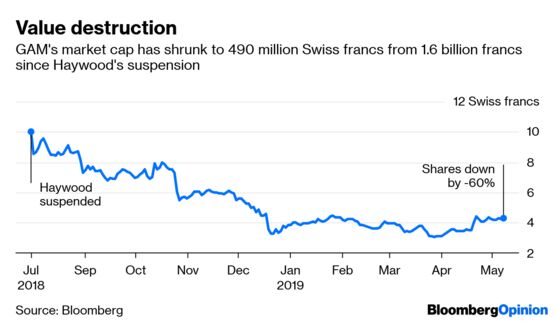

A quick recap of the GAM timeline of events might be handy. In November 2017, an internal whistle-blower expressed worries to GAM’s management about Haywood’s conduct. In March 2018, the informant “expanded on the initial concerns” and contacted the Financial Conduct Authority, the U.K. financial services regulator. It took GAM until the end of July 2018 to suspend Haywood and halt redemptions from his funds, and another couple of weeks before it announced it was liquidating those investments.

In November, CEO Alex Friedman stepped down, with board member David Jacob taking over pending a permanent replacement. And In February of this year, GAM dismissed Haywood for “gross misconduct.”

At the time it suspended its star fund manager, GAM had about 84 billion Swiss francs of assets in its investment management division, including a bit more than 7 billion francs in the funds overseen by Haywood. By the end of March, that total had shrunk to about 55 billion francs as customers spooked by the turmoil pulled money from the firm.

Haywood tried to attend Wednesday’s meeting, but wasn’t allowed in. GAM said the shares he’d bought to gain access weren’t registered; Haywood told reporters his stock had been deregistered. A conspiracy theorist might well raise an eyebrow at that blocking maneuver.

For his part, Haywood has said the firm has made him a “scapegoat,” and that he plans to appeal his dismissal, which GAM has acknowledged is within his rights. There could be rather a lot of dirty laundry waiting to be aired about who knew what about the illiquid investments Haywood made to juice his returns, and some mudslinging about his alleged abuse of the company’s policies about accepting gifts and entertainment.

"I continue to believe that I have been treated unfairly and this is a forum in which I could make my voice heard," Haywood told my Bloomberg News colleague Patrick Winters in an interview after being barred from Wednesday’s meeting. Haywood’s actions today suggest he’s not willing, in Dylan Thomas’s phrase, to go gentle into that good night. Any legal action against GAM from disgruntled investors will be dramatic enough; adding Haywood’s complaints into the mix promises to make the firm’s drama even bloodier.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.