Powell Finds a Way to Disappoint Markets. Again.

Another muffed Fed message leads market commentary. Plus, foreign-exchange fun, gold’s giveback and more.

(Bloomberg Opinion) -- The Federal Reserve, by cutting interest rates for the first time in a decade, signaling more reductions are possible and ending its balance-sheet reduction two months early, did what the market expected. Then Fed Chair Jerome Powell, who has a history in his relatively short tenure of making some incredible communication gaffes that have roiled markets, did it again.

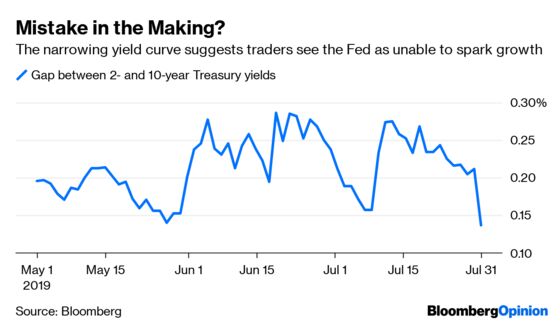

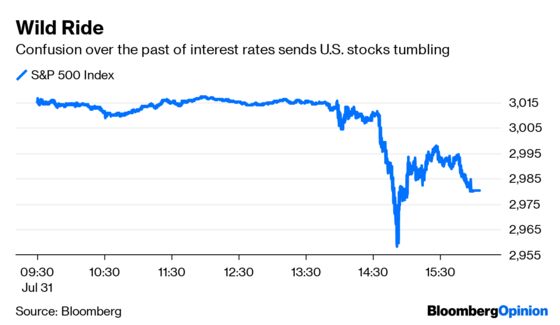

At his press conference a half hour after the Fed announced its decision, Powell said this rate cut wasn’t necessarily the start of an easing cycle. Stocks went from little changed to having the rug pulled out from under them, with the S&P 500 Index falling as much as 1.83%, while the closely watched gap between short- and long-term U.S. Treasury yields narrowed and the dollar soared. None of this was desirable for a Fed chairman and a central bank in the crosshairs of President Donald Trump, who has complained that Powell has “no feel” for markets. But of those market reactions, the movement in bonds may be the most concerning. To refresh, a flattening yield curve is generally a sign that bond traders see slower economic growth and inflation. So the reaction in the bond market, where the gap between two- and 10-year yields shrank to 0.14 percentage point from 0.23 percentage point, is in direct conflict with Powell’s opening statement that the rate cut was aimed at insuring against further downside risks to the economy while sparking faster inflation toward the central bank’s target. Also note that at the start of the last two easing cycles, in January 2001 and September 2007, the yield curve steepened, as you would expect it would. “The flattening of the curve implies investors are worried about a potential 'policy error' if the Fed doesn't act further,” the top-ranked team of rates strategists at BMO Capital Markets wrote in a note to clients.

In his defense, Powell was in a tough spot. He needed to sound dovish without actually sounding downbeat on the economy. It’s not an easy needle to thread. After all, nobody wants a central banker who isn’t confident in the abilities of his or her policies to get the job done. They also don’t want a central banker who is out of touch with what the markets are signaling, which in this case was that the economy needs more than a “mid-cycle adjustment policy.”

POWELL’S FED AND STOCKS

Stock market rallies on the day of Fed decisions have been a rare event under Powell, happening just twice in the 12 meetings he has chaired before today dating back to March 2018. Even so, Powell’s tenure has been pretty good for the stock market, with the MSCI USA Index up 10.2% since that March 2018 meeting, handily beating the 8.21% decline a MSCI index of global equities outside of the U.S. This year’s gains can be solely credited to the Fed and Powell’s dovish pivot back in January, which sent bond yields lower. Simple discounted cash flow analysis shows how lower rates make future earnings more valuable now, justifying higher multiples for equities even though profits are flat from a year earlier and forecasts have come way down. That explains the expansion in the S&P 500’s price-to-earnings multiple based on forecasted 2019 profits to 18.1 from 14.6 at the start of January. Up next is a notoriously tough month for equities. The S&P 500 has been down an average of 0.78% in August over the past 10 years, worse than any other month, according to LPL Research. Going back further, the S&P 500 has been up at least 20% by the end of July seven times with 2019 poised to become number eight before Wednesday. So it’s probably a good thing that stocks fell to trim this year’s advance to just under 20% because of those seven times, August was a down month in five of those years, LPL found. The last time it happened was in 1997, and the S&P 500 tumbled 5.7% in August.

