Five Essential Numbers For Measuring An Economy

(Bloomberg Opinion) -- When you hear about economic growth, or the size of the economy, it’s referring to gross domestic product. Invented in the 1930s, GDP measures the market value of everything produced in a country (or region, or state) in a given year. When you hear about the labor market, it usually involves the unemployment rate, which is the percent of people who want to work who don’t have jobs.

In recent years, more people have begun to question the use of these commonly reported economic statistics. One problem with GDP is that it doesn’t take inequality into account — if all the gains from growth flow to the rich, GDP will go up while the average person won’t be any better off. Another problem people complain about is that GDP doesn’t measure human happiness — if people get sick and are forced to buy more medicine, GDP can go up while the standard of living goes down. Meanwhile, the unemployment rate doesn’t take discouraged workers into account — people who exit the labor force entirely because no one will hire them.

These flaws are real. But instead of thinking that the official economic numbers are fake news, and that there are some much better numbers out there, it’s important to realize that there is no perfect measure of an economy’s health. Different numbers are better for different purposes.

If you’re trying to measure a country’s overall economic power, total GDP is probably as good a measure as any. It represents the size of the tax base that governments can draw on to pay for their militaries and provide social services. GDP also gives a good rough measure of a country’s ability to move world markets, though it’s also important to look at how much a country actually imports and exports.

When looking at the living standards of developing countries, per capita GDP — adjusted for purchasing power parity, to take into account price variations of goods in different countries — is a good measure. Per capita GDP is easy for most countries to collect with a reasonable amount of accuracy, and for outsiders to estimate from proxy measures. It correlates with lots of important measures of well-being, such as hunger and infant mortality, that affect broad swathes of the population. There’s a very tight relationship between PPP GDP per capita and the Human Development Index, an index invented specifically to measure tangible living standards.

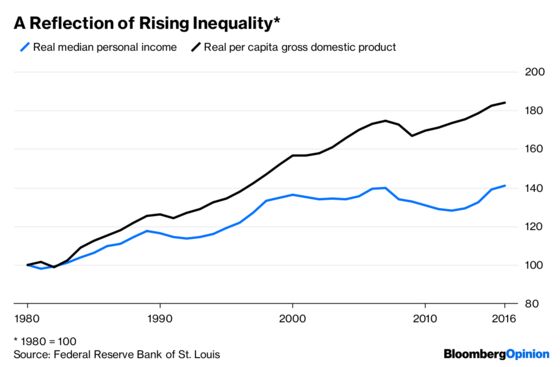

But when measuring the decade-to-decade performance of a rich country like the U.S., GDP growth isn’t the best measure, for the reasons described above. A better alternative is real median personal income. This looks at the median, so it isn’t changed very much by large gains for the rich. Unlike household income, it isn’t distorted by changes in the number of people who live together. And it looks at all sources of income, including government transfers, benefits and investment income.

Since the 1980s, real median personal income has gone up, but more slowly than real GDP per capita:

The gap between the two is a good, quick way of illustrating the growing inequality between the rich and the middle class.

But if you need information quickly — if you’re in a recession or crisis, or if you’re trying to do a rapid evaluation of a new economic policy — you’re stuck with GDP. Real median personal income is only available with a lag — for example, the most recent numbers are from 2016.

This measure also doesn’t give much information about the standards of the poorest members of society. For that, you can look at the average income of the bottom 80 percent or 90 percent, as measured by economists Thomas Piketty, Emmanuel Saez and Gabriel Zucman. You can also look at the Supplemental Poverty Measure, a number created by the Census Bureau and the Bureau of Labor statistics that tries to take into account the cost of the things poor people need and the government assistance they receive. Though this benchmark is generally higher than the official poverty measure, it also shows some good news — child poverty has fallen substantially in recent years, thanks to government programs.

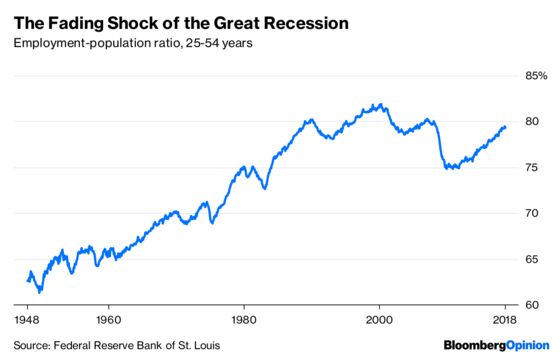

When looking at labor markets, the most important number is probably the prime-age employment-to-population ratio. By looking at who has a job rather than who doesn’t, this yardstick ignores the unhelpful distinction between unemployed people and discouraged workers. By only looking at people between the ages of 25 and 54, it ignores most of those who are either still in school or in early retirement. This measure currently shows a labor market that has mostly recovered from the Great Recession:

Over the longer term, changes in the ratio don’t just reflect the health of the labor market — they also include long-term changes like women’s entry into the formal workforce.

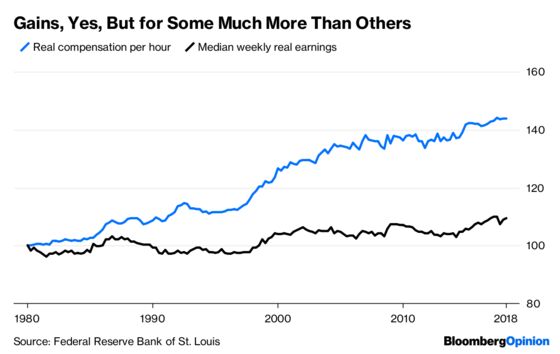

As for wages, there are two measures I like — real hourly compensation, and median real weekly earnings for full-time employees:

Both have grown, but the former has grown much faster, especially before the Great Recession — this shows rising wage inequality, since the figure is an average that gets pushed up by big wage gains for high earners. Meanwhile, increases for both have slowed in the current recovery.

So if you only look at GDP and the unemployment rate, you’re missing out on a lot of information. If you can, remember to also look at real median personal income, the Supplemental Poverty Measure, the age 25-54 employment-to-population ratio, real hourly compensation and median real weekly earnings. Even all together those measures won’t tell you everything about the health of the economy, but they capture much of the important stuff about growth and labor markets.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.