(Bloomberg Opinion) -- What happened to Europe’s high-yield bond market?

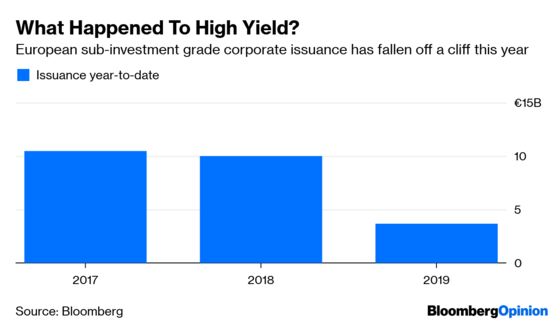

It has been a banner year so far for bond issuance for investment grade companies and governments. But for those with weaker credit ratings, sales are about 60 percent down from the same time last year.

This is a worrying sign that financing is shutting off for the borrowers that are most vulnerable to swings in liquidity. The European Central Bank needs to think harder about breathing life into the wider corporate engine of growth before it stalls for good.

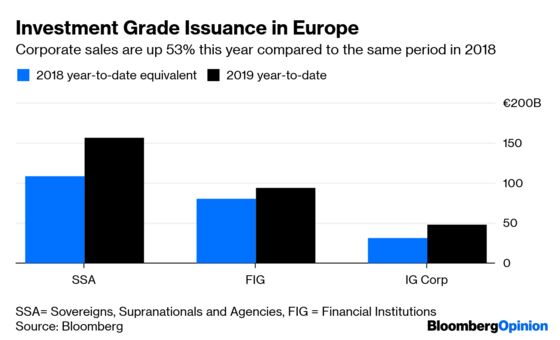

The region’s bond investors have flocked to the safety of high-grade this year, most notably sovereigns, where issuance is up 45 percent to over 150 billion euros so far. Volumes for investment-grade companies are up even more, reaching nearly 50 billion euros. Spreads on 22 of the 24 deals that priced this month have tightened.

Pick your reason for this new-found love of fixed income: The Federal Reserve’s dovish turn, stuttering euro-area economies, and a relatively easier political environment. Italy is a perfect example. At the end of 2018 it could barely issue long-dated debt. Now it’s fighting buyers off for a 30-year security.

This frenzy has helped lower-rated countries such as Greece and Cyprus to return to the debt markets. This suggests investors are more confident the European Union will stick together – Greece's successful transition out of its third bailout is testimony to that.

But the enthusiasm has not filtered through to the high-yield corporate market. This demonstrates there’s significant skepticism on the outlook for riskier issuers, which is perhaps understandable. The euro-area economy has hit a brick wall and is on the verge of a manufacturing recession.

It’s a different story across the Atlantic. In the U.S the market is as healthy as ever and the pace is about the same as 2018, with at least 50 new deals totaling more than $30 billion as of the end of last week.

There are some signs that low-rated European corporates unable to muster demand in bond format are exploring other options, such as the less-liquid and more restrictive loan market. But these are not as deep or flexible as high-yield bonds.

This is an accident waiting to happen, and it is partly of the ECB’s making. It’s becoming more apparent that the decision to end quantitative easing was premature.

The central bank chose to curtail its corporate sector purchases, along with its other bond-buying programs, at the end of 2018. It had never directly targeted the high-yield market as it amassed 180 billion euros of mostly investment-grade-rated corporate bonds. However, the purchases drove spreads tighter across all sectors, ensuring that credit markets would stay open.

That benefit swiftly unraveled as it became clear the programs were going to stop. Borrowing costs have returned to levels seen before the ECB started propping up the market with its Corporate Sector Purchase Program.

There is not much hope any near-term change to policy will help. ECB officials have raised the prospect of a new round of targeted long-term refinancing operations at the March 7 meeting. While this would allow banks across the region to access super-cheap liquidity, and in theory should encourage them to boost lending to riskier corporate credits, that has not convincingly proved to be the case in previous rounds.

The real benefit of TLTROs has been to subsidize existing lending and to prevent a worsening of liquidity. If the ECB were to fail to offer a new round by June it would effectively be tightening funding conditions. This is not a good look with the economy stalling, and officials seem to be recognizing this.

But just as TLTROs were not the answer for corporate funding needs when the ECB first started its extraordinary stimulus, nor are they today. The stuttering high-yield primary market should prompt policy makers to think wider and deeper than just using the banking system transmission mechanism to keep liquidity flowing. Even if sentiment quickly reverses, and a flood of new issues comes in, that this corner of the credit market even got this thin should give officials pause.

It may be madness to even consider restarting quantitative easing, or extending it to include high-yield debt, but the ECB may have little choice but to start thinking of some alternatives.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.