(Bloomberg Opinion) --

Spare a shekel for a beleaguered European bank.

There’s no pleasing some people. Europe’s banks have been under severe pressure for years. That pressure has intensified of late as financial-crisis-era debt comes due and the euro-zone economy once again slows. While the shares of banks in the U.S. are roughly back where they were before the crisis, European bank shareholders are sitting on terrible losses:

Then came Thursday, when the European Central Bank sprang a real surprise by announcing a sweeping package of measures designed to stimulate the economy, including a fresh round of targeted lending to banks. Such a move was thought likely, but not as soon as now. This news should have alleviated the fears surrounding European banks, but instead the FTSE-Eurofirst 300 bank index had its worst day of the year, falling more than 3 percent. With the exception of HSBC (which can only tenuously be described as a European bank), every member of the index fell. Trading at less than two-thirds of their book value, distrust of the sector is extreme:

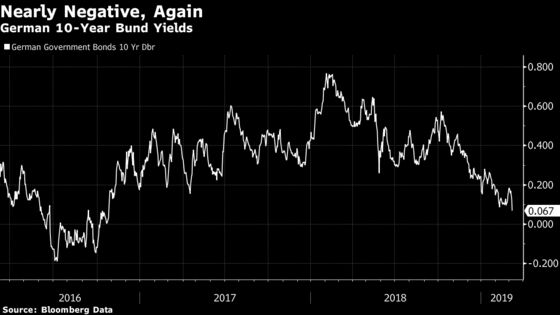

So why the dismissive response from investors? First, a more dovish ECB means lower interest rates, which make it harder for banks to generate decent profits from lending. German 10-year bund yields, which were already heading lower before the ECB’s decision, continued to drop, leaving them just 6 basis points away from turning negative in a development that the ECB must surely have hoped was left behind in 2016:

Second, the ECB may have been too clear about the reasons for its generosity. Its forecasts for inflation and growth were slashed, while immense political challenges facing the euro zone are not going away. Even if the circus over Brexit finally results in a British departure from the European Union this month, plenty of other serious issues remain to be resolved, starting with Italy’s relationship with the EU. Italian bond yields, however, fell sharply, but the share prices of Italy’s troubled banks also posted a big decline.

Finally, the ECB had not done enough to prepare the market, and therefore gave the impression that it was running scared. It is not a good sign for the central bank that Bloomberg Opinion columnist Mohamed El-Erian described its latest policy package as a dramatic flip-flop. Put differently, the message is that “Central Banks Don’t Have the Answer and Markets Know It,” to borrow the headline from Robert Burgess’s Bloomberg Opinion column. Europe’s bad day set the scene for a troubled “risk-off” day in the U.S., where a stronger dollar, buoyed by the tanking euro, did nothing to help sentiment.

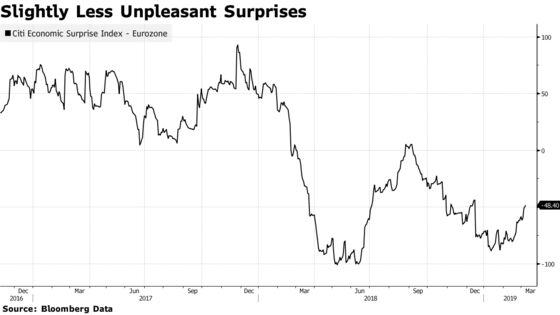

So it’s clear that sentiment toward the euro-zone economy is dreadful. But is the negativity excessive, and does that create an opportunity to profit? Until Thursday, the data implied that economists had at last got their arms around the extent of the euro zone’s problems. Citigroup’s economic surprise index for the euro zone, which nosedived in 2018, has shown signs of improvement this year, which should be a good sign for banks:

