Financial Darwinism Works its Magic on Research Analysts

(Bloomberg Opinion) -- The MiFid II regulation introduced by the European Union at the start of last year changed the way research on companies gets paid for, prompting warnings that the amount and quality of analysis of small firms would suffer. Instead, the sell side seems to have risen to the challenge by widening its net.

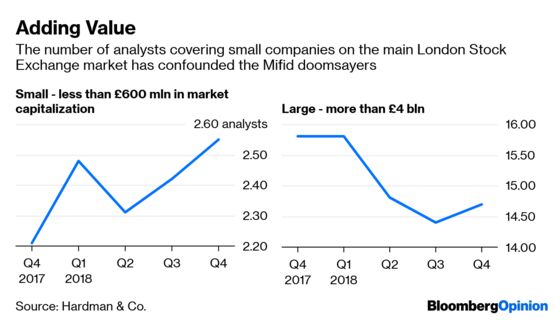

The Markets in Financial Instruments Directive, which obliges investment managers to separate what they pay for research provided by the sell-side community from what they spend on trading fees, stoked concern that large companies would monopolize analysts’ attention.

But figures compiled by consultancy firm Hardman & Co. suggest that researchers have responded to the existential threat posed by the rules by shifting more attention to less-scrutinized players.

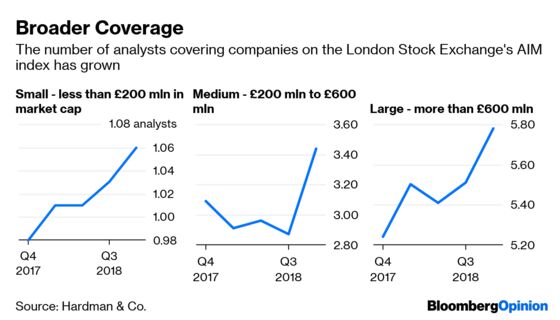

Coverage of firms listed on the London Stock Exchange’s AIM index, launched in 1995 as the Alternative Investment Market to allow smaller companies to float shares without meeting the more onerous rules of the broader market, has also widened, Hardman’s research shows.

The Hardman study backs up comments made by the Financial Conduct Authority earlier this week. The regulator said that the change in funding research has not had “the dramatically negative impact that some predicted” on coverage of smaller companies.

The FCA reckons the new rules saved investors in U.K.-managed equity portfolios 180 million pounds ($239.7 million) last year, as dealing commissions dropped and buy-side spending on research declined by as much as 30 percent. The regulator estimates those savings for fund buyers will rise to as much as 1 billion pounds in the coming five years. That’s not to be sniffed at, given how much opaque and elevated fees have cost investors in diminished returns in recent years.

The reprieve for analysts may not last. The FCA remains concerned that bigger banks are underpricing their research to maintain market share at the expense of smaller independent firms, and is expected to deliver the results of its review in the second quarter. My colleagues at Bloomberg Intelligence expect the regulator to make an example of firms it finds in breach of the rules.

But for now at least, it’s encouraging to see economic Darwinism at work in finance, with research departments seeking increased differentiation to win the eyeballs and fees from the buyside community. The laws of unintended consequences work in mysterious ways indeed.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.