There’s Something Worse Than Running Deutsche Bank

(Bloomberg Opinion) -- Juergen Fitschen probably thought life would become a bit calmer when he stepped down as co-chief executive of Deutsche Bank AG in 2016. Later that year he was nominated supervisory board chairman of German electronics retailer Ceconomy AG, where the 70-year-old now collects a salary of 240,000 euros ($273,816), a fraction of his Deutsche days.

And then, all hell broke loose. Since its separation from the German cash-and-carry group Metro AG, Ceconomy’s fortunes have gone from bad to abominable. A succession of profit warnings resulted in the departure of both the chief executive and chief financial officer, forcing Fitschen to hunt for permanent replacements, so far to no avail.

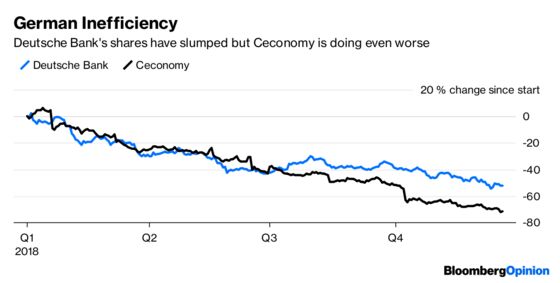

On Wednesday, Ceconomy capped its annus horribilis by reporting a 210 million euro net loss and scrapping the dividend. The shares have lost three-quarters of their value in 2018, a worse performance even than Deutsche Bank, where Fitschen is still an adviser.

Remarkably, things could get grimmer still for Ceconomy. Results in the fiscal year to September were flattered by non-recurring items. Meanwhile, 2019 looks like being another tough year for sales and the company faces unspecified restructuring costs. Ceconomy’s balance sheet isn’t the strongest either. So calling 2019 a “year of transition,” as management did today, could prove to be an understatement.

Like other bricks and mortar retailers, Ceconomy has suffered as customers migrated online (largely to Amazon.com Inc.), though many of them aren’t ashamed about first popping into one of Ceconomy’s enormous Saturn or MediaMarkt stores for a free consultation. It’s been stung too by Germany’s “unusually” hot summer. Although, with climate change only set worsen, northern hemisphere retailers really need to get used to people not going shopping in July or August.

Many of Ceconomy’s problems are home-made, however. It appears worryingly incapable of forecasting earnings with any precision, in part because it depends on rebates from suppliers for selling an agreed volume of goods (which in some cases it didn’t). That has left Ceconomy leaning heavily on suppliers to boost its cash reserves of 1.1 billion euros. It needs the money to fund a restructuring of the German business and further digitalization.

Better working capital contributed almost two-thirds of the company’s free cash flow in the 12 months to September and that happened in part through a “temporary” extension of supplier payment terms. That doesn’t sound sustainable.

And from next year the new IFRS 16 accounting rules will force Ceconomy to include roughly 2.5 euros billion of store lease liabilities on its balance sheet. While there’s no impact on its actual cash, the change means Ceconomy’s net liquidity position will probably become net debt, which won’t help optics.

Ceconomy raised almost 280 million euros of capital this year when mobile communications provider Freenet AG purchased a 9 percent stake. But its losses have undone most of the benefit of raising that money. The company is rated only one notch above junk by Moody’s, which understandably has a negative outlook.

A downgrade to junk would be unhelpful to say the least. Ceconomy’s annual report warns it would have a negative impact on corporate liquidity and financing, including the possibility of “worsening payment conditions” and less favorable credit insurance limits. Fitschen has swapped one crisis for another.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2018 Bloomberg L.P.