(Bloomberg Opinion) -- General Electric Co.’s annual filing marked a step forward in the company’s efforts to be more transparent, but the added disclosures on its insurance operations also underscore the ongoing risks in that legacy business.

There was no outright bad news in the 10-K report released late Tuesday and GE went to much greater lengths than in the past to explain the state of its insurance liabilities and the relationship between its financial and industrial arms. That counts as a victory for the company as it tries to claw its way back from a crisis of cash flow and credibility. Notably, GE still expects to contribute a total of $14.5 billion to shore up its long-term care insurance reserves, in line with the funding gap it disclosed in January 2018. I had been concerned that number may grow as GE completed its statutory-reserve stress test; the fact that it didn’t is probably what drove the stock higher on Wednesday. “We are putting GE on firmer financial footing,” CEO Larry Culp said in a letter to shareholders that was also released late Tuesday, one day after the company announced the sale of its biopharmaceutical business to Danaher Corp. for $21.4 billion.

The proceeds from that deal are earmarked for debt reduction, which means GE will needs to come up with the cash for the remaining insurance contributions elsewhere. And while GE seems to have avoided fresh disaster for now, it’s worth digging deeper on the numbers and asking whether the reprieve is only temporary. Recall that GE took a relatively nominal $65 million after-tax charge related to its long-term care insurance operations in the fourth quarter. One reason the charge was so small is because GE recorded a $1.9 billion benefit to its reserve margin related to its assumptions around the interest rate calculations used to estimate its future policy benefit reserves, known as the discount rate. That more than offset a $1.2 billion hit from a more pessimistic outlook on morbidity improvement – i.e., the extent to which claimants who are functionally limited will get better and stop needing the insurance benefits. Without the change in rate assumptions, GE likely would have faced a much more material charge, which would have cast a harsher pall on the lack of 2019 guidance.

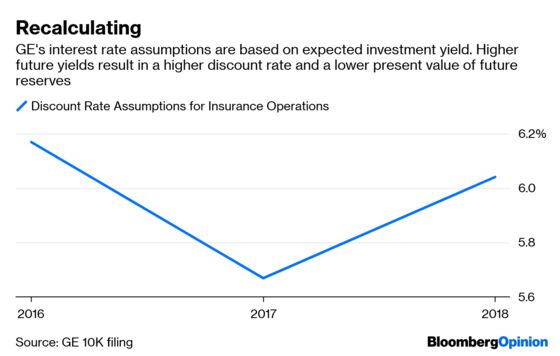

We’re now learning more about what drove that outlook for higher investment yields. GE hired a new chief investment officer for its insurance operations and decided it could get more bang for its buck by pushing into higher-yielding assets such as private equity, senior secured loans and infrastructure debt, among others. So GE assumed a higher weighted-average discount rate of 6.04 percent for the 2018 test of insurance reserves, compared with 5.67 percent in 2017. (Recall that a reduction in discount-rate assumptions contributed to a $9.5 billion pre-tax charge to 2017 earnings). I don’t have a crystal ball on markets and who knows, maybe GE has some choice bets up its sleeve and this plan will work out splendidly. But in the spirit of increased transparency, let’s call this for what it is: taking on more risk and potentially only kicking the can down the road on bigger insurance charges.

Prudential Financial Inc., one of the biggest sellers of long-term care insurance before it halted new issuance in 2012, also released its annual report this month and it assumes a weighted-average investment rate for its legacy long-term care operations of 5.39 percent. There are puts and takes between the two companies’ books of business, but the point is that GE’s outlook doesn’t look particularly conservative. That’s all the more so because new accounting rules set to take effect in 2021 will standardize assumptions and require a discount rate equivalent to an upper-medium-grade fixed-income instrument yield. Honeywell International Inc. and Emerson Electric Co. both have single-A credit ratings and yields on their longer-term bonds are in the 4 percent range.

The difference between these numbers seems small, but a 25 basis-point reduction in the discount rate would result in a $1 billion pre-tax increase to future policy benefit reserves, GE said in the filing. So knocking the discount rate down to 4 percent would require $8 billion in additional reserves. It’s also worth noting that Prudential last year said it would no longer assume a morbidity improvement for its long-term care insurance business because it wasn’t seeing covered people get healthier. Despite its lowered outlook, GE is still assuming a 1.25 percent morbidity improvement per year over 12 to 20 years. Taking that down to zero would require a $3.7 billion increase to reserves.

We will learn more about the thinking behind GE's assumptions next week when the company hosts a "teach-in" on its insurance operations. I can't tell you that GE's assumptions are wrong; the markets may go the company's way. But given everything the company has been through, it would seem to wise to assume the worst and then be able to surprise investors with positive, rather than negative, developments. And that isn't what GE is doing here.

Prudential was a primary provider of long-term care insurance, while GE sold reinsurance. GE's reserves per individual life covered are on the high end, but its average holder is older, which means there's less time to collect premiums, and a bigger share of its policies offer lifetime benefits or inflation protections, which makes them more costly.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.