The Trade-Off Between Jobs and Inflation Disappears

(Bloomberg Opinion) -- Earlier this week Representative Alexandria Ocasio-Cortez challenged Federal Reserve Chair Jerome Powell on whether something known as the Phillips curve -- the hypothetical inverse relationship between unemployment and inflation – is “no longer describing what is happening in today’s economy.” In a rare moment of bipartisan agreement, presidential economic adviser Larry Kudlow agreed.

Ocasio-Cortez is probably concerned about wages. Although unemployment is at historic lows, real wage growth has been distinctly underwhelming in recent years:

If the Fed cuts interest rates, or keeps them lower for longer, it could prolong the current expansion and raise wage growth. That would be especially beneficial for less-educated workers and minority workers, who tend to do the best near the end of an expansion. It would also be good for President Donald Trump’s reelection prospects, which is doubtless why Kudlow agreed with Ocasio-Cortez.

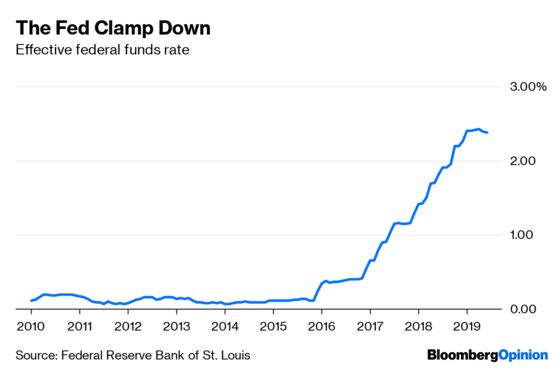

Despite sluggish real wage growth, the Fed raised rates pretty steadily from late 2016 through early 2019, at which point it halted:

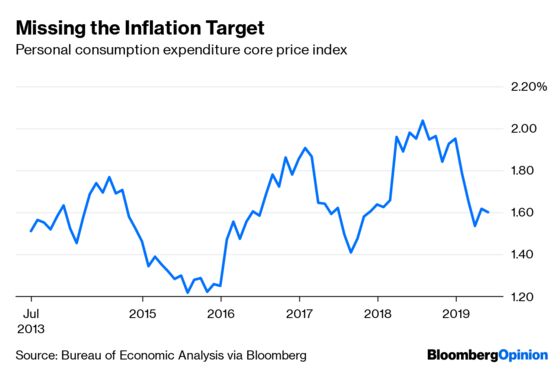

The standard reason for the Fed to raise rates is to ward off possible inflation. But inflation, excluding volatile food and energy prices, has generally been below the Fed’s official 2% target rate:

According to the classic Phillips curve, low unemployment should mean rising inflation. The fact that this hasn’t been happening seems to indicate that the Phillips curve has either broken down, or was never really right in the first place. By reminding Powell of this, Ocasio-Cortez is telling the Fed not to let fear of inflation get in the way of rate cuts.

But is she correct? Is the Phillips curve defunct? Economists have been arguing about this question for decades. In the 1970s, macroeconomist Robert Lucas pointed out that the Phillips curve should break down as soon as the Fed tries to use it to make policy. At that time, some policy makers believed that allowing higher inflation would lead to lower unemployment; Lucas argued that if people realized that the government was trying to do this, the government would get both high inflation and high unemployment. The stagflation of the 1970s seemed to bear out this prediction, and the classic Phillips curve fell into disrepute.

But over the years, economists have come up with a variety of alternative Phillips curves. Many rely on different definitions of inflation. The most popular ones, instead of using current or past inflation, use expectations of future inflation. (These are the models typically used at central banks.) Some use nominal wage changes in place of consumer price inflation. A number of other innovations have been tried.

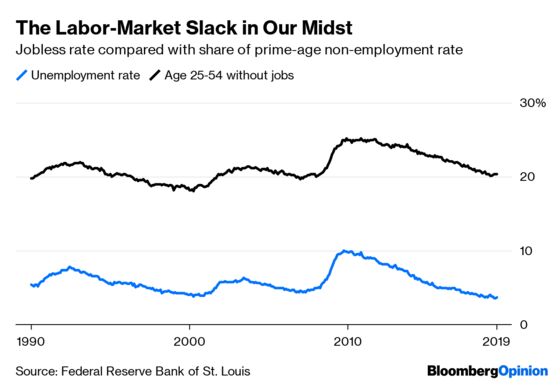

There are also different concepts of labor market slack -- i.e., how many workers could still get jobs without causing a bidding war and inflation. Traditionally, slack is represented by the unemployment rate. But in the most recent expansion, although unemployment has hit record lows, the percent of the population between the ages of 25 and 54 without jobs has not fallen to the all-time low levels it attained in the 1990s:

Using the prime-age non-employment rate and the employment cost index (a measure of nominal wage inflation), economist and writer Adam Ozimek showed that recent levels of unemployment and inflation fit nicely along a traditional Phillips curve. In other words, the reason low unemployment hasn’t led to higher inflation in the recent expansion could be that true unemployment simply isn’t that low.

Of course, Ozimek and others who claim that the Phillips curve is alive and well might simply be cherry-picking their data. Past tests of various Phillips curves have generally found that they do a poorer job of forecasting inflation as time goes on. New and improved versions might prove equally fickle.

So don’t expect the academic dispute over the Phillips curve to end anytime soon. But in some sense, that debate is irrelevant to the question of whether to cut interest rates right now. If the curve has broken down, as Ocasio-Cortez suggests -- or if it was always a mirage -- then the Fed should probably cut interest rates, in order to sustain the expansion and help marginal workers get a raise. But if there really is a Phillips curve and low inflation is due to continued labor market slack, as Ozimek argues, it means there are still some workers left to be put to work, which also implies that the Fed should cut rates.

So essentially everyone now agrees -- looser monetary policy is in order. But if inflation were to make a comeback someday, the argument over the Phillips curve will inevitably reignite.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2019 Bloomberg L.P.