(Bloomberg Opinion) -- What exactly is sterling up to? There was a theory that the recent mini-rally in the pound was all down to the receding prospects of a “no-deal” Brexit as moderate lawmakers tried to seize control of the process from Prime Minister Theresa May.

On Tuesday night that idea was tested to destruction. A parliamentary proposal from MPs Nick Boles and Yvette Cooper to delay Brexit rather than leave without a deal was comfortably beaten. Meanwhile, May and her fractious euroskeptic lawmakers made peace around another proposal that will see her return to Brussels to try to rework the U.K./EU withdrawal agreement. If anything, the chances of a “no-deal” exit have increased and those for the softest options such as a second referendum diminished.

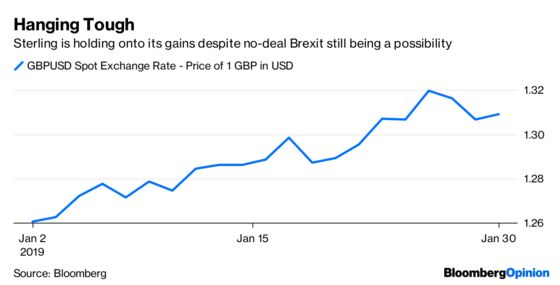

Despite all of this, sterling held onto most of its recent gains. What this tells us is that the restored unity of May’s ruling Conservative party (even if temporary) is being given at least equal weight among traders to the avoidance of a no-deal Brexit — or a messy extension to the process. This somewhat counterintuitive market behavior can almost certainly be ascribed to one man: Jeremy Corbyn.

While a no-deal Brexit is a clear worry given the potential for economic carnage, the prospects of a hard-left Labour government under Corbyn is arguably even more troubling for financial markets. A Brexit-created split in the Conservatives between the hard Brexiteers and moderate remainers would only make that more likely. As such, May finding common cause with Boris Johnson, Jacob-Rees Mogg and Northern Ireland’s DUP is at least a sign of some stability within the governing party and its backers.

How long this lasts is a fair question, given the intransigence of the Brexiteers and the EU’s stout refusal to give them what they want: a scrapping of the so-called backstop that guarantees no hard border with Ireland. But May at least has a clear-enough majority from her lawmakers to justify another go at negotiating with Brussels.

While there was a mess of different possibilities ahead of Tuesday night, this is starting to look like a more binary situation (which is what May wants). Either we get some reworked version of her deal, with probable concessions on a backstop, or a hard exit on March 29. The soft Brexit crowd haven’t given up, but Tuesday night didn’t go well for them.

Now one could question — and I certainly would — whether sterling bulls are correctly pricing the risk of no deal. But given that May herself doesn’t want to crash out without an agreement, you can see the logic. A reworked agreement, even with a modest delay to Article 50 to secure passage of the required legislation, is also the most likely path to an early interest-rate hike from the Bank of England.

The only certainty is that we’re less than two months away from Brexit today and if nothing is agreed by the U.K. Parliament and the EU, then it’s the hardest of exits. Valuing sterling on the outcome of a coin toss still leaves it vulnerable.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.