FOREX FUN

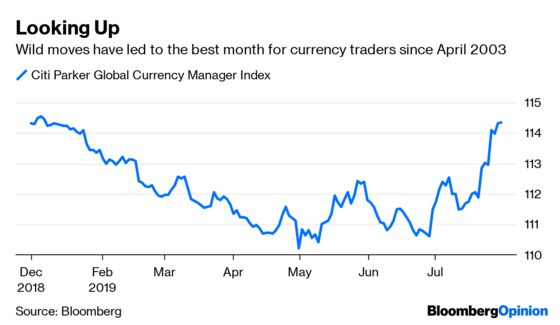

The dollar’s reaction is another seeming market anomaly, as lower rates are typically viewed as a negative for a currency. The Bloomberg Dollar Spot Index, though, soared as much 0.53% in its biggest gain since March 7. While bad for U.S. exporters, it capped an epic month for currency traders. The Citi Parker Global Currency Index, which tracks nine distinct foreign-exchange investment styles, was up 3.40% for July. Not only is that the best monthly performance since April 2003, it’s also more than what the index has gained in a full year since 2008. Another way to look at it is that returns have fallen in each of the past four years and seven of the past eight. Currency traders have been a victim of central bank transparency, which has suppressed volatility. It’s hard to be a contrarian when everyone knows what the major central banks will do, when they will do it and how much they will do it by. Also, increasing globalization means economies tend to move in the same direction more or less at the same time. In July, however, speculators benefited from some big moves in widely traded currencies. The British pound tumbled 4.27% against the dollar amid rising concern about the possibility of a so-called hard Brexit, the Swedish krona fell 3.85% and the Norwegian krone dropped 3.69% despite a general firming in the price of oil. On the flip side, Turkey’s lira soared 3.77% despite increased control over the central bank by the government and the Brazil real appreciated even with evidence of a slowing economy. Currency trading, it seems, is getting fun again.

GOLD BUGS SCATTER … FOR NOW

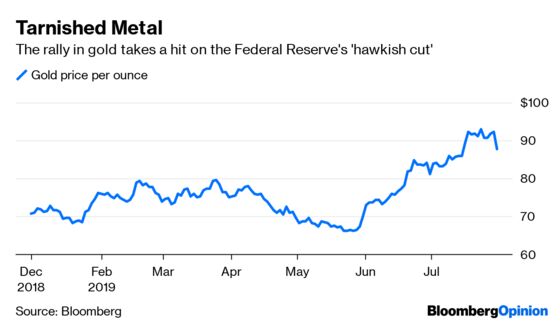

The Fed’s actions Wednesday are being described as a “hawkish cut.” At least that’s how the gold market reacted. Although rate cuts are traditionally good for the precious metal – with prices having risen 11.6% this year through Tuesday on the Fed’s dovish pivot – gold tumbled as much as 1.41% on Wednesday. Nevertheless, gold is still poised for its best annual showing since 2010. Just this month, prices topped $1,450 an ounce for the first time since 2013. Gold is traditionally viewed as a haven asset to own in times of turmoil, but what’s happening this year is less about strife than it is about financial repression, as major central banks embark on a new easing cycle. That can be seen in the almost direct correlation between gold and the rising amount of negative-yielding debt globally, which has more than doubled to about $13.8 trillion from less than $6 trillion October, according to data compiled by Bloomberg. The prospects for ever lower rates are generally a boon to gold, which doesn’t pay interest. But gold is that much more appealing in a world where Deutsche Bank figures that a whopping 43% of bonds globally outside the U.S. trade at negative yields. In a sign of demand, exchange-traded funds backed by bullion own the most amount of gold since 2013.

TEA LEAVES

Let the second-guessing begin. The Institute for Supply Management’s national manufacturing index for July set to be released Thursday will either support or discredit the Fed’s decision to lower rates for the first time in a decade. The median estimate of economists surveyed by Bloomberg is for little change, forecasting a reading of 52 for July versus 51.7 in June. The first thing to know is that the measure is a diffusion index, meaning readings above 50 denote expansion and those below 50 signal contraction. The second thing to know is that recent measures of regional manufacturing activity by the Fed have been all over the place, with those from the New York and Philadelphia branches coming in stronger than forecast and those from Richmond, Dallas, Kansans City and Chicago doing worse. Bloomberg Economics is more optimistic, expecting a reading of 53.5 in the ISM index, aided by the gains revealed in the recent durable goods report.

DON’T MISS

Fed Can’t Seem to Satisfy Bond Traders or Trump: Brian Chappatta

Boris Johnson Is Playing With Fire on the Pound: Lionel Laurent

Mark Carney Is Smacked in the Face by Reality: Marcus Ashworth

China Buying More U.S. Farm Goods Is a Dead End: David Fickling

This Political Storm Could Churn Up Some Hidden Gems: Shuli Ren

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.