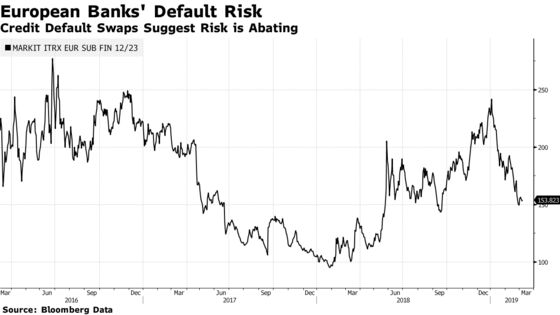

Another point in favor of the banks comes from the market for credit-default swaps. Narrower spreads imply a reduced risk of default, and widely followed indexes suggest that perceived credit risk for the sector has fallen significantly this year. This may reflect confidence that the ECB would offer help, and that Thursday’s announcement had been discounted, but it still suggests that the intensity of pessimism towards the sector has been overdone:

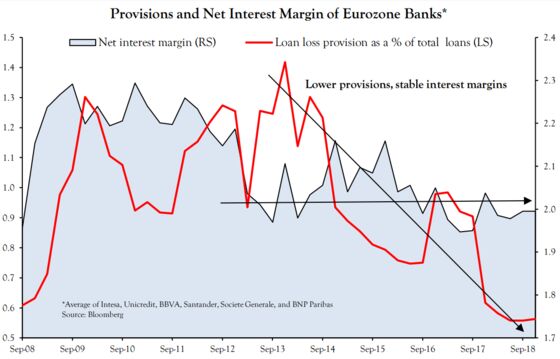

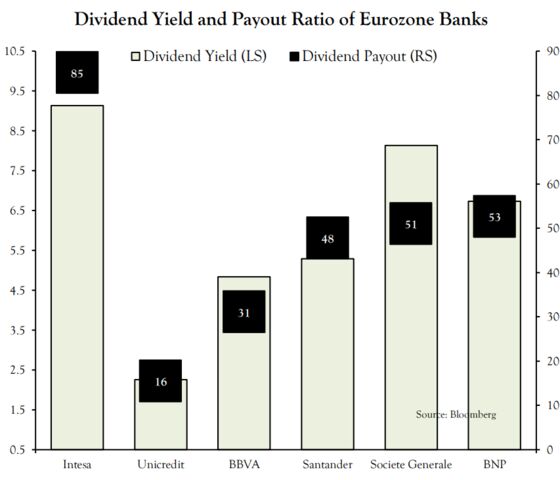

None of this changes the undeniable fact that European banks have been a value trap for a decade. They have looked cheap but continually have failed to deliver returns to contrarian investors. Uncertainty remains high. But they might just make sense as a value proposition if there is a margin of safety. INTL FCStone strategist Vincent Deluard suggests that the safety comes from their dividends, which are high and well covered. He offers this chart to show that banks’ net interest margin has been stable for five years as bad loan provisions declined:

Meanwhile, dividend yields look mighty generous at a time when 10-year bunds yield almost nothing:

As Deluard puts it, there is no need for European bank profits to return to pre-crisis levels for investors to profit. All investors need is for the banks to survive without cutting their dividends for a couple of years. It is a decent bet that the European economy will not be so bad as to force dividend cuts. Stop me if you think that you’ve heard this one before — but maybe, just maybe, it is time to buy European bank shares.

Authers notes:

Trade is slowing down: Whether the cause is front-loading of orders ahead of the planned imposition of tariffs, or a broader slowdown in economic activity, world trade is barely growing. In fact, it has just suffered two successive monthly contractions. This useful summary chart is from Capital Economics in London:

This is going to create worry until such time as a U.S.-China trade deal can be agreed, and subsequent trade volumes can show that this slowdown was driven merely by tariff concerns and not by economic weakness. For the time being, it is worrying.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

John Authers is a senior editor for markets. Before Bloomberg, he spent 29 years with the Financial Times, where he was head of the Lex Column and chief markets commentator. He is the author of “The Fearful Rise of Markets” and other books.

©2019 Bloomberg L.P.