Fed Will Keep Easy Policy Way After Coronavirus Subsides

(Bloomberg Opinion) -- The Federal Reserve has taken bold, unprecedented steps in the past two months to help mitigate the lasting damage to the U.S. economy caused by the coronavirus pandemic. If there was one overarching message from the Federal Open Market Committee’s first non-emergency decision since January, it was this: There will be no change of course anytime in the near future.

As expected, the central bank on Wednesday left its benchmark interest rate unchanged at a range of 0% to 0.25%, and to the surprise of some analysts, it left the interest rate on excess reserves unchanged at 0.1%. But more notably, the FOMC statement drew a clear distinction between the imminent risks from the Covid-19 outbreak and those that will linger long after the country reopens: “The ongoing public health crisis will weigh heavily on economic activity, employment, and inflation in the near term, and poses considerable risks to the economic outlook over the medium term.”

Veteran investors of the previous recession and ensuing recovery know that the Fed acts extremely gradually and with plenty of advance notice before moving away from the zero lower bound. Still, this explicit difference in time frames is a reminder that in the wake of a significant economic slowdown, the central bank will keep interest rates near zero when things are bad, when things are good and even when things are great. The Jerome Powell-led central bank is no different in committing to do whatever is necessary, for however long is necessary, to get the economy back toward where it was before the global pandemic.

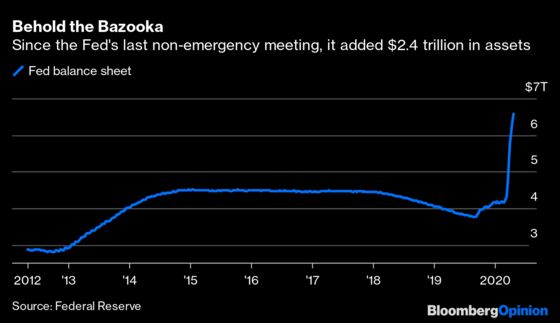

This pledge to stay the course also applies to the central bank’s bond-buying, which has already pushed its balance sheet to a record $6.57 trillion, from $4.15 trillion as of its last scheduled meeting in January. The Fed “will continue to purchase Treasury securities and agency residential and commercial mortgage-backed securities in the amounts needed to support smooth market functioning.”

It’s true that the central bank has been slowing its purchases gradually in recent weeks. But some investors expect the Fed will keep buying as the Treasury increases the size of its bond sales to fund the federal government’s relief efforts. “It’s our expectation that Fed asset purchases will be scaled to effectively offset U.S. Treasury issuance, to maintain an accommodative term structure of rates; critically the FOMC will utilize language that maintains optionality of action, as they don’t want to box in policy,” Rick Rieder at BlackRock Inc. wrote on Twitter before the decision.

Powell largely did just that, repeating time and again that the central bank was satisfied with what it had done so far but always stands at the ready to do more. “We think our policy stance is right where it should be, for now,” he said during the Q&A segment. And yet, “it may well be the case that the economy will need more support, from all of us, if the recovery is to be a robust one.”

Powell, who early in his tenure got in trouble for being more plainspoken than his predecessors, was refreshingly forthcoming when asked to explain the committee’s medium-term outlook. First, he said, the timeline for getting the coronavirus outbreak under control, discovering drugs to treat it and ultimately developing a vaccine is “shrouded in uncertainty.” Additionally, small- and medium-size businesses most impacted by lockdowns are “worth so much more to the economy than the sum of their net assets,” and a wave of insolvencies could damage the economy in ways the Fed can’t perfectly address. Workers could have trouble restarting their careers if they remain unemployed for too long.

By contrast, in the near term, “chances are that it won’t go right back to where we were,” Powell said of the economy. “It probably will take some time for us to get back to a more normal level of unemployment and ultimately to maximum employment,” he said. “We’re not going to be in any hurry to withdraw these measures or lift off.” As for the central bank’s corporate credit facilities, those are close to being finalized and will be up and running “soon,” Powell said.

Put it all together, and while the Fed didn’t explicitly mention a yield-curve control policy, it’s going to be awfully hard for bond traders to wager on any meaningful moves in the front part of the Treasury yield curve in the immediate future. Indeed, two-year yields fell 1 basis point, five-year yields dropped 2 basis points and 10-year yields were little changed. They’ve been stuck in a range for weeks now.

To Powell, that’s a signal that the world’s biggest bond market works again, indicating a job well done by the Fed’s policy. The tougher task is still ahead: facilitating an economic recovery. Whatever shape it takes, the central bank has made it clear it’ll be there to provide whatever support it can every step of the way.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.