(Bloomberg Opinion) -- The search continues for a permanent chief executive officer to run GAM Holding AG, interim leader David Jacob said on Thursday. If the board doesn’t get a wiggle on, there won’t be much of the Swiss fund manager left to run for whoever is brave, foolish or desperate enough to take the job.

To summarize: In July, GAM suspended Tim Haywood, the head of its flagship absolute return bond funds, more than six months after an internal whistle-blower raised concerns about his conduct. Rattled clients started to pull money out of the firm. In November, it ditched CEO Alex Friedman, with board member Jacob stepping in as a placeholder. The outflows continued.

Investors pulled a net 10.5 billion francs ($10.5 billion) out of GAM’s funds last year, almost matching the 11 billion francs unwound from the business Haywood oversaw. Add in 6.8 billion francs of market losses and currency movements, and the assets overseen by the firm shrank by a third in the second half of the year. As Jacob said on a conference call, Thursday’s earnings report “does not make for easy reading.”

The collapse in earnings was flagged in December. What’s more worrying is the deterioration in GAM’s underlying business, which is reflected in the 80 percent slump in its share price in the past year.

The amount of money eligible for performance fees has slumped to 6.7 billion francs from 17.3 billion francs at the end of last year. That slide, combined with a paucity of returns, saw GAM’s income from performance fees collapse to 4.5 million francs from more than 44 million francs a year earlier.

So even if the firm’s portfolio managers are able to generate market-beating returns this year, “it’s clear that our potential to generate performance fees has much reduced,” the company said.

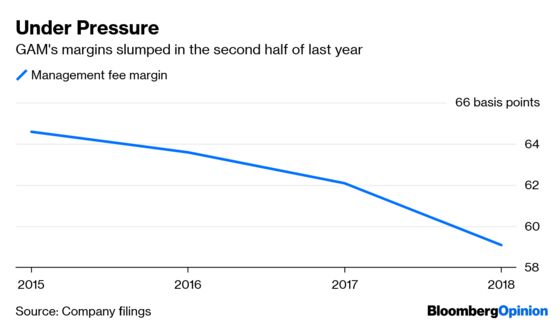

Moreover, the annual decline in average management fees shown in the chart above masks an even nastier figure. While margins held up in the first half at 61.2 basis points and were little changed from 2017, by the end of the year they had collapsed to 55.6 basis points. Worst hit among the products GAM offers were its systematic strategies, with margins on its quant funds collapsing to 74 basis points from 100 basis points. Those fees aren’t coming back.

In one apparent bright spot, GAM employees don’t seem to be fleeing, with total headcount about unchanged at 925 full-time staff at the year-end. Of course, that may say as much about the lack of hiring across the entire fund management industry as it does about loyalty to the cause. And GAM’s straitened circumstances mean it plans to cut about 10 percent of the workforce to trim costs, so some may be hanging on for redundancy payouts.

The future guidance, however, remains bleak, with the firm repeating that underlying profit this year will be “materially below” what it earned in 2018. More big clients may still decide to withdraw their funds.

GAM said on Thursday it has dismissed Haywood for gross misconduct. If he appeals, which Jacob says he has the right to do, the saga will drag on for even longer, undermining GAM’s efforts to draw a line under the debacle – and making the top job even less attractive to potential candidates.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.