Fund Managers on a Roll as M&A Hopes Spring Eternal

(Bloomberg Opinion) -- After trashing the share prices of European asset managers in 2018, stock market investors are showing the industry a lot more love this year. What’s puzzling about the scale of the rebound is that it comes as clients are still proving reluctant to entrust their savings to fund managers.

Even as global equities recover from the pounding they took in the fourth quarter, there’s a distinct lack of enthusiasm from savers and investors to pump money back into investment products, a reluctance that’s reflected in the first-quarter data reported so far by the industry.

Amundi SA, Europe’s biggest asset manager, saw clients pull 6.9 billion euros ($7.7 billion) from its funds in the first three months of the year. Man Group Plc, the world’s biggest publicly traded hedge fund, suffered $700 million of net outflows, while Jupiter Fund Management Plc endured a fifth consecutive quarter of withdrawals as an additional 482 million pounds ($627 million) headed for the exit.

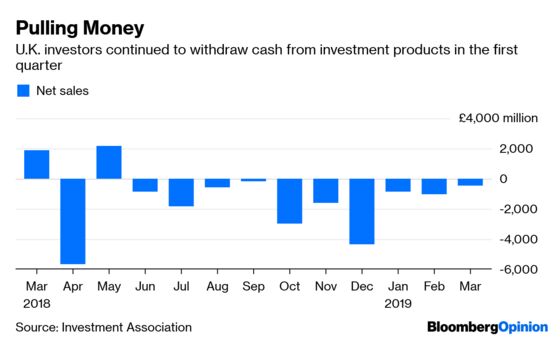

Figures compiled by the Investment Association show that in the U.K., for example, investors have pulled money out of funds for 10 consecutive months. Both retail and institutional clients withdrew money in the first three months of this year even as stock markets gained, according to the trade body’s most recent data.

Moreover, the industry worries that contributed to last year’s collapsing share prices haven’t gone away. A report published this week by the Boston Consulting Group suggests that profits will fall almost a third by 2023 in a worst-case scenario for the global investment management industry. The study of 30 firms around the world with $39 trillion of assets suggested that net new flows were worth 0.9 percent of assets in 2018, compared with a historical average of 1.5 percent, while revenue growth slowed to just 3 percent last year, a third of the pace seen in 2017.

Analyst at UBS AG, led by Michael Werner, are dubbing this year’s European share–price rally “the flowless recovery,” noting in a research report last week that the industry’s forward price–earnings ratio has improved to about 13.7 times, from a bit more than 10 times at the end of last year. For that improvement to be justified, though, the UBS analysts calculate that net retail inflows would need to accelerate to about 6 percent of assets under management – which is double what the bank estimates is the best that can be expected in the second half of this year.

As a result, UBS reckons asset managers are no longer oversold, and has responded by changing its recommendation on Jupiter to sell from neutral, and by downgrading Schroders Plc to neutral from buy. It remains a wonder to me how many analysts shied away from slapping sell recommendations on asset managers’ shares through the bloodbath of last year.

So if investment flows aren’t the inspiration behind the rebound in their stocks, what’s helping European asset managers defy gravity? Their market values seem to be getting tickled higher by the tailwind of takeover talk, even though the theme of industry consolidation has been floated for a couple of years without really translating into transformative deals.

But the recent flurry of articles contemplating the likely future of Germany’s DWS Group GmbH, majority owned by Deutsche Bank AG, as well as the prospect of Swiss firm GAM Holding AG seeking a buyer as a solution to its woes, has reawakened speculation about mergers and acquisitions. Moreover, the chatter seems to be emanating from inside the camps of the potential buyers and sellers themselves, so it’s not just M&A bankers fantasizing about fee-generating deals.

Still, a couple of words of caution are called for. Firstly, the so-called squeezed middle of fund management has thus far shown little ardor for M&A, despite the plethora of consultancy reports arguing that bulking up is the key to survival.

Secondly, if we return to the first chart in this article, note that Standard Life Aberdeen Plc, which was created by the merger of two medium-sized firms, has underperformed its less M&A-amenable peers. After losing half of their value last year, its shares have recovered by less than 10 percent in 2019. Merging two different cultures, it seems, is tricky to pull off.

So takeover talk might remain just that – talk, rather than action. Chasing the shares of fund managers higher in the hope that the urge to merge will finally unleash a series of auctions could turn out to be cruising for a bruising.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.